Table of Contents

What Is Trading Mechanisms?

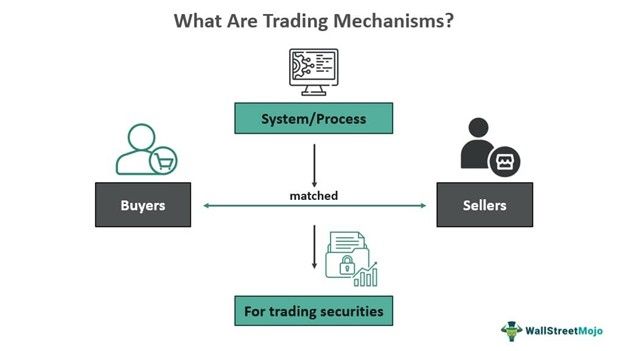

Trading Mechanisms refer to the guidelines and rules that individuals and entities participating in trading securities must follow to ensure the right buyer is matched with the right seller to carry out securities exchange. The mechanism acts as an element that demonstrates the capacity and capabilities of different exchanges in dealing with securities.

The mechanism sets the protocol, reflecting how trading happens and is accomplished on the security exchanges. It emphasizes and gives clarity on the market's microstructure, which in turn reflects the market's efficiency. This helps in conducting comparative studies on how market participants behave and act, helping determine the market quality.

Key Takeaways

- Trading mechanisms are rules and protocols employed in exchanges for the trading of securities.

- The mechanism is determined by various factors such as price discovery, order forms, market type, and transparency.

- The mechanism demonstrates the capacity and capabilities of different exchanges in dealing with securities.

- Trading mechanisms hold relevance and are defined by two broad forms of markets – auction market and dealers market.

- There are two major trading mechanisms: quote-driven and order-driven systems.

- In a quote-driven system, the dealers typically quote prices before the orders are submitted. In an order-driven system, traders usually submit their orders before the price determination happens.

Trading Mechanisms Explained

Trading Mechanisms in the securities market show how the securities are traded. They set the rules and regulations and define protocols that build robust trading platforms. Market participants are pretty serious about considering these mechanisms or designs, and hence, they keep adapting to the changing rules to ensure improvement in the platforms where trading is facilitated, thereby making them more competitive.

The trading rules are listed as the trading mechanism to guide the market in facilitating the proper exchange of securities and thereby boost market efficiency. When it comes to this mechanism, there are two categories of market in which it holds relevance. The first one is the auction market, commonly referred to as the limit order market. In such markets, the investors interact directly, and their bids and offers are recorded in a consolidated limit order book (LOB). The arrangement in the LOB is done with respect to the price priority, which means the higher bids are prioritized for execution, and the same goes for cheaper offers.

Another type of market that makes the presence of robust trading mechanisms worthy is the dealer market. Here, the investors can trade the bid and ask deals based on the prices that the intermediate channels post. These middlemen in the process are called dealers or market makers. No matter what kind of trading mechanism market participants come across, its version can easily be defined based on these two categories.

These mechanisms affect price discovery and the cost of trading in addition to the time it occurs. The time involved is referred to as a trading session, and it contains several phases, right from the pre-opening phase until the closing phase. These phases reveal the order types entered, altered, or deleted and the price at which they were executed.

Types

There are two major trading mechanisms in the securities market: quote-driven and order-driven systems.

#1 - Quote-Driven System

In a quote-driven system, the dealers typically quote prices before the orders are submitted. One example is the NASDAQ (National Association of Securities Dealers Automated Quotations, New York), where traders can obtain price quotations from market intermediaries who purchase and sell securities on demand. This is continuous; hence, the investor does not need to wait for their orders to be executed; the transaction happens between them and their dealer immediately. It is, therefore, referred to as a continuous dealer system and is often associated with a series of bilateral transactions and possible price differences.

#2 - Order-Driven System

In an order-driven system, traders usually submit their orders before the price determination happens. Here, the investors submit their orders through auction. The system is further divided into two types: periodic and continuous auctions. In periodic auctions, the traders' orders are batched or accumulated through multilateral transactions at one price (batch market). On the other hand, in a continuous auction, the traders submit orders to be immediately executed by the dealers on the exchange floor. It is addressed as continuous as the orders are executed immediately, and the price is determined by competitive bidding among the traders (crowd trading).

Examples

Let us consider the following scenarios to understand how having a robust trading mechanism helps:

Example #1

In May 2005, NASDAQ came up with a mechanism for determining the opening price called the Nasdaq Official Opening Price (NOOP). The new system took into consideration different types of orders, such as market-on-open orders, or OPG, open prior to 9:28 a.m., not-held market orders (DAY), and market orders (DAY) that open prior to 9:30 a.m. The day's associated single opening price, here, would be the reflection of the demands and supplies as the market experiences on opening. This example shows that trade sessions in the real world could help determine the prices.

Example #2

In August 2023, the Chinese stock market decided to bring about some changes in the trading mechanisms to improve market efficiency, thereby boosting investor confidence in the market. Shanghai and Shenzhen stock exchanges, as a result of this, agreed to allow investors to place smaller bids in the auction market and also improve trading mechanisms for exchange-traded funds (ETFs). They also said they would keep a watch on and study fixed price mechanisms to take control of the fluctuations that frequently happen for ETFs. Moreover, they decided to feature the trading rules in English so that they could be easily understood and ensure transparency.