Revocable vs. Irrevocable Trusts: A Data-Driven Guide for 2026

Table Of Contents

Introduction

Estate planning is becoming increasingly complex, and trusts are at the center of the conversation. Recent industry data shows that discretionary trusts generated over 81,000 inquiries on major technical platforms, outpacing even pension-related questions.

Advisors now see trusts as more than tax tools—they're essential to sophisticated wealth transfer. With the 2026 TCJA sunset looming, individuals must rethink asset protection strategies. Experts advise reevaluating trusts before the federal estate tax exemptions shift. Choosing between a revocable and irrevocable framework isn't just paperwork; it changes your control, tax exposure, and probate risk.

What's Driving Trust Adoption in 2026

Despite the financial protections trusts offer, 47% of adults over 55 still don't have a basic will or trust. This means many families remain unprotected, even as modern challenges—like rising nursing home costs, blended family dynamics, and longer life expectancies—demand more structured estate planning. Families can benefit from living trusts to address these issues and avoid unnecessary litigation, as local data shows.

Shifting demographics make this even more urgent. Industry reports show that 36.2% of newly drafted wills now include at least one trust, highlighting a shift toward long-term asset stewardship. The legislative landscape in 2026 is accelerating this trend. Current federal exemptions are historically high, limiting estate tax concerns for many families, but once the TCJA sunsets, that safety net shrinks.

Financial advisors now prioritize probate avoidance, asset protection, and state tax mitigation over tax avoidance alone. Establishing clear, legally binding trust entities is more important than ever.

Revocable Trusts: Keeping Control While Bypassing Probate

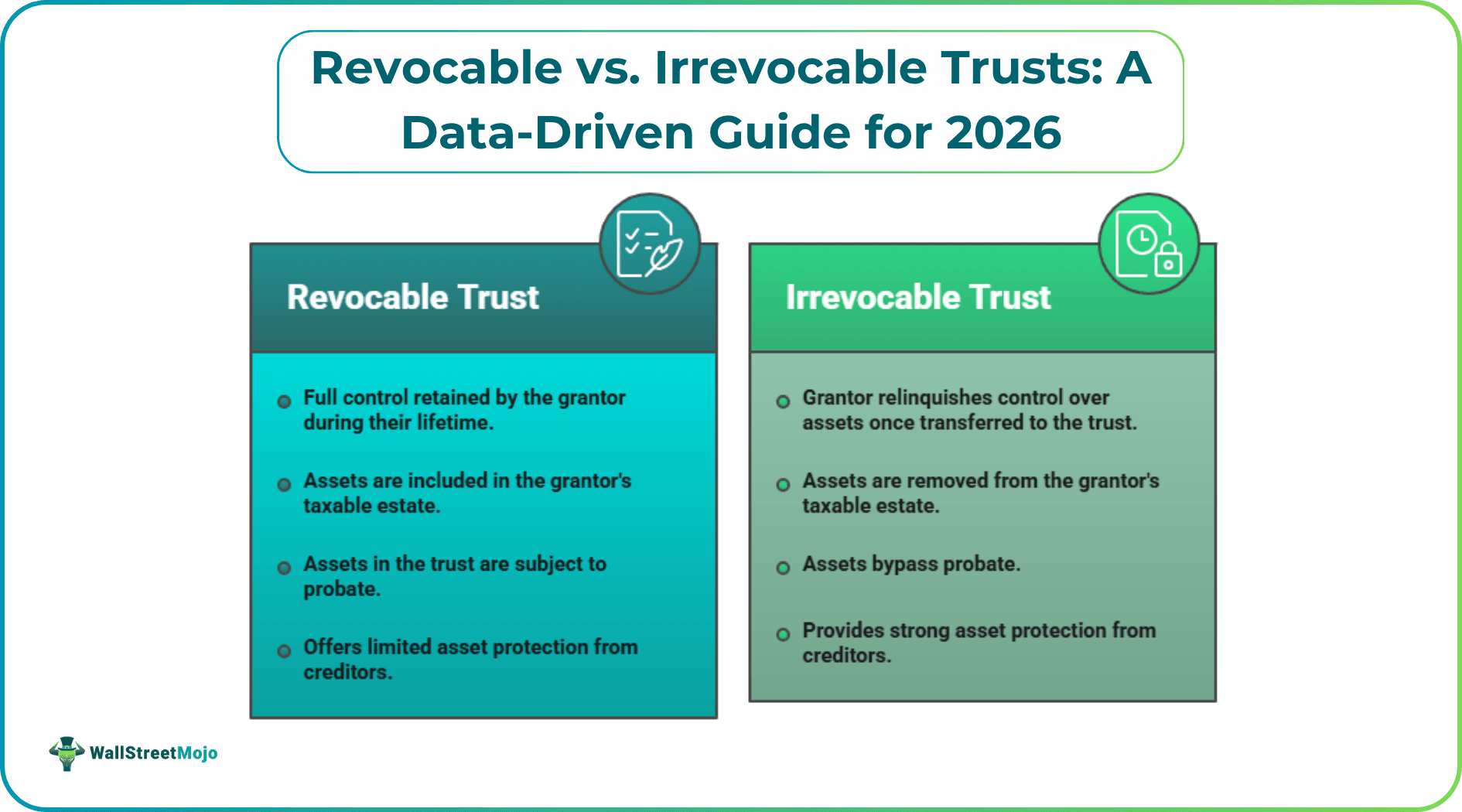

A revocable trust (often called a living trust) gives the creator full authority to alter, amend, or dissolve it during their lifetime. Investors gravitate toward this structure because it lets them maintain uninterrupted control over their financial portfolios. The creator, legally known as the settlor, typically names themselves as the primary trustee, which means they can buy, sell, or trade trust assets exactly as they would on their own.

The main financial benefit is avoiding probate, which is public, slow, and expensive, often causing significant delays for beneficiaries.

Take Arizona as a concrete example. State statutes trigger probate if personal property exceeds $75,000 or real estate exceeds $100,000. Even straightforward, uncontested cases take six to twelve months to clear the court system and routinely cost families upward of $6,500 in attorney fees alone.

Navigating these state-specific thresholds takes precise legal structuring. For anyone setting up an Arizona living trust, consulting localized experts helps make sure assets are properly funded and titled so they seamlessly bypass probate. That gives successor trustees immediate access to capital if the settlor becomes incapacitated or passes away.

One step you can't skip: proper funding. A trust controls only assets that have been retitled in its name. Property funded into a trust bypasses court appointment requirements, letting families manage real estate and investment accounts without interruption.

Irrevocable Trusts: Asset Protection and Tax Savings

An irrevocable trust works on a fundamentally different premise. When you establish one, you're generally giving up direct control over the assets in exchange for strong legal and tax protections. Once funded, the settlor can't easily amend, rewrite, or dissolve it. Because the settlor no longer legally owns the transferred assets, the IRS removes that capital from the individual's taxable estate entirely.

Historically, irrevocable trusts were seen as overly rigid. But modern legislative updates have given wealth managers new tools to adapt these entities over time. For instance, the updated Maryland Trust Act expands "decanting" and non-judicial settlement agreements. Decanting allows a trustee to transfer assets from an outdated trust into a new one with better administrative terms. That flexibility matters when older trusts impose unnecessary tax complexity or governance constraints on beneficiaries.

Advisors are also reviewing legacy irrevocable trusts to address state fiduciary income taxation, which can trigger steep liabilities if a family relocates across state lines. Here are some of the most common reasons people set up irrevocable trusts:

- Estate tax reduction: Removing high-appreciation assets from the taxable estate before the 2026 tax code sunsets

- Medicaid planning: Shielding core assets from nursing home spend-down requirements while qualifying for government long-term care assistance

- Creditor protection: Insulating family wealth from targeted litigation, bankruptcy, or divorce proceedings

- Special needs provision: Structuring supplemental income for dependents with disabilities without disqualifying them from federal aid.

How Revocable and Irrevocable Trusts Compare

Wealth preservation comes down to weighing your immediate need for capital access against your long-term desire for tax insulation. Picking the wrong vehicle can mean irreversible tax liabilities or frozen family assets. And tax law updates constantly shift the math. Accountants are publishing guidance on how changing IRS rules affect individual deduction thresholds and trust filing requirements.

Here's how the two structures stack up across core financial metrics:

| Feature | Revocable Trust | Irrevocable Trust |

|---|---|---|

| Asset control | Settlor retains full control to manage, spend, or reclaim assets | Settlor gives up direct control; managed by a designated trustee |

| Modification | Can be amended, rewritten, or dissolved at any time | Generally permanent; changes require complex legal processes like decanting |

| Probate avoidance | Yes, assets bypass probate entirely | Yes, assets bypass probate entirely |

| Tax liabilities | Assets remain part of the settlor's taxable estate; income taxed at the individual level | Assets removed from taxable estate; trust may file a separate return |

| Creditor protection | None; assets remain vulnerable to creditors and legal judgments | High; assets generally shielded from creditors and litigation |

To optimize these structures, financial professionals often pair trusts with concurrent wealth-transfer strategies. For example, the federal gift tax exclusion lets you transfer up to $19,000 per person annually without incurring tax. Combining annual gifting with a solid trust framework can aggressively reduce the size of an estate subject to probate or state-level taxation.

The administrative burden also differs between the two models. Irrevocable trusts require separate tax returns and distinct tax identification numbers. Revocable trusts simply use the settlor's Social Security number. That's a meaningful difference if you're trying to keep things simple.

Planning Your Wealth Strategy for What's Ahead

Revocable trusts let you maintain daily control and avoid probate, making them useful if you want flexibility and easy access to assets. Irrevocable trusts are designed for tax mitigation and asset insulation, so consider them if you prioritize protection and tax planning. With regulatory changes expected in 2026, regularly review your estate plan to ensure it stays aligned with your goals and situation.

Annual estate-planning reviews help catch issues with account titling and let you reassess strategies after major life changes. Getting the right trust structure in place now protects your family's capital against whatever legislative surprises come next.