Bike Loan Interest Rate Trends in India – What Borrowers Need to Know This Year (2025)

Table of Contents

Introduction

The bike craze in India has hit a new high after the reduced GST rates. India's bike loan interest rates in 2025 depend on several factors like the borrower's credit score, vehicle type, and lender. In India, the rates generally vary from approximately 8.5% to over 30% across banks and non-banking financial companies (NBFCs) like IDFC FIRST Bank, ICICI Bank, and L and T Finance.

Current Trends in Interest Rates (India, 2025)

The RBI’s repo rate directly influences bike loan interest rate trends in India. In 2025, it stood at 4.4% in a 50-basis-point cut. Thus, loan rates have become more competitive, and banks are offering low-interest loan rates.

Bike Loans: Bike loan interest rates in India often start from around 10.5% to 12% p.a.

Factors That Affect Bike Loan Rates

Several factors affect the interest rates for loans for bikes.

- RBI Repo Rate: A lower RBI repo rate encourages banks to reduce lending rates.

- Inflation: The RBI can maintain or cut rates when the inflation is below 4%,

- Credit Score: A CIBIL score above 750 secures lower rates for any type of loan including bike loans.

- Loan Amount and Tenure: Higher loans or longer tenures attract slightly higher rates.

#1 - Credit Score and History

When it comes to best bike loan offers India, a score of 750 is considered decent and boosts loan approval chances. With this score, you may also get better interest rates, flexible EMIs, and faster processing.

#2 - Income and Employment

Thise who provide loans look for stable employment and consistent income from the borrower. Frequent job changes increase risk, leading to higher rates.

#3 - Loan Details

When we notice bike loan interest rate trends in India, the interest on a bike loan is calculated based on the following:

- Principal amount

- Interest rate

- Loan tenure

#4 - Policy and Market Conditions

- The RBI reduced the repo rate in the first part of 2025 from 6.50% to 6.00%. This ideally lowers the interest rates on all loans, including bike loans.

- Policy adjustments resumed in 2025 to balance economic growth with stability, which may affect loan rates.

- Also, NBFCs and banks compete with each other in offering competitive current bike loan interest rates, especially in the growing two-wheeler loan market.

- The GST reduction in mid-2025 helped lower the effective cost of bikes, influencing bike loan interest rate trends in India.

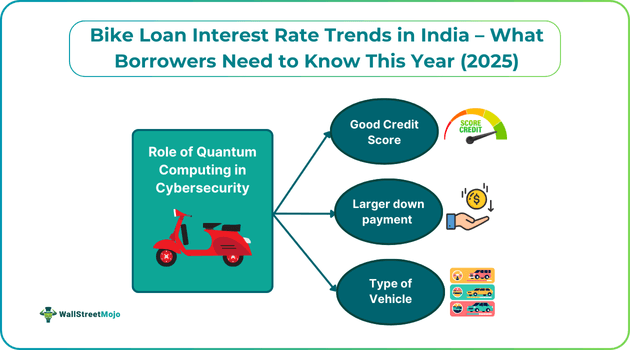

#5 - Other Borrower Factors

The other borrower factors which influence two-wheeler loan rates 2025 include:

- A strong credit score

- Stable employment and income

- Larger down payment and a shorter loan tenure

- Good relationship with lender

- Based on type of vehicle

Comparing Rates Across Banks or NBFCs

Banks are a reliable option for borrowers with good credit scores, while NBFCs are more flexible and can offer loans to individuals with slightly lower credit scores. One can use online loan calculators to compare rates from various banks and NBFCs and select the best offer. It is always smart to compare the two loan interest rate before applying for a bike loan. Let us compare the bike loan rates across different banks and NBFCs using a simple table.

| Bank or NBFCs | Interest Rate Range (p.a.) |

| ICICI Bank | 10.25% - 26.10% |

| Bank of India | -8.75% (April 2025) |

| L&T Finance | 7.99% onwards |

| HDFC Bank | 14.50% onwards |

| State Bank of India | 7.50% - 16.55% |

| Bajaj Finserv | 9.50% onwards |

How To Get the Best Bike Loan Rate?

To get the best bike loan rate in India in 2025, follow these options.

1. Keep your credit score high.

2. Make a larger down payment.

3. Choose a shorter tenure.

4. Always compare offers across banks, NBFCs, and fintechs, and negotiate.

5. Apply during festive or promotional schemes.

- Improve Credit Score: Punctually repaying any existing debts shows financial discipline and an ability to handle new debts. To improve credit score for a bike loan, one must always have zero to low debts with a history of consistent repayments.

- Pay a Higher Down Payment: A larger down payment reduces the loan amount for two-wheeler loan interest rates.

- Choose a Shorter Tenure: Longer tenures mean lower EMIs, but if budget permits, choose a shorter tenure to secure a lower rate.

- Compare and Negotiate: There are many institutions competing with each other to offer the best loan rates. Choose one where you can negotiate and get the best rate. Armed with competitive offers from other institutions, you can negotiate with lenders for better bike loan rates. Many are willing to offer lower rates to attract or retain customers.

- Use a Co-signer: A co-signer with a strong credit history and steady income can significantly increase the likelihood of the loan being approved.

- Maintain Banking Relations: Maintain good relations with your bank for a two-wheeler loan by timely EMI payments, a high credit score, and maintain transparency.

Mistakes To Avoid

Let us look at some mistakes to avoid when availing bike loans.

- Not researching banks or NBFCs: If you do not research and compare interest rates, fees, and terms across multiple lenders, you may not get the best offer.

- Read the fine print: Skipping over clauses about processing fees, penalty charges, or rate resets can lead to issues after availing the loan.

- Applying to too many banks or NBFCs simultaneously: Submitting multiple loan applications in a short span can lead to multiple credit inquiries, which may lower your credit score.

- Zero down payment: Opting for zero down means your entire bike cost gets financed, which often leads to higher interest rates or negative equity.

- No repayment plan: Not having a clear cash flow or repayment strategy increases the chance of default or missing EMIs.

Why Consider L&T Finance?

L and T Finance offer competitive rates starting as low as ~6.99% p.a. They provide flexible repayment tenures, making it easier to manage EMIs. Under their no Cost EMI scheme, customers can purchase bikes without any interest charges on the loan amount. Right now, they have introduced three new offerings called No Cost EMI, Prompt Payment Rebate, and the EMI Lite Festive scheme.

They have streamlined documentation and offer fast decisions. They have also announced attractive loan offers for their two-wheeler finance customers.

The EMI Lite Festive scheme is flexible and customer-friendly and allows them to pay just the interest portion of their EMI for the first two months, with no principal amount included. Thus, it follows the policy of buy in 2025 and pay in 2026.

Final Thoughts

In 2025, bike loans are still easy to get in India. Rates go low around 9% for good borrowers but can shoot up 25%+ if risk is high. RBI cut rates a bit, but not everyone will see that benefit. Best way is to check many banks/NBFCs, keep credit score clean, pay some money upfront, and watch for hidden fees. With planning and regular EMI, a bike loan can be cheap way to own a two-wheeler and also build credit.