Table of Contents

What Is Fama-MacBeth Regression?

The Fama-MacBeth regression examines factors and their pricing power in an asset return's cross-section. It is based on the idea that a linear relationship exists between stock returns and market betas. The relationship is expected to explain the cross-section of returns at any given time.

Fama-MacBeth's two-step regression method was initially used to test the Capital Asset Pricing Model (CAPM) in asset pricing. The model aims to ascertain the risk premium related to exposure to various risk factors. This has shaped the understanding of the connection between risks and returns in the stock market and has been significant in finance.

Key Takeaways

- The Fama-MacBeth regression is a technique for estimating the parameters of asset pricing models, such as the CAPM (capital asset pricing model).

- It was developed by Eugene F. Fama and James D. MacBeth (1973). The method estimates the betas and extra returns that investors desire in exchange for accepting risk for all possible risk factors that could impact asset values.

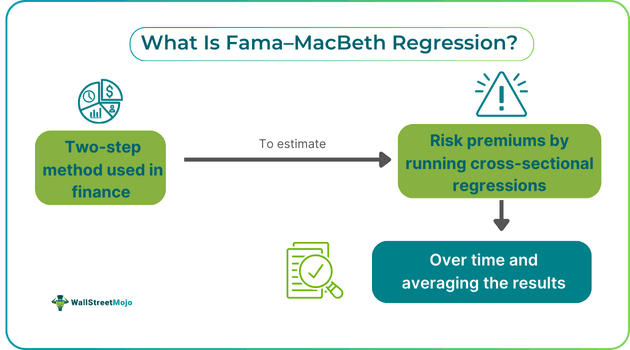

- The method generally involves only two significant steps: the time-series approach and the cross-sectional approach.

- Researchers can determine the risk factors relevant to explaining the cross-sectional variations in asset returns.

Fama-MacBeth Regression Explained

The Fama-MacBeth regression is a technique for estimating the parameters of asset pricing models like the CAPM (capital asset pricing model). The method estimates the betas and extra returns that investors desire in exchange for accepting risk for all possible risk factors that could impact asset values. It was developed by Eugene F. Fama and James D. MacBeth (1973).

The method is a crucial tool for empirical analysis and is frequently used in finance and accounting research. This approach entails performing time-series regressions for each asset against risk indicators, averaging the results to create a cross-sectional regression. Researchers can examine the pricing power of numerous components in the cross-section of asset returns using this method.

Through the evaluation, researchers can determine the risk factors relevant to explaining the cross-sectional variations in asset returns. They can better comprehend the market's risk-return relationship and create more precise asset pricing models by evaluating the betas and risk premiums for each relevant risk component. Beta estimates the returns of an asset's sensitivity to fluctuations in the general market and reveals the systematic risks involved. Similarly, Investors should be aware of the various risk premiums since doing so can enable them to manage their portfolios better and make educated investment choices.

Steps

The method generally involves only two major steps, and they are discussed below:

- Step 1 - The first step involves using a time series approach. In this step, individual asset returns are regressed against one or more risk factors to obtain the return exposures to each factor (often referred to as betas, factor loadings, or factor exposures).

- Step 2 - The second step utilizes a cross-sectional approach. All asset returns are regressed against the asset betas obtained through the time series approach from the previous step. Then, the risk premiums for each of those risk factors are obtained. After averaging these coefficients once for each element, Fama and MacBeth determine the anticipated premium over time for a unit asset's exposure to each risk factor.

Interpretation

Fama's classic assumptions for the Fama-MacBeth regression were two-fold: first, that each period is independent, and second, that the joint distribution of returns is multivariate normal. These assumptions were made to ensure that any regression of returns on returns was well-specified and that the results would be reliable and accurate.

Advantages

In asset pricing theories, risk factors are considered while estimating asset returns. These factors may be macroeconomic or microeconomic. Macroeconomic factors include unemployment and consumer inflation. Microeconomic factors include factors such as the various methods employed in accounting procedures and the other financial metrics employed by the firms. Apart from these, firm size also plays an important role. The Fama-MacBeth two-step regression method is useful for determining how appropriately these risk factors account for asset or portfolio performance.

Some of the potential advantages of using the method involve:

- Estimation of the risk-return relationship: The regression analysis helps assess the risk relationship between an asset and its expected return. This helps investors develop better models for asset pricing.

- Multiple risk factor analysis: The process involves looking at various risk factors associated with the asset. The involvement of multiple factors and analyzing them helps select the most relevant ones to explain the cross-sectional variations to determine asset pricing models.

- Insights into market efficiency: It provides insights into financial market efficiency by assisting researchers in determining whether or not specific risk factors are mispriced. Investors attempting to identify possibilities for profitable transactions may find this information beneficial.

- Helps investors: The beta and risk premium analyses can help investors be more aware of how their portfolio returns are streamlined. This may help them strategize timely to avoid losses and plan better for the future. In short, they help make better investment decisions.