How to Apply for an Education Loan in India and Meet the Eligibility Criteria

Table Of Contents

Introduction

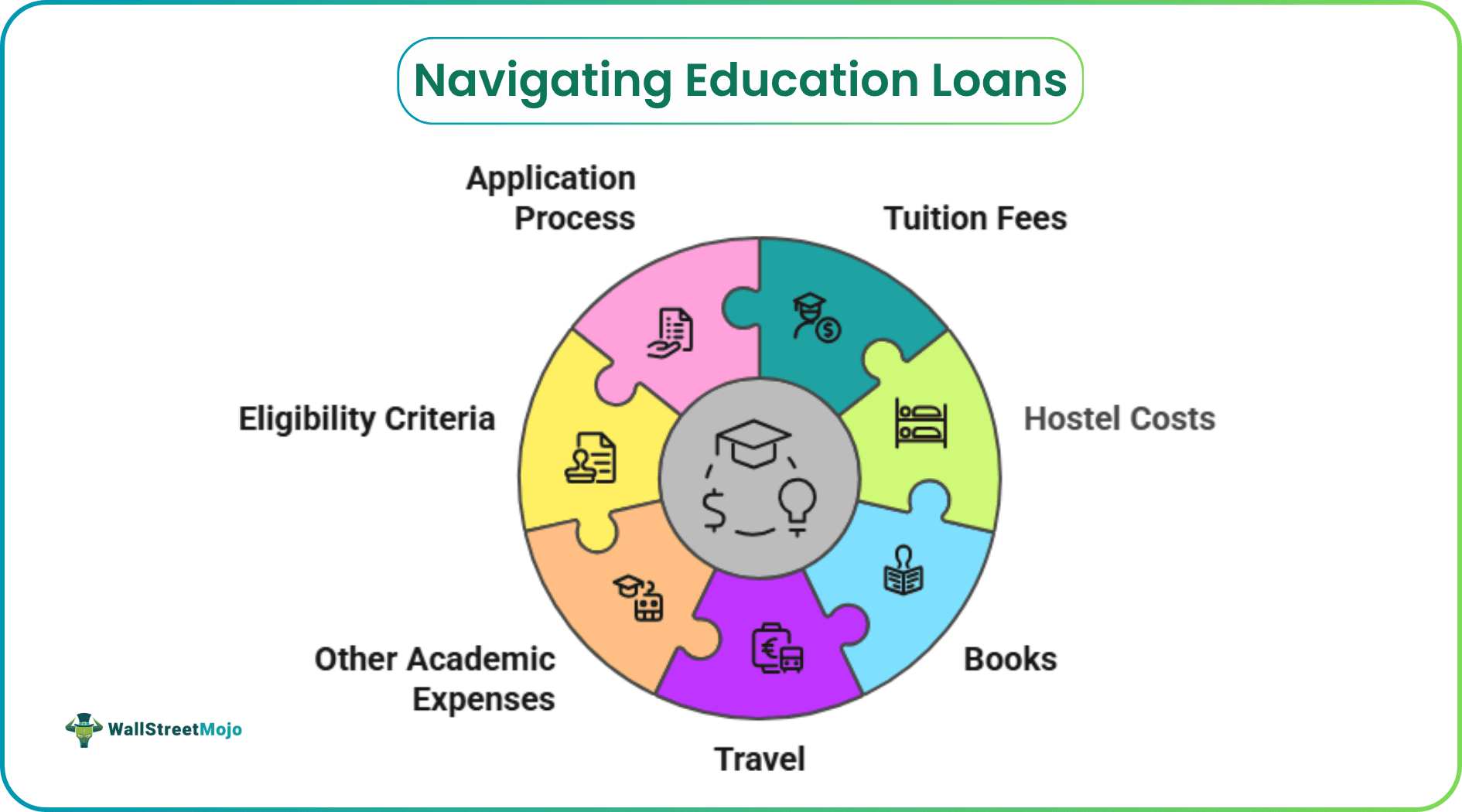

An education loan can help you fund higher studies without delaying your plans. You can use it for tuition fees, hostel costs, books, travel, and other academic expenses. Understanding the eligibility criteria and application process in advance helps you avoid delays and reduce the risk of rejection.

Understanding What an Education Loan Covers

You can use this form of funding for recognised courses in India or abroad. It usually covers:

- Tuition fees charged by the institution

- Examination, library, and laboratory fees

- Hostel or accommodation costs

- Books, equipment, and study material

- Travel expenses for overseas education

Most banks and NBFCs in India offer both secured and unsecured education loan options. A secured loan requires collateral such as property or fixed deposits, while an unsecured loan is primarily assessed based on your co‑applicant’s income stability and creditworthiness.

As per RBI‑regulated lending norms, banks and NBFCs carefully assess your repayment capacity before approval. For most education loans, lenders typically request a co‑applicant, often a parent or guardian, to strengthen the application and ensure smoother approval.

Education Loan Eligibility: What Lenders Usually Check

Before you apply, you should understand the core education loan eligibility criteria. While policies differ across lenders, the following factors are commonly assessed.

First, you must be an Indian citizen. Most lenders require confirmed admission to a recognised institution. The course should be approved by a competent authority in India or abroad.

Your academic record also matters. A consistent record signals your ability to complete the chosen programme successfully.

Your co-applicant’s earnings play a major role. Lenders review salary slips, income tax returns, and bank statements. A stable income improves approval chances.

Credit history is equally important. A strong credit score of the co‑applicant indicates responsible repayment behaviour.

If you apply for a higher amount, you may need collateral. This could include residential property or other acceptable assets.

For example, if you secure admission to a recognised engineering college and your parent has steady income with a good credit record, your application may be viewed more favourably.

Documents You Usually Need

You should keep the required papers ready before starting the application.

These typically include:

- Identity and address proof such as Aadhaar and PAN

- Admission letter from the institution

- Detailed fee structure

- Academic mark sheets

- Income proof of the co-applicant

- Recent bank statements

- Collateral documents, if applicable

Incomplete documentation often delays processing.

Step-by-Step Process to Apply

You should begin by comparing different lenders. Look at interest structure, repayment period, and moratorium terms. Some lenders offer fixed rates, while others provide floating rates linked to benchmarks.

You can check options through financial marketplaces such as bajajfinservmarkets.in for broad comparisons. However, you should always verify final terms directly with the lender.

Once you shortlist a lender, check the criteria carefully. Then submit the application form with required documents.

The lender will verify your admission details, academic record, and co-applicant’s income. They may conduct a credit check and, if needed, evaluate collateral.

After assessment, you receive a sanction letter stating the approved amount, rate type, and repayment terms. Funds are usually disbursed directly to the institution as per the fee schedule.

Factors That Improve Approval Chances

Planning early can significantly improve your chances of securing an education loan. A strong co‑applicant with steady, verifiable income reduces the lender’s risk perception. Choosing a recognised and reputable institution also strengthens the overall application.

Applying for a loan amount that aligns closely with actual academic expenses is advisable. Offering collateral, when possible, may help you secure better terms, including lower interest rates. Maintaining a healthy credit profile is equally essential. Even minor delays or defaults on existing loans or credit cards can negatively affect approval.

Common Mistakes to Avoid

You should avoid applying before securing confirmed admission. Many lenders require formal proof.

Do not ignore the repayment structure. Understand when repayment begins and how the moratorium works.

You should also read the agreement carefully. Look at processing fees, prepayment conditions, and any penalties.

Borrowing more than required can increase long-term burden.

Summary

Applying for an education loan in India involves careful preparation. You need confirmed admission, proper documents, and a reliable co-applicant.

Lenders assess income stability, academic background, and credit history before approval. Understanding eligibility criteria in advance helps you prepare stronger documentation.

If you compare options carefully and plan your finances, you can secure funding smoothly and focus on your studies with greater confidence.