Table of Contents

Economic Productivity Definition

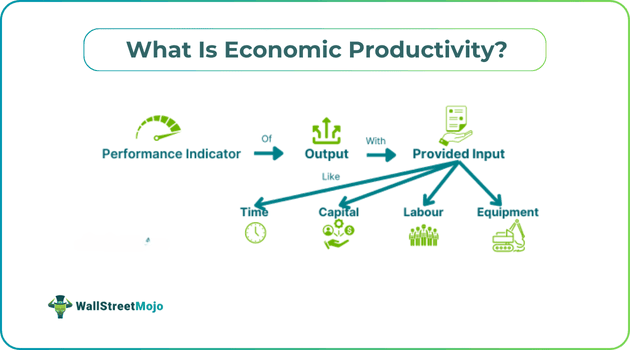

Economic productivity refers to the output received in exchange for the input provided. It serves as a performance indicator that collates the output with the input, which could be anything from time, capital, equipment, or labor. It is the ratio between the gross domestic product and the number of hours worked.

In the US and UK, government authorities focus more on labor productivity. However, there are different types of productivity. In business, productivity simply indicates a company's performance in terms of its production value. It is an important metric for shareholders and investors, including market experts and economists, to understand corporate profits and the economy.

Key Takeaways

- Economic productivity is the measure of output achieved compared to input offered. The input can be anything from labor, time, money, or equipment.

- There are two measures of this productivity: labor productivity and multifactor productivity, also known as total factor productivity.

- Both reports are released by the Bureau of Labor Statistics (BLS).

- Currently, Ireland, Luxembourg, and Denmark top the list of countries with the highest economic productivity, and the US is in eighth place.

- It serves as an essential performance indicator for global economies and sectors, underlining their productivity relative to their social growth and standard of living.

Economic Productivity Explained

Economic productivity defines the output achieved in turn of the input provided. The output is majorly expressed in monetary terms, but the input can be time, effort, labor, capital, or equipment. It is an important performance metric based on which countries gauge their economic contribution to the world economy. Organizations and governments tend to work with the objective of increasing economic productivity, which is a scenario in which more output is produced using the same amount of input, or the output remains the same, but input levels are reduced.

The economic productivity by country is based on gross domestic product (GDP) per hour worked and is expressed in American dollars. Currently, Ireland, Luxembourg, and Denmark are among the top three nations on the list. The United States stands in the eighth position. Productivity and wages are interlinked, and higher productivity is directly proportional to higher wages. Workers with higher productivity produce more output in the same amount of time or resources, leading to higher profits, and are entitled to receive higher wages from companies.

There are two main measures of economic productivity. The first is labor productivity, which is the output per hour, and the other is multifactor productivity, which also denotes total factor productivity. Both of these metrics are produced by the Bureau of Labor Statistics (BLS). Labor productivity is the ratio of inflation-adjusted output per hour. Its estimation across sectors and industries is published quarterly by the BLS, and its growth depends on the actual output and hours worked. On the contrary, multifactor productivity is an alternative measure comparing real business sector output to the combined input of labor and capital; its report is released annually.

How To Calculate?

The economic productivity formula is as follows:

Economic productivity = Units of output/Units of input

Here, the input can be labor, time, equipment, or capital, whereas the output is the number of goods and services produced or targets achieved.

A key note to remember is that the unit defines the productivity context.

How To Increase?

Ways to increase or improve this productivity are:

- Generation of employment and workforce development, with workers handling jobs accurately and efficiently. They are to be skilled and trained well.

- Using the right resources when it comes to technology, machinery, and equipment. It evidently becomes a crucial part of the production process and reduces the required time.

- Proper utilization of human and natural resources at the optimum level of production with the application of both economic forces and different forms of energy.

- In a manufacturing or production process, multiple factors, elements, and frameworks are involved. All of them have to be appropriately aligned and managed correctly.

Examples

Here are two examples of the concept; the first one is a formula-based calculative example, but the second example comes from a global news article:

Example #1

For a calculation-based example, suppose Marcus is employed for 45 hours a week at a battery company. In a given week, Marcus manufactures 180 batteries. The productivity of Marcus in this week will be

Productivity = Output/Labor input

Therefore, 180/45 = 4 batteries in one hour.

Now, if the factory in any given week adds the gross value of the batteries to be 4.5 million dollars with a total of 135000 hours of labor

Productivity = Output in terms of cash/Input hours

Hence, 4,500,000/135,000 = $33.333 per hour

Based on the hourly dollar productivity, the economic productivity of the battery company and monthly, quarterly, or annual economic output can be calculated.

Example #2

According to an article published in Financial Mirror, GenAI will raise economic productivity along with social risk. GenAI, coupled with other AI models, will transform the way organizations work. These models will spread across the public sector and most industries. The concern would be that AI, with its creative possibilities, increases the potential for job losses across many advanced and emerging economies.

Thus, productivity will rise, but GenAI applications will displace jobs, including those requiring moderate skills. Additionally, rapid adoption may result in political and social tensions. The rules for the use of AI will play a crucial role, including policy challenges and social risks. Governments with strong policy-making institutions are likely to develop frameworks for it. Moody's Investor Service first published this article.

Importance

The importance of this productivity is as follows:

- It uplifts and represents the stability and position of national economic growth.

- Productivity is directly related to higher profits; the better the productivity, the higher corporate profits, and returns can be generated.

- As this productivity increases, the prices of goods and services are lowered, and consumers can enjoy better-quality products at an affordable price.

- With optimum productivity, companies earn through economies of scale, and hence, the wages of workers are expected to rise, but it will get offset by the profits. So it is essential for workers as well.

- With increased productivity, the overall GDP, higher standard of living, corporate revenues, and social growth are interconnected.