Part of our Accounting Concepts guide

Deferred Compensation Meaning

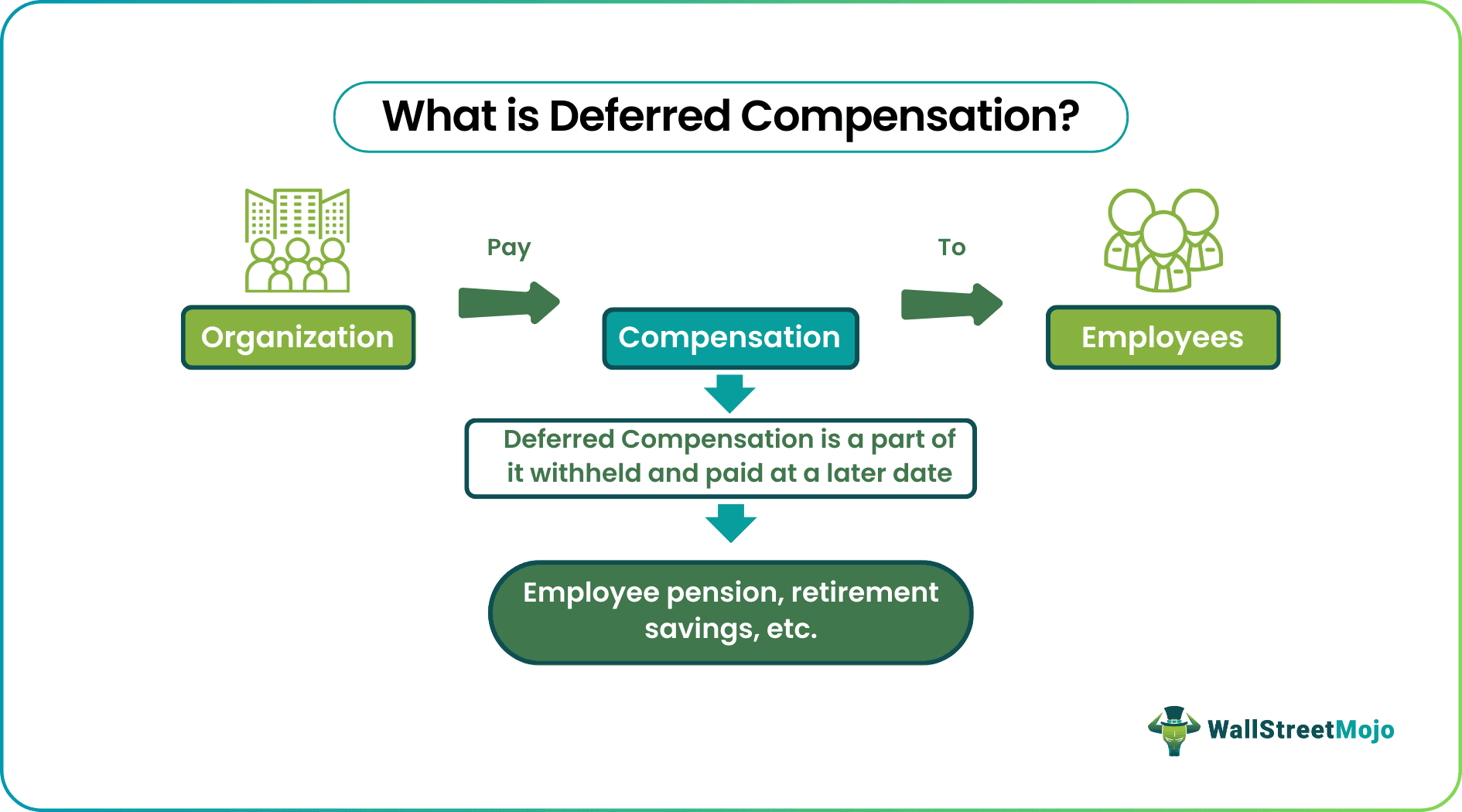

Deferred compensation refers to that part of one’s income that is subject to payment at a future date. The employers withhold a portion of an employee’s salary for a longer period, and defer the disbursement. Such compensations help employees save a percentage of their earnings to ensure financial stability and security throughout their life.

Deferred compensation introduces multiple tax benefits to employees as their taxable income decreases. In addition, the taxes do not apply until the employers pay out the employees or the recipient’s withdraw the amount. Some examples of such compensations include retirement schemes, pension plans, insurance schemes, other contingency plans, stock option schemes, etc.

- Deferred compensation is an arrangement whereby a portion of an individual’s income is set aside and paid at a later date.

- There are two types of such compensations – Qualified and Non-Qualified.

- The choice of the compensation individuals makes on their tax situations.

- Nowadays, it is an essential tool in tax planning, permutations, and combinations to ensure maximum benefits for individuals and companies.

How Deferred Compensation Works?

A deferred compensation plan allows individuals to keep aside a fraction of their income untaxed until withdrawn. In addition, the taxable amount also decreases for the current year, thereby providing significant tax benefits to employees for the term.

Companies withhold a portion of the monthly compensation of employees and store it over time until the predetermined date arrives. On the date as per the employment contract, the employers pay a lump sum to their employees.

Employees can opt for a plan based on their tax situation. For example, if they expect the future income tax rate to be lower than the current rate, they can opt for the programs offering potential tax benefits. As a result, their deferred tax payment shifts to a later date, i.e., at the time of paying out or withdrawing the amount.

On the contrary, if employees expect that the future tax rate will be higher, they can opt for plans offering tax deduction options at the time of investment and not at distribution.

Moreover, other factors that might affect employees’ decisions include the country’s economic situation, government-extended benefits, prospective tax laws, etc.

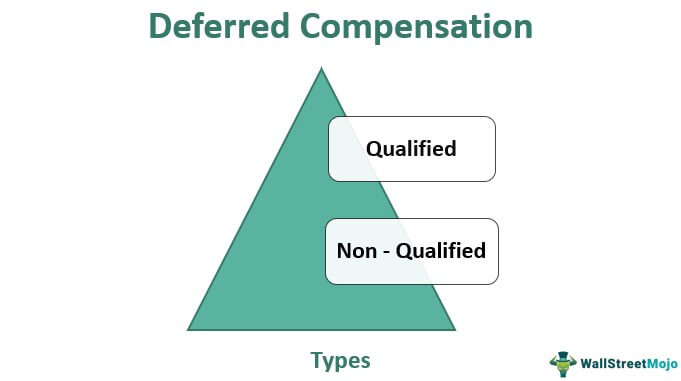

Types of Deferred Compensation

Deferred compensation nationwide is broadly classified as Qualified and Non – Qualified.

#1 – Qualified Deferred Compensation

These are the strictly governed plans monitored and administered under standard rules and regulations. The Employee Retirement Income Security Act (ERISA) sets the laws that govern this compensation option. Also, it restricts depositing amounts beyond a certain limit.

The qualified option keeps the saved amount of employees secure. This is because ERISA does not allow employers to touch that portion of the company’s fund at any cost, no matter how worst the financial situation becomes for a business.

The qualified compensation is for the benefit of the recipient only. The law does not allow companies to use it to pay off creditors and take businesses out of financial crises, even if they are on the verge of bankruptcy. Some examples are 401(k), 403(b), 457 deferred compensation plan, etc.

#2 – Non-Qualified Deferred Compensation (NQDC)

As ERISA imposes restrictions on qualified options, a non-qualified compensation alternative came into existence. This alternative had no legal monitoring and control bindings. However, the most significant difference is that these options did not limit the amount to withhold for payment at a later stage.

NQDCs are for those who earn high and desire to save more without any restriction. As a result, such employees get an opportunity to have even lower taxable income and enjoy better returns on tax-deferred investments.

Though the returns expected are higher, these are not safe options. Unlike qualified alternatives, companies can use these portions of employees’ income to pay off their debts. In addition, as there is no law to govern this compensation type, the employees cannot expect authorities to take any actions upon reporting the incident.

Examples

Moving further, let us consider the following examples to understand the concept well:

Example #1

Scarlet has an income of $250,000 per annum, and she opts to defer her compensation using non-qualified deferred compensation. Thus, she agrees to save $50,000 every month to her NQDC account for 15 years. At the time of withdrawal, however, she knew she would receive $9 million as a lump sum for a further tax deduction.

She was happy to see the huge tax benefit she was enjoying. However, during the 10th year, her company filed for bankruptcy, and it used her ten years of savings to pay off its debt. Scarlet contacted the management, but they did not entertain her. As the plan was under no legal regulation, the authorities did not address her complaints, and she lost all her money.

Example #2

After its merger with Bank of America, Merrill refused to settle the deferred compensation for brokers. It stated that the company does not allow broker compensation if they do not remain in the firm for a specific tenure. The brokers proved that the company’s contract allows employees to leave for “good reason.” After a long legal battle, the brand agreed to pay $40 million for a class action settlement with 1,400 brokers in 2012.

Thus, it shows how legal or qualified deferred income keeps employees’ income safe even if they quit.

Advantages & Disadvantages

This type of compensation comes with its own set of pros and cons. Let us have a look at the same below:

| Advantages | Disadvantages |

|---|---|

| Secures post-retirement life | Tax situation matters |

| Allows enjoying huge tax benefits | Completion of predetermined tenure is important |

| Helps build resources | |

| Makes future planning easier |

Frequently Asked Questions (FAQs)

What is deferred compensation?

It is the fraction of an employee’s compensation that employers withhold to be paid later. It is available in two forms – qualified and non-qualified compensation. While the law regulates the former, the latter remains devoid of it, and hence, it is not as safe as the qualified one.

Is deferred compensation a good idea?

Yes, it is a good idea as it secures an individual’s future in financial terms. They can save well for their retirement while enjoying significant tax benefits as the amount saved remains untaxable until it is withdrawn. However, if one is choosing a non-qualified compensation option, it might not be secure enough. Thus, the choice should be made carefully.

Is deferred compensation taxable?

It remains tax-deferred until it is withdrawn. As soon as employees withdraw the savings, tax is imposed on the lump sum.

Recommended Articles

This is a guide to Deferred Compensation and its meaning. Here we explain how does it work, what are its types, and examples. You can learn more about financing from the following articles –