Table Of Contents

What Is Construction Work in Progress?

Construction work in progress refers to the cost related to the work in progress of each incomplete work related to the construction of long-term assets and fixed assets. It is a debit balance and is treated as an asset in the future and thereby will be recorded on the assets side of the balance sheet under the head of non-current (long term) assets till the construction is not completed. These costs are not depreciated in the books of accounts until the asset is fully ready to use and it's been put into the service of the business.

Table of contents

How To Calculate?

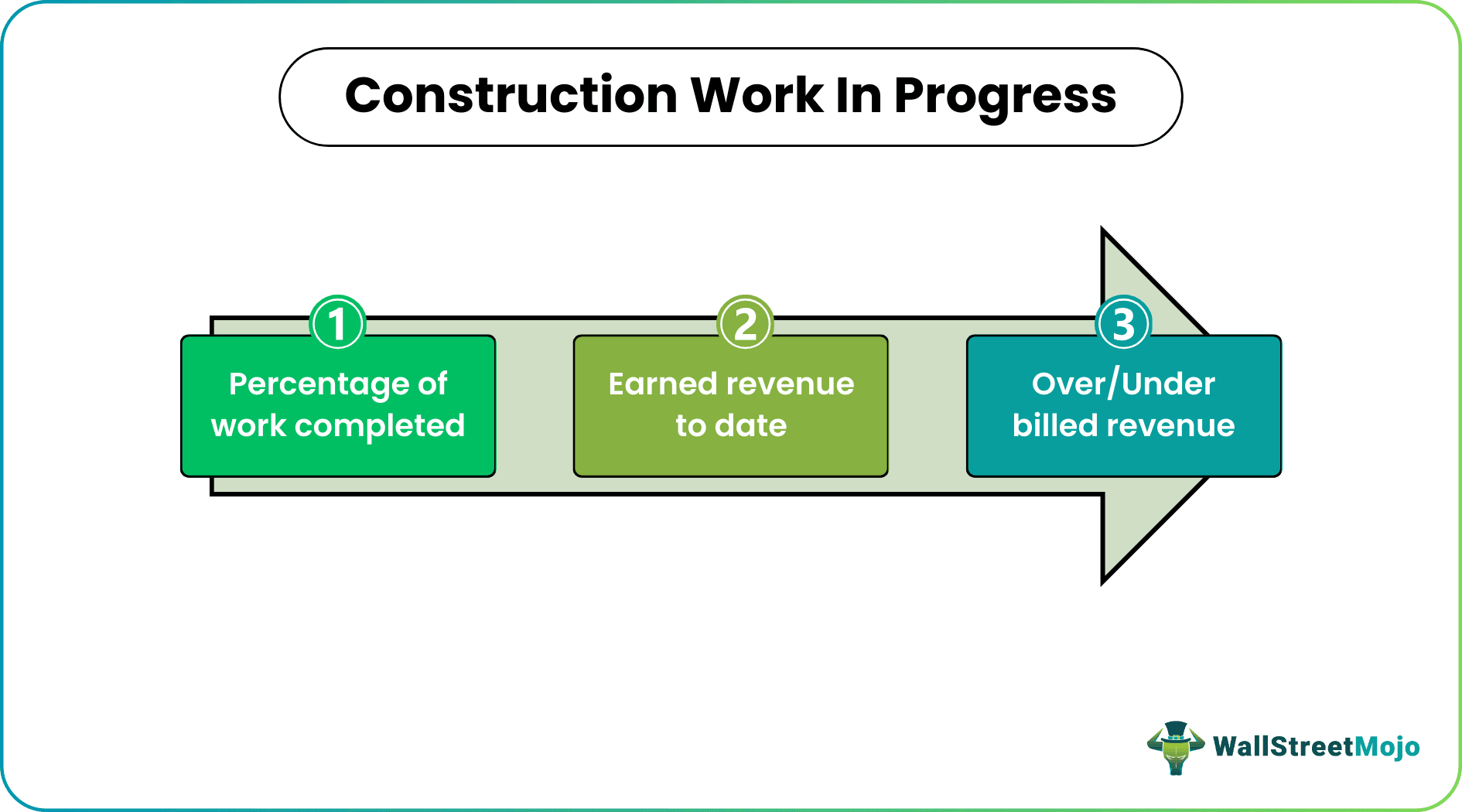

The steps that are required to be followed while calculating construction work in progress are as follows:

#1 - Percentage of Work Completed

It refers to the calculation of the percentage of work completed to date. The formula for the same is:

Percentage of Work Completed = Actual Costs till Date / Total Estimated Costs

#2 - Earned Revenue to Date

After calculating the percentage of work completed, the percentage is applied to determine the Total estimated Revenue to calculate the Earned revenue to date finally. The formula used is :

Earned Revenue till Date = Percentage of Work Completed * Total Estimated Revenue

#3 - Over/Under Billed Revenue

Now the third step is to calculate the over/under billed revenue where the same is calculated using the below-mentioned formula:

Over/Under Billed Revenue = Total Billings on Contract - Earned Revenue till Date

Example

Suppose we take an example of XYZ Ltd., to whom the seller P Ltd delivered the materials on 1st April 2020 to the job site and charged an amount of $400,000. So the journal entry would be:

Next, on 5th April 2020, XYZ Ltd received an invoice from the transportation company for delivering materials at $5,000. So the journal entry would be:

On 14 April 2020, XYZ Ltd. used some of its inventory in constructing the work of a building, and the inventory was priced at $10,000. So the journal entry would be:

On 30th April 2020, seller D Ltd. supplied materials to the job site and charged and invoiced for $80,000. So the journal entry would be:

On 9th May, 2020, XYZ Ltd completed the building's construction and put it into service. The finance department summed the costs, and the total costs would be:

- Seller P Ltd Invoice: $400,000

- Seller D Ltd Invoice: $80,000

- Inventory: $10,000

- Transportation Bill: $5,000

- Total: $495,000

So the journal entry would be:

Construction Work in Progress Double-Entry

When the costs are added to the construction in progress, the construction in progress account is debited with corresponding credits to accounts payable, inventory, cash, or bank. When the construction in progress is completed, the corresponding long-term asset account gets debited, and Construction in progress account is credited. Hence, the double-entry system is given both sides.

Entry to record the purchase of material:

Entry to record the completion of work:

Advantages

- It gives a clear vision to the company for its future costs.

- The construction work in progress helps to control unwanted costs.

- The construction work in progress account measures all the expenses and allows its users to prevent wastage of money in various areas.

- They help the management to control its risk factors for future events.

Disadvantages

- There can be some forecasting mistakes that management can make for which there can be mixed planning for future events.

- Sometimes, there can be huge costs involved in this, which can be a costly arena for the company's management.

- The design costs also play a major role, which can affect the company's financial health.

Conclusion

Construction work in progress is an account that measures everything about the costs, expenses, etc., when the construction is still on, i.e., the construction is still not completed, and the service is not put to use. This account helps the management to predetermine many costs and future billings to plan all its expenses.

Recommended Articles

This has been a guide to what is Construction Work in Progress. Here we discuss how to calculate construction work in progress and an example, advantages and disadvantages. You may learn more about financing from the following articles –