Table of Contents

Introduction

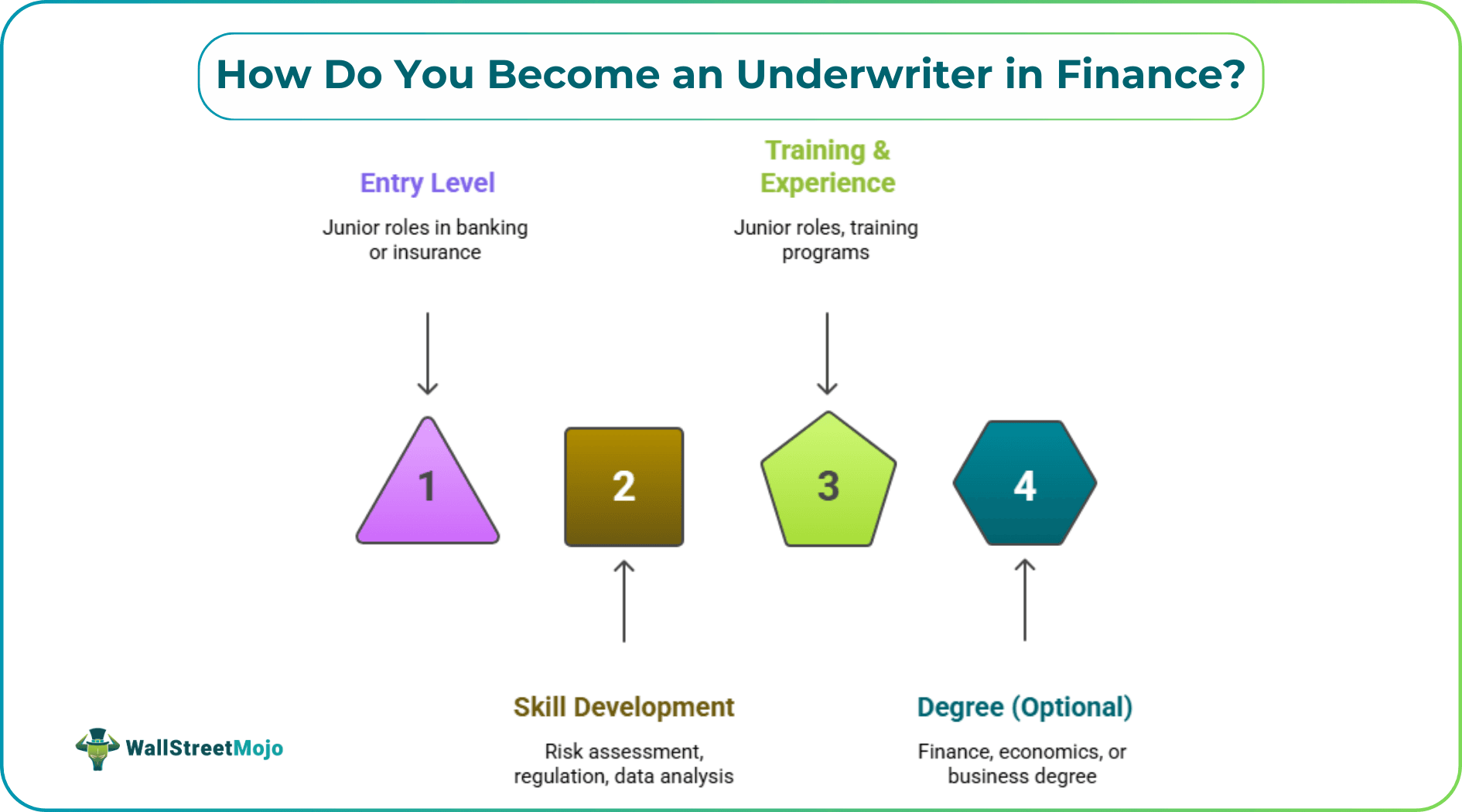

To become an underwriter in finance, you usually start with strong GCSEs and A levels, gain entry level experience in banking or insurance, and build your skills in risk assessment, regulation and data analysis.

Many people begin in junior roles such as underwriting assistant or credit analyst, then progress through training and experience. A degree in finance, economics or business can help, but it is not always essential.

What matters most is learning how to assess risk, apply policy rules and make balanced decisions. In the UK, outstanding residential mortgage lending exceeds £1.6 trillion, which shows how important skilled underwriting is to the wider economy.

What Qualifications Help You Start a Career in Underwriting?

There is no single route into underwriting, but employers look for good numeracy and communication skills. GCSEs in maths and English are important, and A levels in business or economics are useful. Some underwriters hold degrees, yet many enter through apprenticeships or trainee schemes. The UK government has a strong list of apprenticeships you can do in underwriting.

Professional qualifications can support career growth once you are in the role. Employers in consumer finance, mortgages and insurance often fund further study. Ongoing learning is important because underwriting rules and regulations change over time.

What Skills Do You Need for Successful Underwriting?

Strong numerical ability is essential in underwriting. You must review income, expenditure, credit history and risk scores with care. Attention to detail matters because small errors can lead to large financial losses.

Communication is also key in underwriting. You may need to explain decisions to brokers, sales teams or senior managers. Around 70% of UK lenders now use automated credit scoring systems, so underwriters must understand both data systems and human judgement. Being comfortable with technology is therefore vital.

How Does Underwriting Work in Consumer Finance?

Underwriting in consumer finance focuses on unsecured lending such as personal loans, short bad credit loans, credit cards and car finance. Decisions are often high volume and time sensitive. You rely heavily on credit reports, affordability checks and internal scorecards.

This type of underwriting is often a starting point for many careers. It teaches consistency, speed and regulatory awareness. You learn how to balance risk and customer needs within clear policy guidelines.

What is Different about Mortgage Underwriting?

Mortgage underwriting is more detailed and involves larger financial commitments and this overlaps with other types of finance including bridge finance, business finance, asset finance and development finance.

When underwriting secured lending, you assess income stability, employment history, deposit size and property value. Cases can take longer because the sums involved are higher and the risk lasts for many years.

The demand for mortgage underwriting is strong and you receive such a variation of applications, that each day can be quite unique. Lenders must follow strict rules to ensure loans are affordable, making careful document review and sound judgement essential.

How Does Underwriting Operate in Insurance?

Insurance underwriting focuses on assessing the likelihood and cost of future claims. Instead of affordability, you measure risk exposure. This may involve analysing health information, property details or business operations.

Insurance underwriting relies heavily on statistical models and historical claims data. The insurance sector contributes about 10% of UK GDP, which makes it a major employer of underwriters and there are a lot of opportunities in this area, with courses available from the Chartered Insurance Institute.

How Can You Progress in an Underwriting Career?

With experience in underwriting, you can move into senior roles, team leadership or specialist risk positions. Some underwriters shift into compliance, product development or risk management.

Progress depends on accuracy, consistency and good judgement. Over time, strong underwriting decisions build trust within an organisation. By developing technical knowledge and staying aware of regulation, you can build a stable and rewarding career as an underwriter in finance.