Part of our Journal Entries guide

What Is Cost Of Goods Sold Journal Entry (COGS)?

Recording journal entries for the cost of goods sold is an important step in the preparation of financial statements. The various steps of recording the same helps in identifying all the direct cost that are associated with the manufacturing process of goods and services.

It includes items like expenses for raw materials, direct labor, manufacturing overhead like rent, electricity bill, cost of distribution or transportation of goods and services to the customers and any other associated costs. It is essential to arrive at the actual figure of gross profit and later on use it to prepare the financial statement.

Cost of Goods Sold Journal Entry Explained

The journal entries for cost of goods sold refers to the accounting entries that are done in the books of accounts in order to clearly maintain records of various transactions related to the same. This is very useful for the purpose of maintaining transparency, accountability and is used in preparation of financial statements and reports.

Another purpose of studying the correct way to enter the cost of goods sold related transactions in the books is that they provide support during audit procedures. These transactions related to cost of goods sold general journal entry, give a clear picture of the initial steps of production which is used to ultimately arrive at the profitability figure.

The following Cost of Goods Sold journal entries outline the most common COGS. Inventory is the cost of goods we have purchased for resale; once this inventory is sold, it becomes the cost of goods sold, and the Cost of goods sold is an Expense. Inventory is goods ready for sale and shown as Assets on the Balance Sheet. When that inventory is sold, it becomes an Expense, and we call that expense the Cost of goods sold.

Sales Revenue – Cost of goods sold = Gross Profit.

Gross profit can also be called Gross Margin.

- Sales revenue is based on the Sales Price of Inventory sold.

- Cost of goods sold is based on the Cost of inventory sold.

- Inventory is based on the Cost of inventory in hand.

It is crucial for the company to control and manage the cost of goods sold so that the profit levels are maintained and inspite of growing competition in the market te company is able to sustain its operations successfully along with increase in customer base.

Cost Of Goods Sold Explained In Video

Examples

Let us understand the process of recording journal entries of cost of goods sold with the help of a suitable example.

Example #1

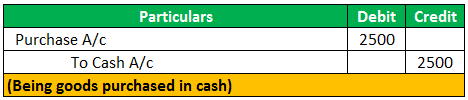

Suppose we have purchased 100 pens for $25/- each, So the Journal entry for the above transaction will be:

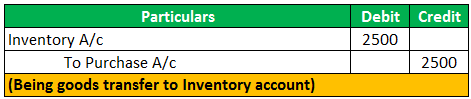

These pens are now known as inventory because they are purchased with the intention of resale.

Thus it means, it is Inventory.

Now suppose we have sold this inventory

Then two transactions take place

- First Sale of goods (pens);

- Second, losing inventory (pens).

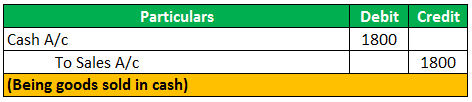

Suppose we sold 60 pens at $30/- each.

Now we don’t have 60 pens in our inventory anymore.

60 pens at cost= 60*25 that is $1500.

It is the Cost of goods sold.

We need to adjust the inventory by the cost of goods sold.

The sales revenue and cost of goods sold.

Gross Profit = Sales revenue – Cost of goods sold 300 =1800-1500

Or

Sales – Gross profit = Cost of goods sold 1800-300 = 1500.

So the cost of goods sold is an expense charged against Sales to work out Gross profit.

- Cost of goods sold formula does not include general expenses such as salary, Wages, advertising, etc. since it is a direct cost of the inventory that we have sold during the year;

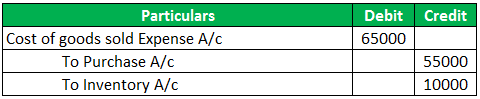

Example #2

XYZ Limited has an opening inventory of $25000/-.The company has purchased goods of $55000/- from the supplier during the month, and at the end of the month, the ending inventory of $15000/-.

The cost of goods sold journal entry will be:

The formula for Cost of Goods Sold (COGS):

Cost of Goods Sold (COGS) = Opening Inventory + Purchases – Closing Inventory

Or

Cost of Goods Sold (COGS) = Opening Inventory + Purchase – Purchase return -Trade discount + Freight inwards – Closing Inventory.

From the above examples of cost of goods sold general journal entry we can clearly understand the method followed to record entries in the books related to COGS. It shows how we can identify the required items from financial statement and use them to record for the COGS so that it becomes easy to use it for analysis and evaluation later on.

Points To Remember

So, here are some points to be kept in mind regarding accounting cost of goods sold journal entry, which is beneficial for accountants and individuals who want to understand the concept better.

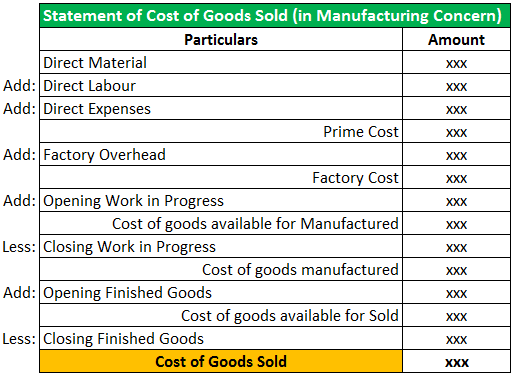

- The cost of goods sold in a manufacturing business includes direct material, labor cost, product cost, allowances, freight inwards, and factory production overhead.

- In Trial Balance, only a purchase account is shown with years of the total purchase value, not the cost of goods sold.

- The Cost of Goods Sold Journal Entry is made to reflect closing stock. That is an increase or decrease in stock value while accounting cost of goods sold journal entry.

- The Cost of Goods Sold is deducted from revenues to calculate Gross Profit and Gross Margin.

Recommended Articles

This article has been a guide to what is Cost Of Goods Sold Journal Entry. We explain the entries with some examples and mention some important points to remember. Here are the other articles in accounting that you may like –