The Average VC Check Is Growing. The Number of Startups Getting One Is Shrinking.

Table of Contents

Introduction

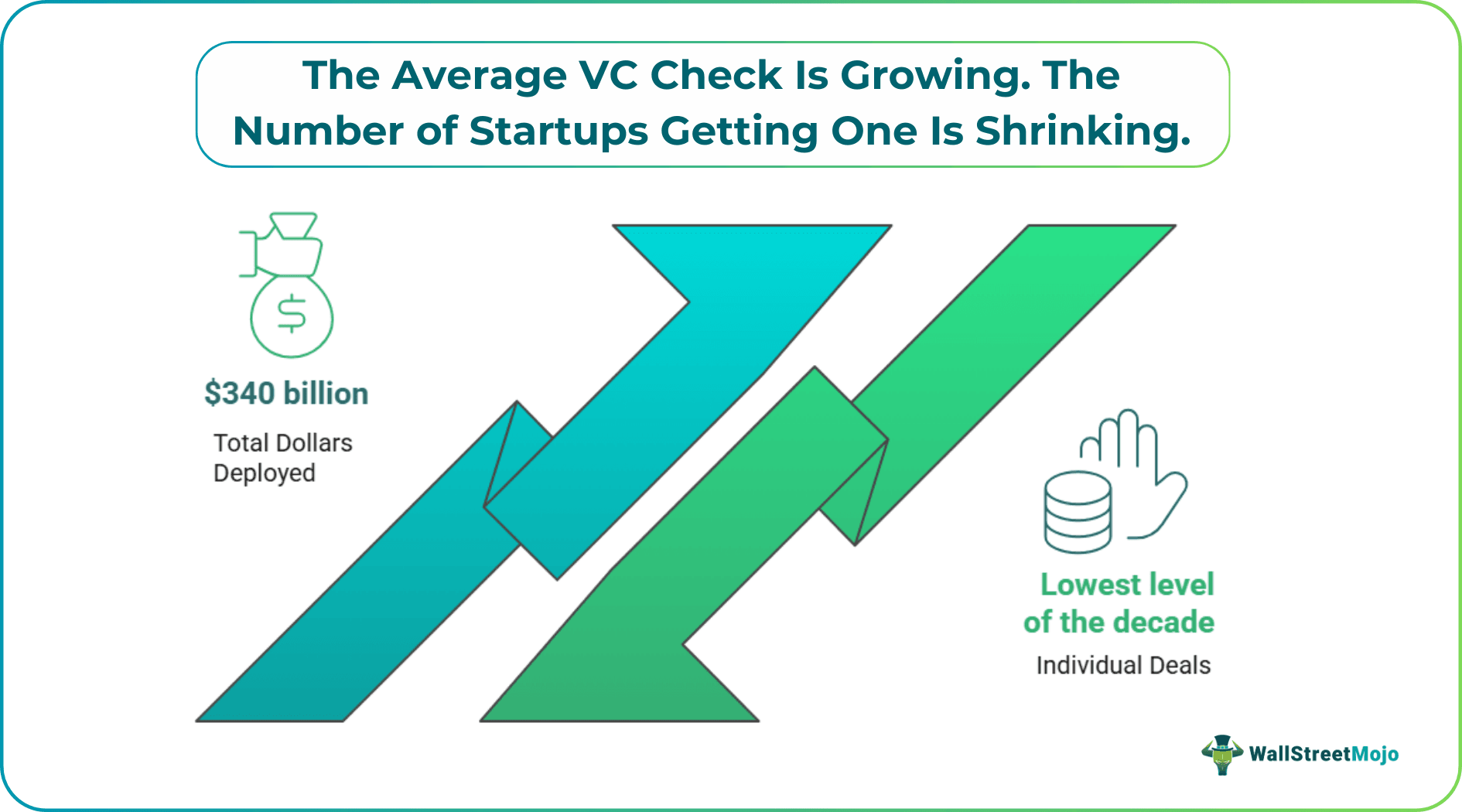

The headline number looks reassuring. Nearly $340 billion flowed into US venture-backed companies in 2025, the second-highest year on record. For venture capital investor Alexander Kopylkov, however, that figure conceals a more important story.

According to SVB's State of the Markets report, total dollars deployed in 2025 surged while the number of individual deals fell to the lowest level of the decade. More capital. Fewer bets. These two facts, sitting side by side, describe a market that is not growing — it is concentrating.

The Numbers Behind the Shift

Mega-rounds — deals exceeding $100 million — surged 77% in 2025, capturing 65% of all venture funding. In 2021, at the peak of the last boom, mega-deals accounted for just 18% of total investment. The gap between then and now is not a market cycle. It is a structural change in how capital is deployed.

The concentration becomes even sharper when you look at distribution. The top 1% of companies by valuation captured a full third of all capital raised last year. The bottom 50% received just 7%.

February 2026 made the pattern visible in real time. Total global venture funding hit $189 billion — the largest startup investment month ever recorded. Of that, 83% — roughly $156 billion — went to just three companies: OpenAI ($110 billion), Anthropic ($30 billion), and Waymo ($16 billion). Overall deal count did not move. The average deal size did.

Why This Is Happening

According to Kopylkov, the mechanism is straightforward: as exit timelines lengthened and valuations normalized after 2022, large funds stopped diversifying and started concentrating.

"The math changed," he says. "Writing 30 small checks becomes harder to justify when your top performers already absorbed most of the return. Investors are betting bigger on higher-conviction opportunities — and they are defining conviction very differently than they did three years ago."

Kopylkov breaks it down into first principles: longer holding periods → compressed return windows → pressure to concentrate capital in the highest-probability outcomes. The result is a market where the decision to invest has become binary. Either a company clears the bar clearly, or it does not clear it at all.

What Is Actually Getting Funded

The shift in capital distribution maps directly to a shift in investor criteria.

Citing data from SVB's 2026 State of the Markets report, Kopylkov notes that the metrics driving investment decisions today bear little resemblance to those of 2021. Burn multiple, revenue per employee, CAC payback period, and gross margin per customer have replaced growth rate as the primary evaluation framework.

"The companies getting the largest checks are not necessarily the fastest-growing ones," he says. "They are the ones where the financial structure holds up under scrutiny."

From an investor's perspective, Kopylkov evaluates early-stage companies by looking at their efficiency ratio — net new ARR divided by burn rate. An efficiency ratio above 1.5 is considered elite in the current environment. "That single number tells me more about a company's long-term trajectory than three years of growth charts."

What Founders Should Do With This

The concentration trend creates a clear decision point for founders raising in 2026.

For founders, Kopylkov recommends thinking in two tracks: either position squarely within an investor's highest-conviction category — AI infrastructure, autonomous agents, defense tech — or build the financial profile that makes a smaller, cleaner round the obvious and logical choice.

"Chasing the mega-round without the mega-round profile is the most common mistake I see right now," he says. "A well-structured $3 million seed from the right investor closes faster and creates more value than a $12 million round from the wrong one at the wrong terms."

In his view, the bifurcation will deepen through the remainder of 2026 before stabilizing. The companies that understand which market they are competing in will raise more efficiently. The ones that do not will spend 18 months learning the same lesson at considerable cost.

The Bottom Line

The venture market is not contracting. It is sorting.

More money is available than at almost any point in history — it is simply moving through a narrower funnel, toward a smaller set of companies meeting a higher set of standards. For founders, that is not necessarily bad news. It is a clear signal about what the market is pricing right now: capital efficiency, credible unit economics, and a team that can execute under constraint.

The average VC check has never been larger. The question is whether your company has the profile to receive one.