Table of Contents

What Is Expected Credit Loss (ECL)?

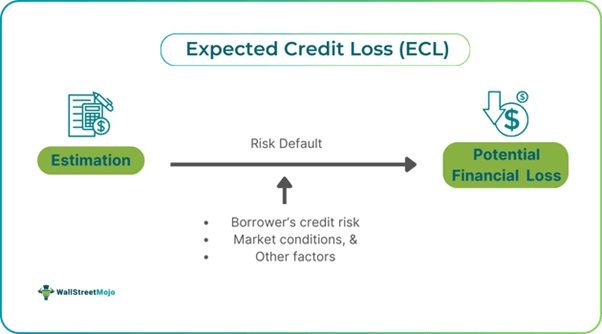

Expected Credit Loss (ECL) refers to a financial measure used to estimate potential losses related to financial assets, particularly receivables and loans, upon default. It helps in understanding future potential losses associated with financial assets and how to identify and address them in financial reports.

ECL utilizes current conditions, historical data, and reasonable estimates to determine potential losses over the entire life of a financial asset due to non-payment by customers. This approach has improved risk management and financial reporting through a detailed depiction of potential credit losses.

Key Takeaways

- Expected Credit Loss (ECL) is a financial metric used to project potential major losses from financial assets, particularly loans and receivables, in the event of default.

- ECL aids in understanding future possible losses related to financial assets and provides a framework for identifying and addressing these losses in financial reports.

- The formula commonly used by firms to calculate anticipated losses due to credit default is: ECL = Exposure at Default (EAD) * Probability of Default (PD) * Loss Given Default (LGD).

Expected Credit Loss Explained

Expected credit loss can be defined as the estimated impairment of a lease or other financial asset based on the probability of default and the potential loss due to that default. This forward-looking approach contrasts with the incurred loss model, which recognizes losses only after they occur. ECL serves as a financial metric used to project potential losses from financial assets, particularly loans and receivables, in the event of default.

ECL has significant implications for risk management and financial modeling, necessitating proactive loss provisioning that enhances the resilience of financial institutions during economic downturns. Many banks and financial organizations use ECL to determine necessary provisions related to potential credit losses, impacting capital adequacy assessments and lending practices. The current expected credit loss model, applied under IFRS 9, provides a structured approach to accounting and estimating credit losses.

Additionally, ECL influences how banks report their earnings and manage risk, promoting transparency in financial reports and encouraging more prudent lending practices. It is applicable to various financial instruments, including leases, loans, and debt securities, ensuring reliable financial statements. Consequently, the current expected credit loss accounting standard has transformed how financial institutions manage credit risk, enhancing both accountability and transparency in financial reporting.

Formula

The ECL formula:

ECL = Exposure at Default (EAD) * Probability of Default (PD) * Loss Given Default (LGD)

This can also be expressed as:

ECL = EAD * PD * LGD

The calculation is grounded in assessing the probability of default (PD), loss given default (LGD), and exposure at default (EAD). The model requires businesses to evaluate credit risk over time and adjust provisions accordingly. LGD represents the share of losses, specifically the actual loss of receivables when a customer defaults, which is expected to be unrecoverable from assets during insolvency proceedings.

Examples (1 For Calculation)

Let us use a few examples to understand the topic.

Example #1

Imagine a bank has the following information for a loan it issued:

- Exposure at Default (EAD): $100,000

- Probability of Default (PD): 5%

- Loss Given Default (LGD): 40%

The Expected Credit Loss (ECL) using the formula:

ECL = EAD * PD * LGD

ECL = $100,000 * 5% * 40%

ECL = $100,000 * 0.05 * 0.40

ECL = $2,000

In this example, the Expected Credit Loss (ECL) for the loan is $2,000. This means the bank should set aside $2,000 as a provision for potential losses on this loan.

Example #2

An example of ECL is illustrated by the recent survey conducted by the International Association of Credit Portfolio Managers (IACPM), which found that portfolio managers at major global financial institutions expect credit conditions to worsen in Q3. The survey included 144 financial institutions and indicated an increase in anticipated corporate defaults and wider credit spreads. The Aggregate Credit Default Index dropped to minus 44.1, signaling higher defaults amid rising interest rates and persistent inflation. Despite concerns about geopolitical tensions, most respondents do not foresee recessions in the U.S. or other regions. This outlook highlights the importance of Expected Credit Loss (ECL), which helps institutions prepare for potential credit risks associated with these challenging conditions.

Example #3

An example of ECL is its application in the context of the COVID-19 pandemic, which led to a rise in corporate credit losses. Financial institutions may have absorbed these losses or passed them on to taxpayers. Research from the Bank for International Settlements indicated that corporate bankruptcies could triple compared to pre-crisis levels, impacting the financial system's stability. ECL helped banks estimate and manage potential losses from corporate debt, particularly in sectors like retail and transportation, which were severely affected by the economic downturn. By using ECL, financial institutions proactively prepared for future credit risks, ensuring their resilience amid an uneven recovery.