The Financial Cost of Manual Loan Processing and How Automation Fixes It

Table Of Contents

Introduction

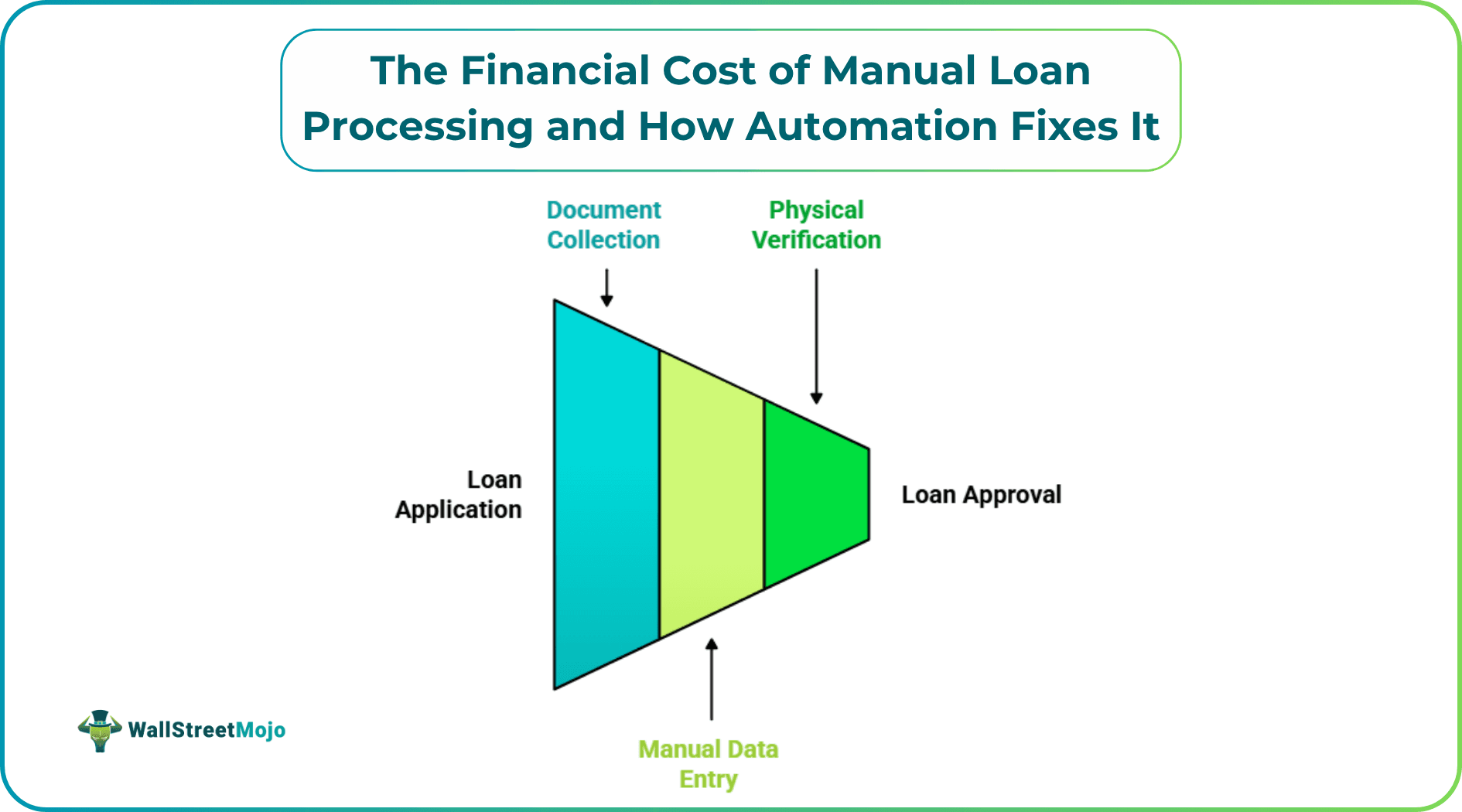

Manual Loan Processing refers to the conventional, human-centric sequence of document collection, manual data entry, and physical verification required to move a loan from a funding application.

The net interest margin of any lender is mainly determined by operational efficiency in the high-interest environment of 2026. In the case of institutions that continue to use the old-fashioned "stare and compare" techniques, the Profitability of the loan itself is often being cannibalized by the Cost per Acquisition (CPA) and Operational Overhead.

Key Takeaways

- Manual processing results in a large error tax that burns institutions.

- The largest aspect of the loan origination costs is Labor Costs.

- Automation offers Scalability without a linear growth in overhead.

The Mechanism of Transition: How Does Loan Processing Automation Work?

The digitization process consists of an organized technical process eliminating human latency at every node:

- Ingestion: Unstructured data (PDFs, JPGs, Scans) is received by the loan document processing software through a secure borrower portal.

- Extraction: Advanced Optical Character Recognition (OCR) and Machine Learning (ML) can extract crucial financial variables, along with Gross Income, Debt-to-Income (DTI), and Credit Scores.

- Checking: The gadget compares extracted statistics with outside databases (e.G., payroll companies or the tax government) using an API.

- Decisioning: The pre-defined risk parameters are used to give an immediate approval/deny/refer.

Quantitative Analysis: The Processing Efficiency Formula

The effect of automation calculated by lenders is based on the formula of the Efficiency Ratio:

Processing Efficiency =Total Operating Expenses/Number of Loans Funded

In a manual world, the Labour Costs and Error Correction Fees are still high, resulting in a low total efficiency score.

Real-World Application: Loan Automation in Practice

Case Study: Apex Lending Corp Performance Metrics

Take the case of Apex Lending Corp, which receives 500 mortgage applications every month.

- Manual Scenario: Apex employs 10 processors at $5,000/month each. The total exertion fee is $50,000. The value in line with the software is $100.

- Automated Scenario: Apex implements an AI-driven machine costing $five,000/month and keeps 2 senior processors for exception handling ($10,000). Total value is $15,000.

Result: Apex will save 70% of operational capital by cutting the amount spent on each application by an average of 100 to 30 dollars.

Comparative Framework: Manual versus Automated Processing

Juxtaposing the Legacy Framework and the 2026 Automated Standard

| Feature | Manual Processing | Automated Processing |

|---|---|---|

| Data Entry | Human-led (High Error Risk) | AI-driven (99% Accuracy) |

| Turnaround Time | 5–10 Business Days | < 2 Hours |

| Scalability | Requires New Headcount | Elastic (API-based) |

| Compliance | Manual Sampling/Audits | Immutable Digital Trail |

Strategic Assessment: Advantages & Disadvantages

Evaluating ROI and Technical Constraints

Advantages:

- Reduction of Cost: Reduces the Cost to originate drastically.

- Fraud Mitigation: AI identifies metadata abnormalities in the documents that are not visible to people.

- Employee Retention: Enables employees to work on Relationship Banking and not data entry.

Disadvantages:

- Initial Capex: It will need capital investment upfront for software integration.

- Technical Debt: Bank cores. Legacy bank cores might need a middleware to access the new APIs.

Future Outlook: The Role of Generative AI in 2026

By 2026, the lending industry will be out of basic OCR. Generative AI is now utilized by modern systems to provide a summary of complex disclosures in the law and give borrowers real-time and conversational updates on their application. This Information Gain guarantees that the lender is not merely a financial supporter, but a hassle-free service platform.

Frequently Asked Questions (FAQs)

Are the chances of default raised through automation?

Does automated processing comply with the GDPR/CCPA?

What is the average ROI of this software?

Recommended Articles

The Evolution of Modern Lending Infrastructure

The financial statistics prove that the territory of paper-based lending has come to the logical conclusion. Using advanced loan document processing software, it would make the back-office of an institution a competitive engine rather than a cost center. The credit market winners going forward in 2026 would be those that emphasize Data Integrity, Speed, and Operational Efficiency.