Table of Contents

What Is A Microfinance Institution (MFI)?

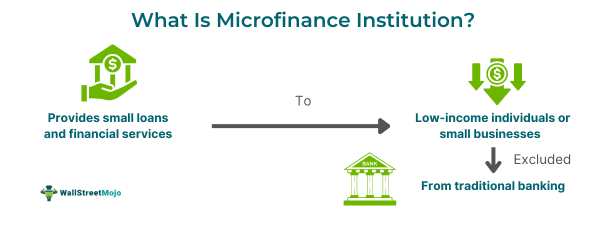

A microfinance institution (MFI) refers to a financial entity providing essential banking services like small savings and loan accounts to small businesses and individuals uncovered by traditional banking. They aim to empower poor individuals to achieve financial independence through products like microinsurance and microloans, along with business and financial literacy.

MFIs have emerged mostly in developing nations to help poor people and the economy. These institutions focus on low-income groups and provide funds at lower interest rates than traditional commercial banks. MFIs promote self-help and joint liability groups to cater to underbanked communities and promote entrepreneurship using innovative banking models.

Key Takeaways

- Microfinance institutions offer basic financial services to individuals and small businesses, aiming to empower poor people through microinsurance, microloans, and business and financial literacy.

- Their features are providing micro-loans to low-income groups in small amounts, with short-term, collateral-free, higher extended repayment frequencies, and for income generation.

- It provides easy access to financial services to underserved populations, but borrowers face heavy financial burdens due to the higher rate of interest.

- It serves primarily the lower-income class of individuals and small businesses, while commercial banks serve all types of customers.

Microfinance Institution Explained

A microfinance institution (MFI) is a financial organization that offers microloans and various financial services to individuals who lack access to conventional banking systems. Their services are tailored to meet the needs of small businesses and low-income populations to achieve financial inclusion. MFIs are designed to address the challenges faced by traditional banking and financial industries, providing sustainable and affordable lending options.

These are the different types of microfinance services:

- Microloans: Unsecured loans provided to individuals to help them eventually qualify for traditional bank loans.

- Micro-Savings: Savings accounts that allow entrepreneurs to save without a minimum balance requirement, promoting financial discipline and growth.

- Micro-Insurance: Insurance products with lower premiums are designed to cover borrowers of small loans, offering protection similar to conventional insurance but at a more affordable rate.

The following are the loan distribution methods:

- Joint Liability Group (JLG): A JLG consists of 4-10 individuals who apply for loans collectively. Each member guarantees the repayment of loans for the others, thereby reducing the lender's risk.

- Self-Help Groups (SHGs): SHGs are formed by micro-entrepreneurs with similar socioeconomic backgrounds. These groups save small amounts of money regularly in a shared account. The collective savings can be used to provide loans to members, leveraging peer pressure and mutual support to ensure timely repayment and responsible credit use.

Let's understand the objectives of MFIs:

- Encouraging participants to grow their businesses, create more jobs, and adopt innovative technologies.

- Helping first-time business owners acquire new skills and improve existing business operations.

- Collaborating with NGOs to provide training, support, and development opportunities for members of JLGs and SHGs.

- Establishing digital banking services in partnership with banks to provide SHGs with updates on both financial and non-financial activities.

Features

All the MFIs have the following features:

- Low-income groups flock to them for loans.

- All the loans provided to the borrowers have the characteristics of small amounts or microloans.

- They provide short-term loans.

- The MFIs need no collateral to extend loans to the borrowers.

- The frequency of long repayment of these loans remains higher.

- Most of the borrowers take loans to generate income.

Examples

Let us use a few examples to understand the topic.

Example #1

An online article published on 6 June 2024 discusses the recognition of Amanah Ikhtiar Malaysia (AIM) as the best MFI in Malaysia. Deputy Minister of Entrepreneur Development and Cooperatives, Datuk R. Ramanan, praised AIM's Managing Director, Mohamed Shamir Abdul Aziz, for receiving the National Leadership Icon Award 2024 for Microfinance. This recognition highlights AIM's efforts in empowering micro-enterprises, aligning with the MADANI Economy and the National Entrepreneurship Policy. In 2023, AIM disbursed RM2.6 billion to 320,000 microentrepreneurs and RM50 million to Indian women entrepreneurs through the PENN initiative. The award also acknowledged KUSKOP's role in facilitating funds and training for entrepreneurs.

Example #2

Let us assume that an MFI named Sundive Finance operates in the rural town of Old York. Martha, a local retailer, needs $5000 to expand her retail shop's inventory. She approached Sundive Finance for a collateral-free loan. Given her business's profitability and longevity, the MFI grants her the loan.

With the loan, Martha adds new products and grocery items to meet the increasing local demand. As her business grows, she repays the loan in small weekly installments of $100. By the end of the year, her business has grown significantly, enabling her to send her children to the best government school with a hostel facility. This success is attributed to the financial training and assistance provided by the MFI.

Advantages And Disadvantages

Let us use the table below to understand the pros and cons:

| Advantages | Disadvantages |

|---|---|

| Underserved populations get easy access to financial services. | Borrowers come under heavy financial burden due to the higher rate of interest. |

| Loans can be tailored as per the needs with better repayment structures. | Borrowers tend to avail of successive loans due to their over-indebtedness. |

| Entrepreneurs get easy loans to expand or start businesses | Broader socioeconomic conditions like education or healthcare are little to minimal affected by it. |

| Helps in financial inclusion of unserved and unbanked populations. | They get a lower spectrum of services with a chance to become over-stressed with loans. |

| Has succeeded in promoting and empowering women's entrepreneurship, helping them assist their families. | It lacks diversity and adds strong loan repayment emphasis, affecting borrowers' mental health. |

Microfinance Institution vs Commercial Bank

Although both offer financial services to people and businesses, they have certain differences, as listed below:

| Microfinance Institution | Commercial Bank |

|---|---|

| Serves primarily the lower-income class of individuals and small businesses. | All types of customers come under its ambit of services. |

| Offers collateral-free small loans like microfinance institutions in India, Kenya, and the Philippines. | Offer large loan amounts that need collateral. |

| Serves to finance income-generating works and micro-enterprises. | It offers loans for all purposes as allowed under conventional banking. |

| Their primary functioning is lending, but they also offer savings accounts to some. | Offers a huge variety of deposit services like savings and checking. |

| It may be regulated by specialized MFI regulatory authorities or even central banks. | Are regulated solely by central banks. |

| Social collateral and group lending are its hallmarks. | Has diversified loan products portfolio and complex management systems. |