Part of our Credit Concepts guide

What Is Credit Score?

A credit score refers to the scoring model used by credit companies to predict the ability of a borrower to pay the loan successfully by using their credit history. It forms the basis for accepting or rejecting a loan applied by a person in a bank or financial institution.

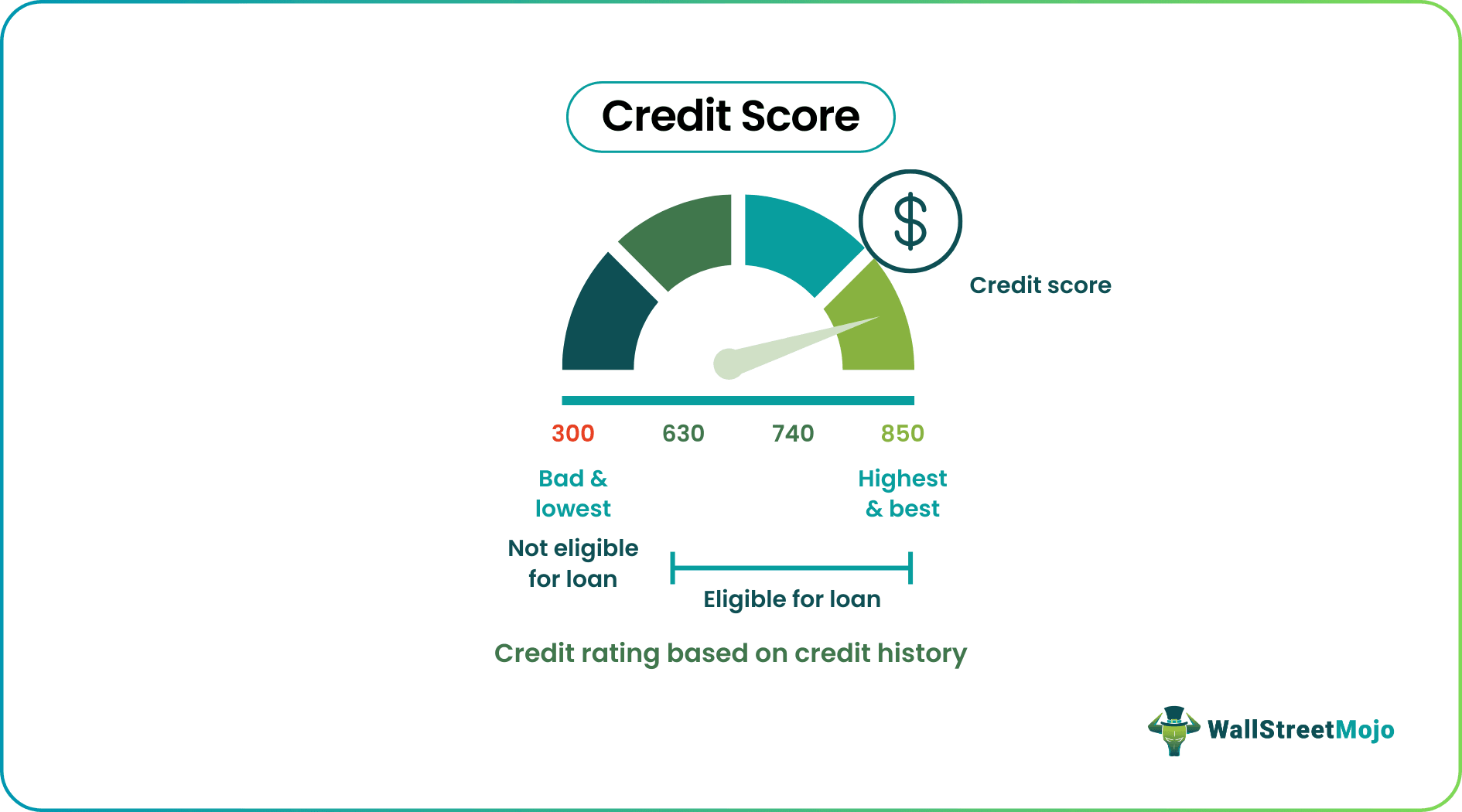

Usually, a three-digit number ranging from 300 to 850 gets calibrated to predict the borrower‘s risks. After that, it depends upon the credit rating model used by the credit rating agency and the credit repayment history of a borrower. A higher score means a better loan record and easier loan approval for a borrower. Hence, if an applicant’s score remains more than 630, the lenders accept the loan application; otherwise reject it.

- Credit scores are a mathematical representation of credit reports generated by agencies using statistical models to know a loan applicant’s creditworthiness.

- They help lenders decide the approval or rejection of loan applicants, with only high scorers getting approved and lower ones getting rejected.

- Timely repayments and lower credit utilization of credit cards form some ways to lower bad credit reports and improve credit scores.

- Every credit rating organization uses a scale of 300 to 850 to determine a person’s creditworthiness.

Credit Score Explained

A credit score is a mathematical representation of the creditworthiness of an entity by credit rating agencies using statistical models to assess past loan records. One assumes it to be the mathematical summarization of a person’s credit report that one obtains from past credit transactions called a credit report. FICO and VANTAGE have been two prominent credit scores provider in America.

The agencies put the entire loan record into various creditworthiness brackets in numerical scores ranging from 300 to 850. The score comprises various percentages of creditworthiness as below:

- Thirty-five percent of the score depends on the applicant’s payment history.

- Thirty percent of the score depends on the amount of loan currently held in a person’s loan account.

- The length of credit account accounts for fifteen percent of the score.

- Ten percent of the score comes from any new loan account applied for by the applicant.

- Rest ten percent of the score comes from the diversity in the loan mix of the individual.

Agencies obtain these rankings from three major credit bureaus – Equifax, Transunion & Experian. Hence, one person can have three different credit ratings.

As per the Equal Credit Opportunity Act of the US government, FICO and VANTAGE ratings do not consider the following information of a loan applicant:

- Age

- Color

- Ethnicity

- Race

- Religion

- Nationality

- Marital status

- Gender

- Salary

- Post

- Employer

- Location

- The interest rate on other loans

- Employment History

- Credit counseling

Moreover, credit ratings form an important part of deciding the loan eligibility of a person. Higher ratings mean robust creditworthiness and repayment history for easy loans, whereas low rankings mean bad credit reports and difficulty in loans. Scores below 640 get as bad, 640 to 740 becomes credit score good, and scores beyond 750 to 850 get exceptional.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

How To Check Credit Score?

One must check their credit ratings before applying for any loan from any lender. However, a credit score check may not always be free or convenient. Hence, let us know the means to check one’s credit-score as discussed below:

- Check the websites that offer free credit rating services online using a google search.

- Many credit card providers offer free credit rating services to potential clients so they can also use their services.

- Major credit reporting firms in America also offer credit scores to customers at a small charge.

- Even if someone still does not want to spend money on getting their credit rating, one must be aware that US federal laws mandate to provide it to everyone every year.

What Is A Good Credit Score?

Agencies rate credit rankings as good or bad based on the credit rating agencies’ cutoff. Hence, it differs from one rating agency to the other. Typically, the score ranges from 300 to 850 for every credit rating agency measuring creditworthiness. For example, for a FICO score, a good credit score ranges from 670 to 739. For Vantage Score, 661 to 780 has been considered good.

How To Improve Credit Score?

Nowadays, every individual or business requires credit from lenders to meet their extra-personal needs and grow their businesses. However, in such a case, the credit history may get tarnished due to untimely prepayment or mismanagement of funds. As a result, credit ratings deteriorate when loan rating agencies report. Hence, for any new loan, one will have to improve their bad credit ratings following the points below:

- First, get a free credit report from any credit rating agency and review any error related to the loan details. In case of error, one must immediately notify the CRA, which will help improve wealth scores, as happened in 26% of cases reported by the government.

- Set up loan repayment reminders to pay back loans on time.

- If possible, one must pay the bills twice every month instead of monthly.

- Be in constant touch with creditors for any issues.

- Avoid frequent loan applications within a short period.

- Avoid closing unused credit cards but close the newer ones for better credit ratings.

- Never pay charged-off debt accounts marked by the lender, as it may reactivate the old debt and lower one’s credit rankings.

- Make a habit of clearing the debt of that credit card with its credit limit used to the fullest to lower the credit utilization limit.

- Maximize the credit mix of the loan portfolio.

- Take a quick loan and repay immediately to improve one’s credit rating.

- Try to enlist oneself in a debt consolidation plan.

- One must also not become a co-borrower to frequent loans.

- Finally, one must ensure to use credit limits within the permissible limit of the eligible loan limit, up to 30%.

Example

Let us look at some credit rating examples to understand the concept. Suppose Alex wants to avail of a personal loan to get his medical bills repaid. Alex goes to the bank in the neighborhood for the applying loan. The bank asks for various documents and details regarding any previous loans. Alex provides all the documents and gives his consent to get the credit rating done by the lender to know the creditworthiness.

After the wealth rating information gets fed into the credit rating agency’s scoring model, a scorecard of credit level gets generated. For example, Alex’s credit score is 670, which is quite good for housing loans but not enough for a personal loan. As a result, Alex is turned down by the lender as they fail to meet the loan requirements.

Credit Score vs Credit Rating

| Credit Score | Credit Rating |

|---|---|

| This score refers to a numerical scorecard derived from statistical models to assist in knowing the real creditworthiness of an applicant. | This rating refers to an option concerning the creditworthiness of an applicant. |

| It allows creditworthiness to be expressed mathematically in numbers. | It measures the creditworthiness of loan applicants’ alphabetical grades. |

| This score had to get converted to an appropriate rating before using them to know the capital requirements of a business. | This rating gets used directly for ascertaining the credit requirements for a business. |

| It uses a statistical base to produce a constant risk indicator of a borrower. | It comprises multiple credit portfolios and ways to assess potential credit risk. |

| Analysts involved in credit risks get quantified by an appropriate scorecard. | Similarly, credit rating becomes the ultimate risk management metric for analysts involved in credit risks, using Credit-Score as input and other information on creditworthiness. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

How does credit score increase?

A history of on-time payments, low credit card balances, a variety of credit card and loan accounts, older credit accounts, less frequent loan applications, and few credit inquiries are all factors that raise your credit score.

What is considered a good credit score?

Even though ranges differ based on the credit scoring model, credit scores between 580 and 669 are regarded as fair, 670 to 739 as good, 740 to 799 as very good, and 800 and up as exceptional in all the major credit rating agencies like FICO and Vantage.

What credit score is needed to buy a house?

When one applies for a traditional loan, it is advised that their credit score be 620 or above. It is because lenders may not be able to approve their loans or may be forced to offer them a higher interest rate, which could mean higher monthly payments if their credit score is below 620.

How credit score is calculated?

The credit bureau typically determines your credit score by compiling information from prior years regarding your payment history. Then, it gets calculated using mathematical models based on the complete credit report of the loan applicant by the CRAs.

Recommended Articles

This article has been a guide to what is Credit Score. Here, we explain how to check it, its example, steps to improve, and comparison with credit rating. You may also find some useful articles here –

Recommended Articles

Continue with these closely related articles from the same guide.