Nvidia Records Explosive Growth Amid Macro Imbalance

Table Of Contents

Introduction

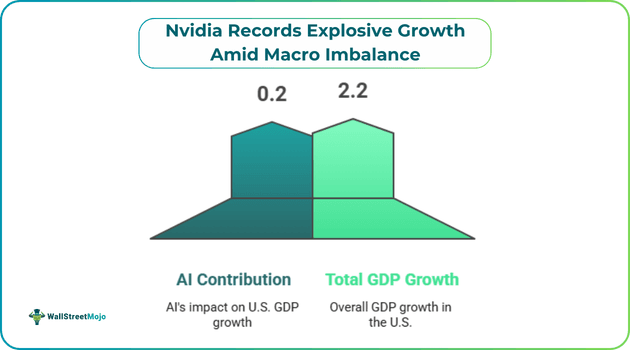

Viewed from a macroeconomic perspective, the AI sector’s dynamics appear more nuanced than the rapid rise in technology companies’ market capitalization suggests. It is estimated that the contribution of AI to U.S. GDP growth last year was only about 0.2 percentage points out of a total of 2.2%. A significant part of U.S. cloud giants’ capital expenditures flows abroad, primarily to Asia, where production of accelerators and server equipment is concentrated. As a result, a paradox emerges: the financial boom is centered in the United States, while much of the production’s value added accrues to Taiwan and other countries in the region.

Against this backdrop, Nvidia's financial results show almost exponential dynamics. Since the introduction of ChatGPT, its server revenue has increased approximately 13 times, and by the end of the last quarter, the total turnover reached $68.1 billion (+73% YoY). The data center segment generated $62.3 billion, which is almost 92% of the total quarterly revenue. By the end of the year, the company generated $215.9 billion in revenue and $117 billion in net profit, while the concentration of customers increased, with the two largest customers accounting for more than a third of revenue. The market still accepts this structure as a given, but it increases Nvidia's dependence on the investment budgets of a limited number of hyperscalers.

In the context of the report's publication and macro estimates, volatility in emini futures increases markedly, precisely following news on AI infrastructure. Even retail traders are pricing in not only Nvidia’s recent earnings and those of other AI beneficiaries, but also future AI investment. In fact, the futures market increasingly serves as a leading barometer, reacting faster than the stock market to concerns about the durability of the investment cycle and signs of cooling demand, while also factoring in expectations of a potential Anthropic IPO and an OpenAI IPO expected later this year.

At the same time, the geography of technological sovereignty is beginning to shift. During the final optimization of its new V4 model, China's DeepSeek prioritized the local accelerator suppliers, such as Huawei, although previously similar stages were associated with Nvidia. Formally, this is driven by faster optimization processes and the desire to improve the efficiency of models based on local hardware, but strategically, the move reflects China's policy toward technological independence. At the same time, the U.S. authorities keep closely monitoring the potential use of Nvidia's latest accelerators in Chinese projects, increasing uncertainty for global supply chains.

Financially, this means that the AI cycle is becoming not only an investment cycle but also a geopolitical one. The United States is increasing capital spending on infrastructure, but the effect on domestic GDP remains limited, with production and export gains concentrated in Asia. Nvidia reported record results and forecasts revenue of $78 billion for the current quarter, excluding the Chinese market, which itself points to a shift in market structure.

Thus, a gap emerges between market expectations and macroeconomic reality. Investors are financing a large-scale infrastructure cycle that is already generating hundreds of billions of dollars in revenue for accelerator manufacturers, but its multiplier effect on the broader economy remains limited and difficult to measure. The question is whether AI will become a driver of sustainable performance in the coming years, or will it remain primarily a source of windfall profits for a narrow range of computing power providers.