Financial Analysts Evaluate Impact of Digital Entertainment Market Expansion

Table of Contents

Introduction

Is the quick capital allocation toward digital entertainment merely an anomaly, or does it symbolise a permanent structural change in the global economy? For institutional investors and financial analysts, the answer determines the viability of billions of dollars in portfolio assets. As physical discretionary spending continues to migrate toward virtual experiences, the "experience economy" is increasingly becoming a digital-first phenomenon.

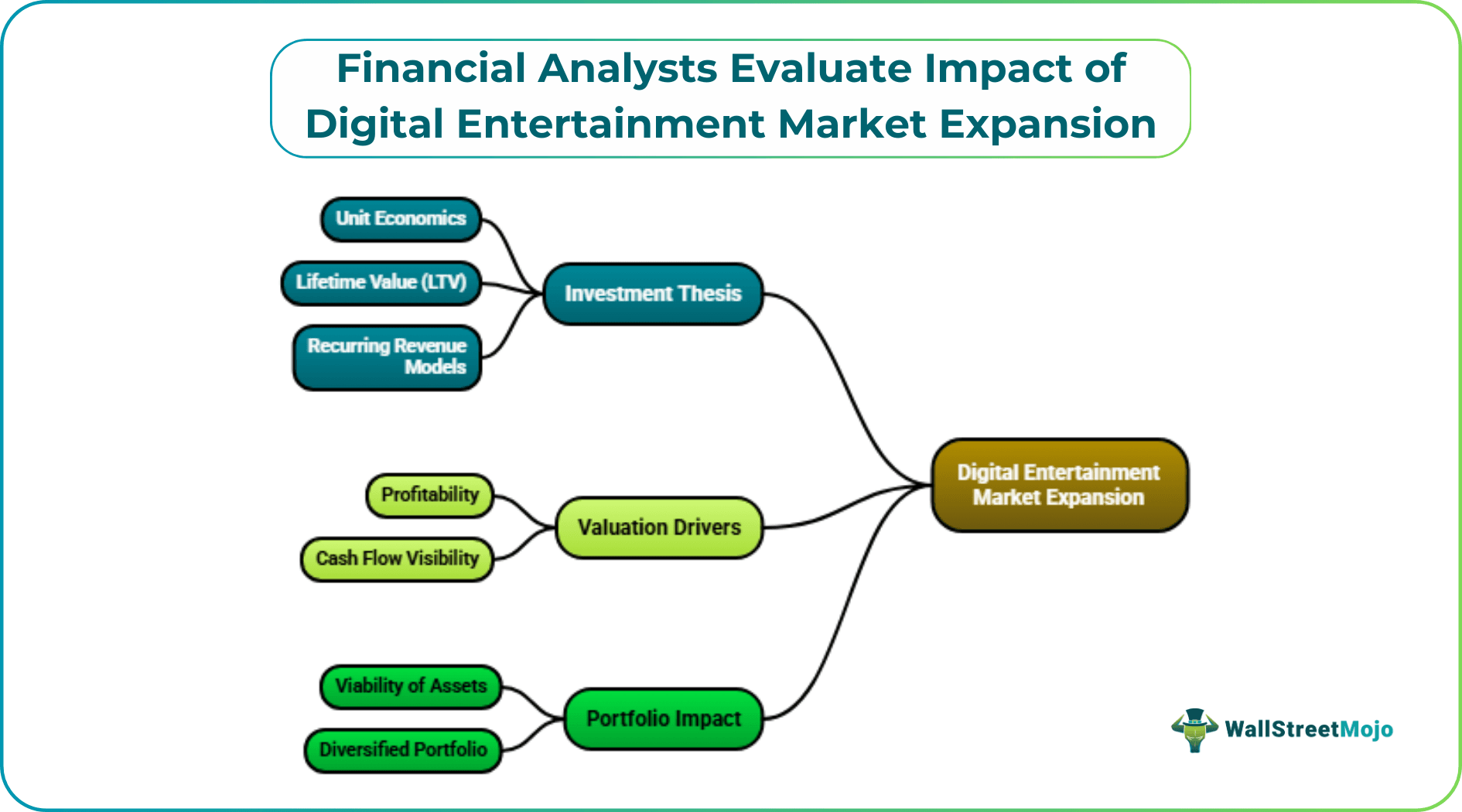

The investment thesis for digital entertainment has gone further than simple user acquisition numbers. Today, savvy analysts focus on unit economics, lifetime value (LTV), and the stickiness of recurring revenue models. With capital markets tightening and interest rates stabilising, profitability and cash flow visibility have replaced "growth at all costs" as the immediate valuation drivers. This maturity in the sector suggests that digital entertainment is no longer a speculative play but a foundational component of a diversified portfolio.

Identifying High-Growth Niches Within Entertainment Sectors

While the broader sector is expanding, smart capital is selectively targeting specific high-growth niches. Video advertising, in particular, has emerged as a dominant revenue engine, influencing the profit and loss statements of major media conglomerates.

As platforms refine their algorithms, the efficiency of digital ad spend has improved, attracting corporate budgets away from traditional broadcast media. In the 2025 financial year alone, internet advertising spending in Australia surged to A$17.2 billion, with video formats capturing nearly a third of that total. This change shows the value of platforms that can successfully blend content delivery with high-yield advertising inventory.

Another area witnessing intense capital deployment is the streaming and content production sector. The narrative that "content is king" is backed by substantial balance sheet commitments. Major subscription video-on-demand (SVOD) providers, including global giants like Amazon Prime and Netflix, invested over USD 341 million into Australian programs during the 2023–24 financial year.

This level of localised investment serves as a defensive moat, increasing barriers to entry for potential competitors while ensuring compliance with local content quotas. For investors, high content costs are a double-edged sword: they depress short-term free cash flow but are essential for long-term retention and library value.

Online casinos are a profitable, high‑growth niche within a large global gambling market. Australia’s restrictive regime, on the other hand, means it captures relatively little of the economic upside compared with more open, licensing‑driven jurisdictions. Markets that license online casinos attract game studios, platform providers, payments and RegTech companies.

A regular player mainly benefits through safety, fairness, and better long‑term value, with online casino platforms offering everything from payment flexibility to gaming options (Source: https://www.gameshub.com/australia/online-casinos/). Most of the big money flows to operators, suppliers and regulators in the chain. By keeping online casino illegal, Australia discourages that cluster from basing itself locally and cedes high‑skill tech and compliance jobs to overseas hubs.

The competitive intensity in these niches is driving consolidation and strategic partnerships. Smaller players are finding it increasingly difficult to compete with the economies of scale enjoyed by global tech giants. The market is seeing a separation between massive, diversified ecosystems and niche, specialised providers.

Analysts are increasingly favouring companies that own their intellectual property (IP) and distribution channels, as vertical integration allows for better margin control and data ownership, a critical asset in an era of privacy-first advertising.

Understanding Regional Regulatory Frameworks And Revenue Models

Investing in digital entertainment requires a fine understanding of the regulations, which vary significantly across different verticals and jurisdictions. In Australia, the regulatory environment is characterised by strict consumer protection laws and evolving taxation frameworks that directly impact net margins.

Beyond compliance, the revenue models themselves are experiencing a significant transformation. The binary distinction between subscription-based (SVOD) and advertising-based (AVOD) models is blurring. Most major platforms now offer hybrid tiers, allowing them to capture price-sensitive consumers while monetising their attention through ads.

This hybrid approach diversifies revenue streams and reduces churn, as users can downgrade rather than cancel during periods of financial stress. For equity analysts, this shift requires a recalibration of valuation multiples, as hybrid models often command different price-to-earnings ratios compared to pure-play subscription businesses.

The taxation of digital services remains a risk factor. Governments worldwide are increasingly looking to digital services taxes (DST) to capture value generated by offshore tech giants. In the Australian context, changes to tax structures or local content quotas can have an immediate impact on the bottom line.

Investors must therefore apply a "regulatory risk premium" when valuing assets in this sector, ensuring that projected returns adequately compensate for the potential of sudden legislative changes that could alter the unit economics of a platform.

Risk Management Strategies For Thematic Investing Portfolios

While the growth narrative is compelling, thematic investing in digital entertainment carries inherent risks that must be managed through diversification. The primary risk is technological obsolescence; consumer preferences can change quickly, rendering dominant platforms irrelevant within a few years.

To mitigate this, portfolio managers often avoid concentrating exposure in a single platform or technology. Instead, they seek exposure to the broader ecosystem, including infrastructure providers, content creators, and hardware manufacturers. This "pick and shovel" approach allows investors to benefit from the sector's growth without betting on the success of a single consumer-facing app.

Long-term projections remain robust, providing a degree of comfort for patient capital. Market research indicates that the Australia digital media market is projected to reach USD 57.61 billion by 2030, driven by a compound annual growth rate of 14.5%. This strong macroeconomic tailwind suggests that even with short-term volatility, the sector's trajectory is upward. However, investors must remain vigilant regarding valuation compression. As the market matures, growth rates will naturally decelerate, potentially leading to a repricing of equities that are currently trading at high multiples based on early-stage growth expectations.

Specific segments like streaming require careful monitoring for market saturation. With the Australia streaming market expected to grow at 18.0% CAGR through 2035, the competition for viewer attention will intensify. This will likely lead to higher customer acquisition costs (CAC) and pressure on operating margins.

Successful investment strategies will favour companies with strong balance sheets capable of sustaining these higher costs, as well as those with diversified revenue streams that are not solely dependent on subscriber growth.