Part of our Estate Planning guide

Subrogation Meaning

The subrogation concept pertains to a situation in which an insurance company steps in to recover losses caused by a third party to the insured. Its main purpose is to recover damages and minimize the losses incurred by the policyholder.

In the real case scenario, the insurance company pays the policyholder claims for the losses that occurred directly at the time of the incident, then seeks reimbursement from the third party’s insurance company. The insurance company then reimburses the amount of loss and other deductibles to be paid back to the insured.

- The subrogation principle in insurance refers to the legal right that an insurance company holds to protect the policyholder against the damages caused by the third party.

- It allows the insurer to recover costs, including deductibles, from the third party’s insurance company if the third party causes the damage.

- There are three kinds: equitable, contractual, and statutory.

- Waiver of subrogation gives the policyholder the right to waive off the reimbursement of the claim amount from the third party during damages.

Subrogation Explained

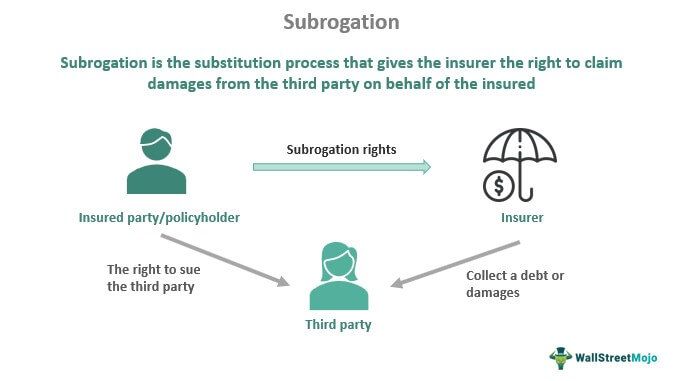

Subrogation, in simple terms, means delegating the responsibility or the right to claim to the hands of the insurer or the insurance company. It gives the insurer the legal right, on behalf of the policyholder, to claim money from a third party if they are found guilty at the time of the accident.

The concept comes under the indemnity clause, meaning a contract is signed between the insurer and policyholder that lays down the procedures and rules to be followed when claiming the amount against the losses and damages caused at the time of mishap by the other party.

It consists of an arrangement between the three stakeholders. One is the insurance company; the other is the policyholder, followed by a third party responsible for the damages. After a loss, the insured claims an amount against the loss caused by the third party from the insurance company.

After settling the claims with the insured, the insurer asks the policyholder for the legal rights to sue the third party. After that, insurance companies initiate the reimbursement process of the claim amount. Once the insured gives the subrogation rights to the insurer, the insurer becomes entitled to claim the lost amount from the third party.

It is generally classified into three types:

- Equitable: The legal doctrine allows the insurance company to recover the claims from the third party that causes damage to the insured. The provision is not possible during unforeseen circumstances, such as natural disasters.

- Contractual or conventional: It is a written contractual arrangement between both parties, i.e., the insurer and the insured. It gives the rights to the insurance company on behalf of an insurer to sue the third party once the policyholder transfers the right to the insurance company to recover the claims. At times, the insured would not want to continue with contractual subrogation, so the insurance company has the right to file a lawsuit against the third party.

- Statutory subrogation: It does not involve the insurance company at the time of the accident or a loss. Instead, there is an amicable decision between the insured and the third party to settle claims and recover the losses without involving the insurer.

Examples

Let us look at some examples to understand the concept better:

- Jim drives his car towards Vermont Road. Unfortunately, on his way, his car met with an accident with Keith’s car. As a result, Jim’s car gets damaged, and the overall repairing charges amount to $5,500.To recover the losses, Jim contacts his insurance company XYZ Ltd. Since he had insurance for his car, he received the claimed amount of $5,500 from XYZ Ltd. Interrogation revealed that the accident occurred due to the fault of Keith (third party), who was responsible for rash driving and the car’s accident. Therefore, Jim’s insurance company XYZ Ltd. recovers $5,500 from Keith’s insurer or Keith due to his irresponsible behavior.

- Large insurance companies have collaborated to meet rising customer expectations in an age of fast-paced technology. For example, State Farm, a mutual insurance company based in the United States, and USAA, a financial services company based in San Antonio, United States, announced that auto subrogation claims settlement between two companies using blockchain technology. In addition, both the companies announced advanced testing of a blockchain solution to automate the time-consuming and paper-intensive subrogation claim processing.

- Let’s take a look at an example associated with non-permissive use circumstances. A and B are friends, and B used A’s car without permission. In some cases, B’s auto insurance will act as the primary coverage instead of A’s even if A’s insurance limit is sufficient to cover the damage.

Waiver of the Subrogation

A waiver of subrogation also refers to one of the subrogation clauses. It is a contractual provision where the policyholder waives the rights of an insurance company to recover claims from the third party who caused the damage. The waiver helps reduce the legal formalities such as lawsuits and countercases arising due to the claim. It is usually applicable in commercial, professional, property, and vehicle policies.

It increases the risk for the insured’s insurance company as waiving off the claims increases the cost of the policy with increased premiums. However, the insured needs permission or consent from the insurance companies before signing the waiver of subrogation letter with the third party.

Frequently Asked Questions (FAQs)

What is the meaning of subrogation in insurance?

In insurance, it refers to the right that most insurance companies have to take legal action against a third party that caused an insurance loss to the insured. It ultimately helps the insurer and insured to recover the cost associated with accidents due to the fault of a third party.

How to negotiate a subrogation claim?

Negotiation can take many forms, depending on the merits of the case and the parties involved. Negotiations should be structured and premised to make the settlement a win-win solution for both parties.

Is subrogation good or bad?

It is good because it allows insurers to recover costs from third parties, which helps to keep overall insurance costs low. In addition, it benefits both insured and insurance companies by ensuring that third parties are held accountable for the damage they cause.

Recommended Articles

This article is a Guide to Subrogation and its Definition. We explain the meaning of this principle in insurance, its examples, waiver, claims, and clauses. You can also go through our recommended articles on personal finance –