Part of our Banking Services and Operations guide

What Is A Stop Payment?

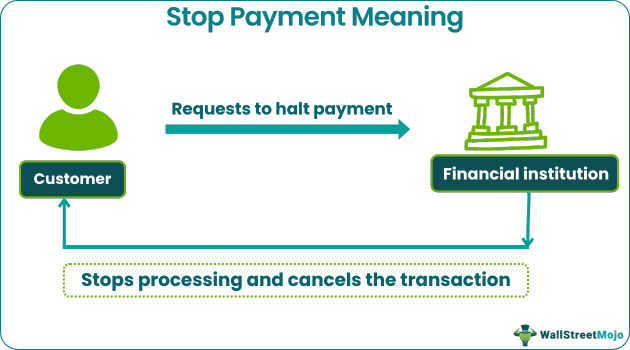

A stop payment refers to a request by a customer to stop the payment before being processed using a wire transfer, automated clearing house (ACH) or check payment. It aims to prevent fraud, disputes, and insufficient funds.

It is effective only when done on time. The discretion of implementing the stop payment lies with the bank. It is done via email, personal branch visits, or over the phone. Most of the banks charge a small fee for carrying out these instructions. The order expires after 6 to 12 months but is renewable.

- A stop payment is a customer’s request to halt a transaction, like wire transfers, ACH, or checks, before processing to prevent fraud, disputes, and insufficient funds.

- It gets triggered for various reasons, including incorrect information, wrong mailing addresses, theft, insufficient funds, disputes, and fraud.

- To cancel a wrong payment instruction, check the timeframe fees, contact the bank, verify the instruction canceller, provide the necessary information, and request a formal stop payment request.

- It is a preemptive measure against fraud, halting payment while a void check cancels a check before bank presentation and a cancel check voids after issuance but pre-presentation.

How Does Stop Payment Work?

Stop payment is defined as a banking service allowing its customers to appeal for cancellation of a check or payment transaction. It can only be done before the processing of the check or transaction. It mainly helps to prevent fraud and help customers correct any error in check issuance or loss stolen or loss of check.

Upon detection of any error, lost check, or dispute, a customer formally requests its bank to stop the payment. After the bank receives the request, it checks for the validity of the request and, if valid, tries to stop the transaction or check honoring. Consequently, the bank flags the transaction or check payment and cancels its processing. Such stop-payment instructions are kept on record for six to twelve months.

The stop payment order expires when the payment fails to get processed during the stipulated time. Businesses use it to ensure fraudulent activity. The financial world remains free of corruption and malpractices using it. Individuals can easily thwart wrongful payment or fraud from their accounts. Banking has become more trustworthy and safe.

It has brought stability and growth in the banking sector. Financial institutions like Wells Fargo offer services to facilitate stop payment requests under Wells Fargo stop payment, ensuring a reliable approach for managing such situations effectively. Moreover, concerns about the impact of a stop payment on credit card transactions arise. It may encourage scammers to withhold payments from the rightful owner of the issued checks.

Any unauthorized transaction or theft in check gets stopped by its virtue. Moreover, it has brought transparency and accuracy in financial transactions globally. People often wonder about the process and requirements when faced with a need to stop payment on a check. They can do this through a letter or telephonic instruction.

Crafting a letter to stop the check payment can be essential to communicate the intent to the bank. Therefore, stop payment enables consumers and organizations to stop pre-processing fraudulent or incorrect payments, assuring accuracy and financial security.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Reasons

Several reasons exist for evoking stop payment requests. The most common ones are as follows:

- Incorrect information: If a cheque is issued with the wrong payee name, incorrect amount, and date.

- Wrong mailing address: If the issuer writes the wrong address on the check or gets lost in the mail.

- Theft or loss of check: When a check becomes lost or stolen, it is done to prevent encashing the amount from the issuer’s account wrongfully.

- Insufficient funds: If an issuer realizes that their account does not have enough funds to pay the check holder. So, the issuer safeguards themselves from the legal issue of check bounce.

- Dispute: In any dispute with a seller, merchant, or party, one can issue stop payment instructions to prevent any withdrawals from the account.

- Fraud: If a person feels that he has become the victim of cyber fraud. It aids scamsters from any fraudulent withdrawals from bank account holders.

Examples

Let us use a few examples to understand the topic.

Example #1

Suppose Linda found herself short on funds after hastily writing a check to purchase her dream antique table. In a state of panic, she reached out to the bank, urgently requesting a stop payment. The bank assured her they wouldn’t honor the check. Days later, as she submitted the payment again with adequate funds, she felt relieved, knowing the check hadn’t gone through. This experience taught her about the responsible use of stop payments and the importance of financial planning.

Example #2

Sarah Graham from London attempted to cancel a £6,500 payment to scammers who claimed to be booking a Greek villa. She sought help from her bank but couldn’t stop the transaction. They informed her that they couldn’t intervene. Hence, the bank’s response left her disappointed and betrayed by both Vrbo and her bank. The incident mentioned here emphasizes the importance of exercising caution when making online reservations, as Sarah’s unfortunate experience serves as a poignant lesson to all.

How To Cancel?

One can execute stop payment instructions through the following steps:

- Check the timeframe of canceling the order of the payment stops.

- Check for the fees required to cancel the payment stop.

- Contact the bank immediately.

- Provide all the personal details asked by the verify that the instruction canceller is the real check or account holder.

- Provide all the necessary information to the bank, like account number, ACH transaction number, check number, payee name, payment amount, and payment date.

- Then, finally, make a formal request to the bank to cancel the cheque.

If the bank feels it can honor the cancellation instructions, it will cancel it.

Stop Payment vs Void Check vs Cancel Check

Let us use the table below to understand the differences between the three:

| Stop Payment | Void Check | Cancel Check |

|---|---|---|

| An instruction by the customer to stop the payment is a precautionary measure to stop fraud in the account. | It is the annulment of a check before it is presented to the bank for payment. | The process of canceling a cheque after its issuance but prior to presentation for payment. |

| It can be done after or before the check issue. | Always done before the issue of the check or just after its issue. | It can be done before the presentation for payment or after check issuance. |

| It can only be done only by check issuer. | Either the issuer or the recipient can do it. | The issuer amicably does it with the knowledge of the recipient. |

| It helps to correct wrong payments or fraudulent activity in the account. | The issuer does it to rectify the error, replacement, or non-occurrence of the transaction of the check. | One uses it in the instances of disputed payment or modification of mode of payment. |

| It requires a certain fee for implementation by the bank. | No charges are levied on the account of the holder. | The bank releases the amount to the account without levying any charge. |

| It immediately stops all transactions on the check. | The issued cheque gets invalidated immediately. | The canceled cheque gets invalidated immediately. |

| The check recipient is unable to encash the cheque. | The cheque recipient gets another cheque. | The recipient has no right to encash the cheque but gets other ways to get the payment. |

| Banks maintain a record of the stop payments and their request. | Accounting requires the record of such checks to be kept. | The issuer keeps a record stating the reason for the check cancellation. |

| It helps prevent loss of money from accounts due to loss, theft, or fraud. | Mistakes like the wrong payee name, amount, or date can be corrected. | It addresses any account change, payment change, or payment mode change. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1.How long does a stop payment last?

A stop payment on a check typically lasts approximately six months. However, if the issuer wishes to continue to prevent the cashing of the cheque beyond this period, they may need to resubmit the stop payment request.

2.Who can stop the payment of a cheque?

The account holder who wrote the check can initiate a stop payment request, preventing the bank from honoring the check if it hasn’t cashed it yet. However, this service usually incurs a cost.

3.Does stopping payment affect your credit?

Initiating a stop payment on a check doesn’t immediately impact your credit score. However, improper use of this action could strain your relationship with the bank, potentially leading to account limitations.

4.What does it cost to stop payment on a check?

Depending on the bank, the cost of placing a stop payment on a check varies, typically ranging from $20 to $35. Some account holders, particularly those with premium accounts, might qualify for this service to be provided free of charge by certain banks.

Recommended Articles

This has been a guide to what is Stop Payment. Here, we explain its reasons, comparison with void check and cancel check, examples, and how to cancel it. You can learn more about it from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.