Table Of Contents

What is the Cost of Goods Available for Sale?

The cost of goods available for sale refers to the cost of total goods produced during the year after accounting for the cost of finished goods inventory at the beginning of the year and is available for sale to the end-users.

Table of contents

Calculation of Cost of Goods Available for Sale

It includes all the manufacturing costs related to the production of the final inventory, including the material, labor, and overhead expenses, as well as the cost of finished inventory in hand at the beginning of the period. However, this does not include the cost related to the selling and distribution of the goods for the reason it is the cost of the total inventory available for sale and not the total cost of sale of the product.

Thus, the calculation can be arrived by preparing a cost sheet, as shown below:

Cost Sheet

For the Period Ending…

| Particulars | US $ | |

|---|---|---|

| Particulars | US $ | |

| Direct Material Consumed | a | xx |

| Direct Labor Cost | b | xx |

| Direct Overhead Expenses | c | xx |

| Prime Cost | d= | xx |

| Factory Overhead | e | xx |

| Gross Factory Cost | f=d+e | xx |

| Stock in Process at the Beginning | g | xx |

| Stock in Process at the End | h | xx |

| Net Factory Cost | i=f+g-h | xx |

| Office and Administration Overhead | j | xx |

| Cost of Production | k=i+j | xx |

| Finished good inventory at the Beginning | l | xx |

| Cost of Goods Available for Sale | m=k+l | xx |

| Finished good inventory at the End | n | xx |

| Cost of Goods Sold | o=m+n | xx |

| Selling and Distribution Expenses | p | xx |

| Cost of Sales | q=o+p | xx |

| Profit Margin | r | xx |

| Sales | S | xx |

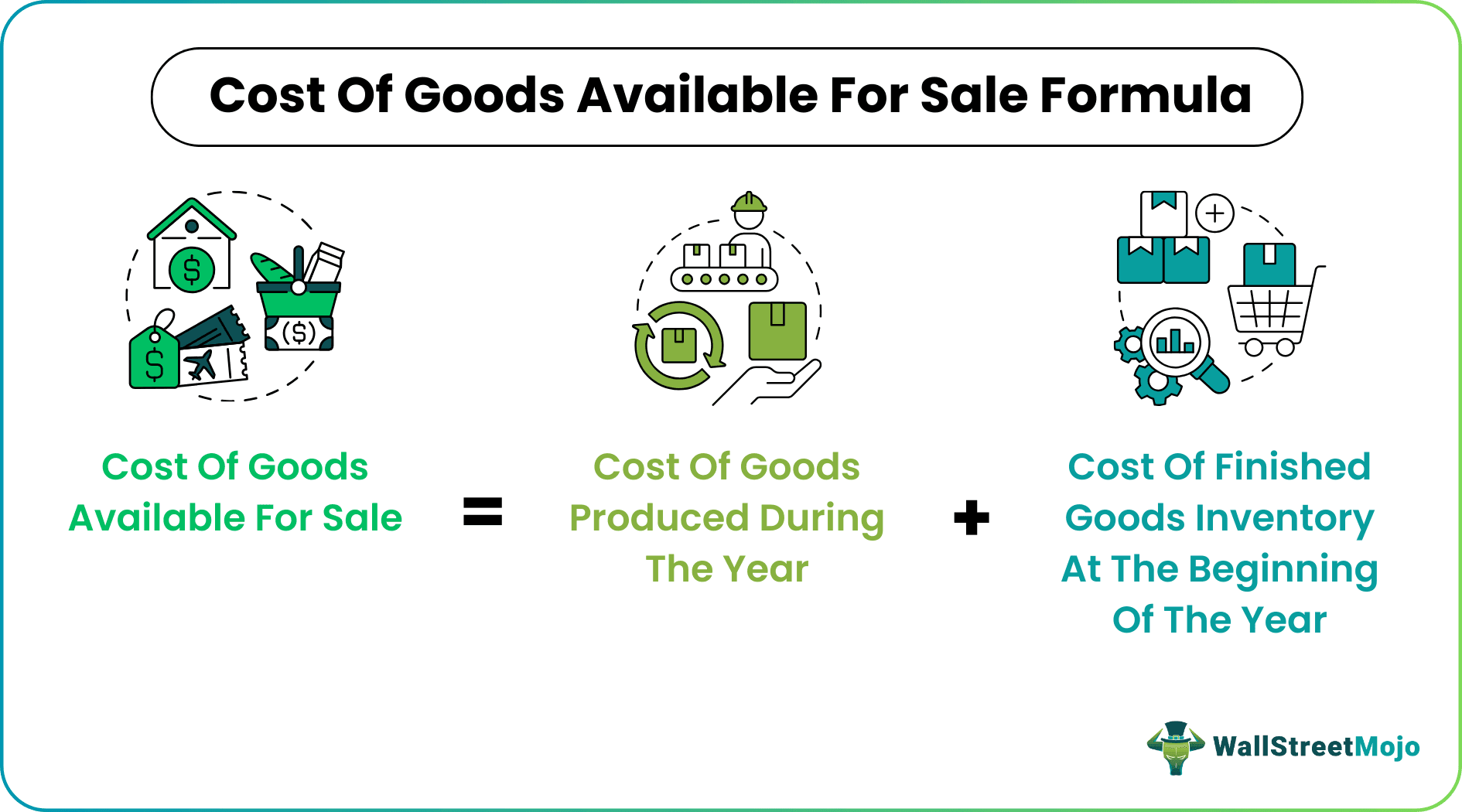

Cost of Goods Available for Sale Formula

Cost of Goods Available for Sale Formula = Cost of Goods Produced During the Year + Cost of Finished Goods Inventory at the beginning of the Year

Example

XYZ Inc. manufactured 2000 units of its product during the year. The total production cost of producing the 2000 units of output was US $ 10,000. The Company also had 100 units of inventory at the beginning of the year worth US $ 800. It paid US $ 250 towards the distribution of its product and left with an ending inventory of US $ 600 at the end of the year. What will be the cost of goods available for sale?

In this case, there will be

Remember, we will not account for the cost of selling the goods and the cost of inventory at the end as we are computing the total cost attributable to the salable product in hand, not the cost of the product sold.

Let’s take another example.

Suppose XYZ Inc. produced 1000 chocolate boxes for a total production cost of US $ 4000. The Company had 75 boxes with it as inventory worth US $ 360 at the beginning of the year.

In this case, there will be

Again, we will not account for the cost of promotion and inventory at the end as we are calculating the total cost attributable to the salable product in hand, not the cost of the product sold. Also, the cost of freight inward is a part of production cost as it is the transportation cost of bringing the material to the factory place; hence it is a part of overhead expenses.

Conclusion

Cost of Goods Available for Sale is the total production expense of the final output available for sale. It accounts for the cost of inventory in hand at the beginning of the period and excludes the cost of selling and distribution and the cost of inventory left at the end of the period.

Recommended Articles

This has been a guide to What is the Cost of Goods Available for Sale & its Definition. Here we discuss its formula along with step-by-step calculations and examples. You can learn more about it from the following accounting articles –