Part of our Banking Services and Operations guide

What Is A Virtual Credit Card?

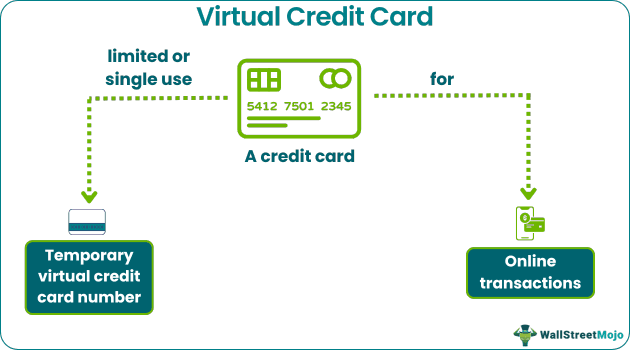

A virtual credit card, often referred to as a single-use card, is a digital payment method that provides a temporary credit card number for a specific transaction. Virtual credit cards are primarily used for online payments and serve as a secure alternative to physical credit cards.

The application of virtual credit cards for businesses and consumers is widely spread. The main purpose of this card is to provide seemingly convenient, hassle-free digital payments without any physical existence. It acts as an add-on card to their primary plastic money. In addition, it makes it convenient and easy to use for consumers. Also, there is full-proof security while conducting these transactions. However, some restrictions exist, as virtual cards cannot be used anywhere.

- A virtual credit card, also known as a disposable or single-use card, is a digital card designed for making secure advance payments during online purchases on e-commerce sites or through other online modes.

- These cards gained popularity in the United States in the early 2000s, with Discover and American Express being among the first card issuers.

- These cards typically have a 16-digit number valid for a limited time, usually 24 to 48 hours. Each merchant or store may have a different virtual card number.

- The issuance process for single-use cards is typically hassle-free, as verification is conducted online.

How Does A Virtual Credit Card Work?

Virtual credit cards are considered one of the safest payment methods. They provide a secure way for consumers to purchase with a single click on various e-commerce platforms. The concept of limited or single-use cards for businesses and individuals emerged in the early 2000s, with the credit card networks American Express and Discover being pioneers in this field.

The process of generating virtual credit card numbers can vary. Unlike physical credit cards, each virtual card number is unique to the specific merchant. For example, the virtual credit card number used for a clothing store purchase will differ from that used for a grocery store transaction. This uniqueness makes it more challenging for fraudsters to discover the card’s identity. Additionally, since virtual cards are stored digitally on devices such as smartphones, the risk of physical theft is reduced.

To apply for a virtual credit card, individuals can contact the issuer of virtual cards. Once the necessary Know Your Customer (KYC) and verification processes are completed, the card company or bank will issue the virtual credit cards online. Consumers can then use these credit cards to make online purchases and pay bills. Here are the steps to use a virtual credit card for a transaction:

- Enter the virtual card number on the payment site.

- Input the validity period and CVV of the card.

- Request an OTP (One Time Password) on the registered phone number.

- Enter the received OTP and submit the payment.

Single-use credit cards are connected to a physical credit card. In essence, they are a virtual form or replica of the primary credit card linked to the consumer’s bank account. In addition, it’s worth noting that virtual credit cards usually have a maximum transaction limit, which further helps mitigate the risk of fraudulent activities.

Examples

Let us look at some of the examples to understand them better:

Example #1

Suppose Sheldon wants to make some purchases online due to ongoing offers and discounts. However, he has a threat of fraudsters misusing his information and bank details. Therefore, he opts for a virtual credit card to make safe purchases. According to the instructions, Sheldon can use the credit card to make online purchases. However, this card has only single use with a limit the user decides.

So, if Sheldon wants to buy an oven from Amazon, he gets a virtual card number (4000 **** **** ****) that can be used only on this site. Once an item is selected, enter the card number and OTP. Likewise, if he wants to shop on the e-commerce platform Shopify, he will get another card number (4210 **** **** ****). As a result, the details of Sheldon remain disguised (unknown). However, in the end, the postpaid amount will get deducted from his primary bank account.

Example #2

According to a report, in 2021, the virtual credit card industry’s global market will be $3.36 billion. As a result, it will reach 25.9% between 2022 to 2030. Likewise, another report states that Western countries and the African continent are the fastest developing market. In contrast, European, Russian, and associated countries have a larger market base.

Benefits

Let’s explore the advantages of using a prepaid virtual credit card for businesses and consumers:

- Reduces Unnecessary Costs: Virtual cards help cut costs. From a business perspective, there is no need for paper receipts when individuals make purchases at physical stores. With virtual cards, online stores generate electronic bills, reducing paper waste. Moreover, the issuance cost of these cards reduces as the verification process takes place online.

- Increases Cash Flow: Virtual card availability encourages consumers to use them, increasing online spending. This benefits the card issuing company and merchants by generating a steady cash inflow.

- Easy Mode of Payments: Single-use credit cards enable convenient online payments, eliminating the need to stand in long queues. This makes it easier for individuals to purchase items.

- Maximum Security and Privacy: They offer enhanced security. They are designed for single use, meaning they have a one-time validity only for a specific merchant. If the buyer purchases from another store, the card number will change. This helps ensure the safety of user details. Additionally, users can freeze the card for added security.

- Cost-Cutting and Flexible Limits: Individuals can set their credit card limits to manage their budget effectively and reduce unnecessary business expenses.

- Rewards and Cashbacks on Purchases: Owners of prepaid virtual credit cards can earn various rewards and cashback for their purchases.

Virtual Credit Card vs Physical Card

Although consumers use both types to make instant purchases, they have differences. Let us look at them:

| Basis | Virtual Credit Card | Physical Card |

|---|---|---|

| Meaning | A credit card has its existence in the digital space (in online mode). | A physical card is a plastic card used in debit and credit transactions. |

| Purpose | To make credit payments securely in the online mode. | To make offline (in-store) transactions hassle-free. |

| Application or Usage | Only in online stores and e-commerce sites. | Both physical and online stores |

| Expiration | For one to two days | Physical cards are valid for a few years. |

| Fees | Usually, no fee is charged | A fee is involved during transactions. |

| Number of transactions | Individuals can incur only one transaction. | It can be unlimited until the limit crosses. |

Frequently Asked Questions (FAQs)

1.Are virtual credit cards legal?

Yes, this type of virtual card is legal. Banks and financial institutions offer them as a secure form of payment for online transactions, adhering to relevant regulations and laws.

2.Can a person get a refund from a virtual credit card?

Yes, a person can generally receive a refund from a virtual credit card. However, the refund process would depend on the policies of the card issuer or the merchant from which the purchase was made, similar to refunds with physical credit cards.

3.Can virtual credit cards be tracked?

It can be tracked to some extent. The transactions made with virtual cards leave a digital trail that can be monitored by the card issuer and potentially tracked by authorized parties for security and fraud prevention purposes. However, the specific level of tracking would depend on the card issuer’s policies and the applicable laws in the jurisdiction.

Recommended Articles

This has been a guide to what is Virtual Credit Card. We explain it with its benefits, comparison with physical card, and examples. You can learn more about it from the following articles –