Table of Contents

What Are Digital Payment Methods?

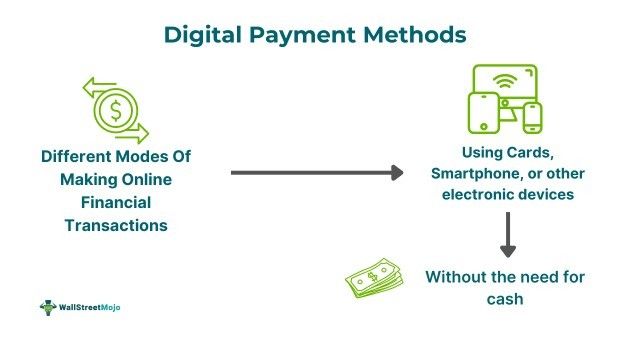

Digital payment methods are the various electronic modes used for executing financial transactions like paying bills, making purchases, transferring money, etc., rather than using cash. These mediums include mobile wallets, card payments, pay links, P2P digital payments, and crypto payments.

These online payment modes have made people independent, carrying sufficient cash. Moreover, users can make instantaneous payments from any corner of the world with just a few clicks. Indeed, these methods ensure immediate transfer of funds through a secured payment gateway, thus reducing the possibility of delay or fraud.

Key Takeaways

- Digital payment methods are the online transaction modes available to users for transferring funds, paying bills,

- and making purchases using their smartphones or other devices without any physical cash.

- Some popular online payment methods are debit/credit cards, digital wallets, pay links, P2P digital payments, and Unified Payments Interface (UPI).

- These modes of payment are comparatively more convenient than the traditional payment system since users can send or receive money from anywhere at any time.

- They facilitate quick money transfers through an encryption-protected gateway. However, technical downtime, payment failures, and cyber fraud are some concerns.

Digital Payment Methods Explained

Digital payment methods refer to different options for a user to make an online financial transaction without relying upon physical cash. It helps people go cashless while shopping, offline or online, paying bills, traveling, or going on a vacation. Moreover, banks have evolved from traditional banking facilities to offer their customers a broad range of online payment options in a competitive business scenario, driving demand for a Business Payment app that supports fast, secure, and scalable transactions.

Further, the use of Encryption, biometrics, and fraud detection systems has even made online payments more reliable than ever before. Also, the cyber cells, government, and regulatory bodies have set strict rules and regulations for safeguarding consumers against online payment fraud and cyber attacks. Such measures include data privacy, consumer rights, anti-money laundering, licensing, cybersecurity, consumer protection, and interchange fees. In fact, with the growing demand for mobile payment app development, companies are focusing on building highly secure platforms that comply with these regulations. Financial institutions and other service providers need to follow these regulations to strengthen the digital payment system and ensure excellent safety and credibility in online transactions.

New arrivals and students often explore options like the Suits Me for accessible banking services tailored to their needs.

Types

Online payment modes are the present and future of the world. Let us explore the different digital payment methods available to the users for making online financial transactions:

- Card Payments: Customers can obtain a debit, credit, or prepaid card from their respective financial institutions. The card is directly linked to their bank accounts and can be swiped anywhere to make payments.

- Digital Wallet Payments: These apps store the user's card or other payment details and can be used on any device to facilitate online transactions. One such example is a mobile wallet that enables users to make payments through mobile apps like Google Pay, PayPal, and Venmo. The growing demand for such applications has created opportunities in mobile payment app development for companies looking to create secure, user-friendly financial transaction platforms and efficient payment systems for digital goods.

- Electronic Bank Transfer: Users, whether individuals or companies, can directly transfer any amount from their bank account to a single or multiple bank account in a fraction of a second using this medium.

- Peer-to-Peer Digital Payments: P2P payment is a way to make a one-on-one financial transaction. It enables a person to transfer funds to another individual's bank account.

- Contactless Payments: Contactless payments are an advanced digital payment mode that allows users to disburse payments by waving or tapping their contactless card above a card reader. The amount is transferred through a secured terminal.

- Mobile Point of Sale (MPOS) Systems: An MPOS is a portable device, tablet, or smartphone that facilitates payments and receipt printing while moving around from one location to another, such as at petrol pumps.

- Social Media Payments: Users can pay money to each other in a secure environment using social payment apps with a strict encryption protocol over social media platforms.

- Crypto Payments: Some apps and businesses accept payments through cryptocurrencies or other similar digital assets through blockchain technology.

- Paylinks: These are the payment links received by the payers through emails, messages, or notifications where they can click on the mentioned link to disburse the stated amount.

For efficient cross-border payments, many individuals and businesses use the Wise Money Transfer UK or Wise Money Transfer US services for transparent and low-cost transfers.

Examples

Understanding the need for the digitalization of financial transactions is incomplete without the following real-world examples:

Example #1

Suppose ABC Ltd. is a software company with an annual turnover of USD 2.5 million. It is a small business entity with 28 employees. The company sells its services across the US through its website and accepts payments online through various digital payment methods, such as digital wallets, P2P digital payments, and card payments. Moreover, the company disburses the monthly compensation to its employees through an electronic bank transfer, which allows the accounts manager to conveniently credit the salaries without visiting the bank.

Example #2

Brazil's economy was anticipated to reach a GDP of USD 2.13 trillion in 2023 due to the nation's rapidly growing economic diversification and digitalization. The country is witnessing a financial transaction evolution with a rapid increase in digital payments, especially Pix, which handles more than 3 billion monthly transactions. Brazil's e-commerce sector captures one-third of the overall Latin America market and is expected to surge further to USD 125.68 billion by 2029. Moreover, in Brazil's B2B sector, 68% of business entities engage in digital interactions, while digital wallets have become a daily affair for one-third of Brazilians.

Notably, there are around 22 digital banks in Brazil, including Nubank, C6 Bank, PicPay, Mercado Pago, and Banco Inter. Moreover, the country has seen a 26% decline in cash transactions since 2018, although some payments are only made in cash. Further, Brazil's inbound remittances have risen to USD 5 billion in 2023, while digital remittances are anticipated to reach USD 870 million in 2024. The nation's e-commerce transactions, especially with China, account for 4% of the overall transactions. With the growth of the country's content creator market, which ensures online disbursements to more than 12 million people, digital payment methods will become more popular. However, amid significant challenges in Brazil's cross-border B2B payments, I.e., high fees and strict regulations, 38% of the businesses have switched to digital payment systems for more efficiency.

Source - https://www.thunes.com/news/how-digital-payments-drive-brazils-economic-transformation/

Advantages and Disadvantages

Millennials and Gen-Zs have said goodbye to the habit of carrying cash all the time, and an increasing number of Gen-X are now adopting digital payment methods. For more on how cash usage is evolving across generations, see this study by Empower | The Currency. However, along with many pros, these modes of transaction also have some flaws, as discussed below:

| Advantages | Disadvantages |

|---|---|

| Digital payment methods have reduced the need and risk of carrying cash or checkbooks every time, making people's lives easier. | The biggest drawback of these methods is the technical glitch that results in downtime or payment failure. |

| The availability of different digital payment methods ensures that users can choose the method they find most convenient. | Cyber fraud, such as phishing attacks, ID theft, etc., in online payments, is another critical issue that users may face, and the cost of it is as high as sweeping out the whole bank account. |

| People no longer need to visit the bank or ATMs frequently for cash withdrawals since these online payment modes are linked to their bank accounts. | Hackers can steal bank details and other personal information provided by users while making online transactions to commence cyber theft. However, digital transactions generally require a One-Time Password (OTP) nowadays. |

| Also, it has helped businesses expand globally while accepting payments from anywhere in the world. | There is a minimum transaction limit, which restricts users from paying a higher amount through digital modes. |

| Unlike checks, digital payments have no waiting period, and funds are transferred from one bank account to another in just a few seconds. | Also, every online transaction has a time limit for entering the OTP, beyond which it times out, and the payment can't be processed. |

| These online payments are made through highly secured Gateways empowered by fraud detection systems and Encryption. | If a user loses their smartphone with their digital payment details or their cards, then these can be used illegally to steal money from their bank accounts. |

| Further, these payment options are available to customers in remote areas who can access traditional banking facilities conveniently. | While cash transactions don't have any fees or charges, users have to incur various online payment fees for using such facilities. |

| Also, the digital payment system keeps a complete record of all transactions, whether successful, processing or failed, to help users track their payment status and review their spending. | Many people are unable to make online payments due to their technical illiteracy, and many don't have smartphones or even bank accounts. |

| The payment fees charged by the facilitators are often low, making these methods cost-efficient. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.