Table of Contents

What Is A Secure Payment System?

A secure payment system refers to use of information technology and procedures of payment processing safeguarding financial and personal data from fraud and unauthorized access. It intends to provide security to payments, assure safe & fraud-less transaction experience to customers, build trust in the market and retain financial stability.

It complies with the strictest security frameworks established by governing authorities like ISO/IEC 27001, EMV, and PCI DSS to protect consumer's financial data. It incorporates different technologies like multi-factor authentication, biometrics, tokenization, OTP and encryptions to secure sensitive data and stop all unauthorized activities.

Key Takeaways

- A secure payment system utilizes payment processing protocols and technology to protect users' financial information and personal against unauthorized access and fraud.

- It aims at safeguarding payments, giving guarantees to clients a safe and fraud-free transaction experience, fostering market trust, and maintaining financial stability.

- Its components are - digital wallets, EMV chip cards, fraud detection systems, PCI DSS compliance, encryption, payment gateways, tokenization, multi-factor authentication, and secure data storage.

- It offers numerous benefits comprising quicker transactions, automated payments, customer trust, reduced costs, regulatory compliance, global payments, fraud prevention, security, improved customer experience, and contactless transactions.

Secure Payment System Explained

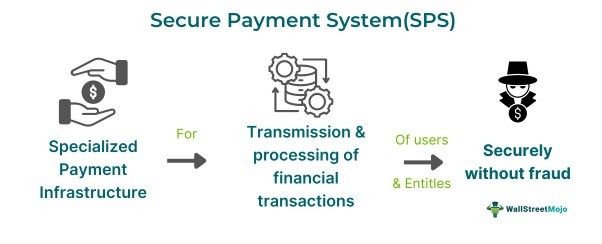

A secure payment system (SPS) represents the most specialized infrastructure ensuring the transmission and processing of financial transactions safely in the digital mode, mitigating unauthorized access and fraud. It deploys various technologies as its major components listed below to prevent fraud and data theft and safeguard users' sensitive personal and financial information.

It works by using elements like encryption, tokenization, authentication, and fraud detection mechanisms to safeguard customer data and protect financial information. When a customer starts a transaction, SPS encrypts data during transit, and then tokenization changes the sensitive information into zero-valued tokens. Various means, like 3D secure payment systems and biometrics, authenticate customers, preventing any fraud immediately. A secure e-commerce payment system can safeguard digital shopping spaces. However, other advanced fraud detection procedures examine transaction trends to find and block all suspicious activities.

It facilitates a secure and seamless payment experience for customers at minimal risk of expensive data breaches while protecting at every level. They have been adopted by every entity and business, like physical stores, online e-commerce platforms, and SAAS providers, in digital financial transactions safely. Food delivery services are no exception, where secure payment systems help prevent food delivery fraud and protect user transactions. Moreover, the integration of SPS gateways with the Point of sale (POS) systems has further enhanced the convenience and usability for consumers and companies. Finally, it has positively impacted the financial world by minimizing frauds, stabilizing markets, increasing financial inclusions and being a vital organ of the modern financial ecosystem.

Components

The nine components of a secure payment system are as follows:

- Encryption - It helps convert plain text information into a coded form, known as ciphertext, helping in thwarting unauthorized access.

- Payment gateways - They transmit payment information safely and securely between a processor or bank and a business or customer.

- Tokenization - It converts and interchanges sensitive payment information with less sensitive tokens, increasing security and decreasing the data breach risk.

- Multi-factor authentication (MFA) - It deploys multiple layers of use authentication before initiating and completing transactions like biometrics, one-time passwords and codes to give an extra level of security.

- Digital wallets - These wallets can store payment data and money securely removing the need for presenting account or card information for every transaction.

- EMV chip cards - Such cards employ microprocessor chips to produce unique transaction codes, leading to difficulties in counterfeiting payment cards.

- Fraud detection systems - They contain various means to detect fraud, like real-time transaction monitoring, machine learning and algorithms, besides other security measures.

- PCI DSS compliance - It ascertains that businesses follow a set security standard process to secure cardholder data during transactions.

- Secure Data Storage - It stores & protects all payment data involved in transactions, card and account data of consumers by encryption at rest and transit.

Examples

Let's work with a few examples to understand the topic.

Example #1

An article published on 20 July 2021 discusses the teaming of Opus Consulting Solutions with Noname Security regarding APIs for a secure payment system. Opus Consulting has created more than 350 payment systems worldwide. Such APIs have become quite important with the rise of mobile and cloud technology to integrate applications securely. Moreover, it has been estimated that APIs help in transactions worth $1.1 trillion annually.

Considering that APIs remain subject to cyber threats, the partnerships between these companies have offered successful diagnose and monitor their vulnerabilities across their lifecycle. Further, an agentless platform of Noname can examine and identify API traffic, giving extensive security in the absence of any additional burden to the infrastructure. Besides, the collaboration between Opus and Noname becomes significant in advancing secure payment techniques.

Example #2

Let us assume that Zenith City Corporation has offered a vibrant online marketplace called Zmart. Zmart utilizes the latest technology of payments with an extra layer of security called ZenPay. One of its customers, Zarita, bought a handcraft-based Vase from the Indoa pottery store listed on Zmart. For the purchase, Zmart's technology uses its algorithm to devise a one-time ecommerce token without using any information from the buyer's credit card, Zarita.

And that digital ecommerce token was sent to |Indoa for payment completion. As soon as Zarita authenticates her purchase using her fingerprint on her smartphone, ZenPay deducts the amount from her bank account. Thus, it helps the fund transfer to an India account without exposing her credit card details.

Benefits

Across the retail and purchase domain, one finds that it offers a platitude of benefits to all, as shown below:

- Security - It provides security to accounts from online fraud, financial data exposure, and privacy.

- Improved customer experience - It boosts the consumer experience as they can do transactions using digital payments quickly.

- Quicker Payments - It has become one of the hallmarks of the system as users can perform swift transactions and authorization automatically without much hassle.

- Automated payments - Users can now automate every kind of payment from their phones, like rent payments, utility and loans.

- Customer faith - It instills and strengthens customer trust in sellers because their payment details and transactions remain secure from fraud.

- Decreased costs - It has eliminated any need for the paper world, physical infrastructure or manual handling, leading to cost-cutting for both users and companies.

- Regulatory adherence - It enforces businesses' compliance with PCI DSS, helping with customer data, minuses data breaches, and containing unnecessary penalties or fines.

- Global payments - It has led to global trade expansion by way of accepting and receiving global payments in a business's currency without the hassle of delays, involving paper checks and other fees and costs related to international trade.

- Fraud prevention & Identity theft - These systems have inbuilt tools and techniques to detect frauds to prevent any data theft, privacy concerns and fraudulent transactions from taking place from customers' accounts.

- Improved efficiency & Contactless - Businesses and customers can both conduct all their transactions efficiently without any contact with the actual transaction method like checks, interactions with staff or being in queues.