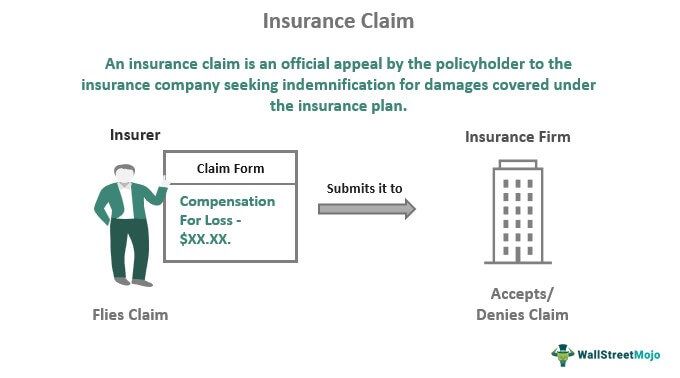

What Is An Insurance Claim?

An insurance claim is a formal request made by the policyholder to the insurer for compensation against losses covered in the insurance plan. It provides financial assistance to the policyholder during unfortunate circumstances. Moreover, the insurance claim adjuster helps discover a reasonable settlement offer for the same.

The insurer analyses the claim for credibility and, when approved, releases payment to the insured or claimant party (representing the insured). In addition, the most general types of claims are for life, health, homeowner, and car insurance.

- An insurance claim is an official request the policyholder makes to the insurance firm to get reimbursement for insured damages.

- It certainly aids cover unpredicted expenditures to lessen the financial distress of the policyholder amid an unfortunate event.

- Health, Life, Homeowner, and car insurance are the most popular types of claims.

- The claims process incorporates five stages. First, it encompasses disclosing the claim to the insurer, investigation by the adjuster, determining the coverage, maintenance and renovation, and final payment.

How Does An Insurance Claim Work?

An insurance claim attempts to inform the insurance company about the occurrence of the covered event for discharging the claim amount. It may cover incidental expenses, act as income replacements, and help the insured’s family settle their living costs to avert huge economic difficulties.

In the case of financial dependents, the insurance claim check might act as a helping hand for households lacking economic assistance due to unemployment or medical emergencies. Regarding life insurance, the nominee acquires financial security following the insured’s untimely demise.

There are two kinds of claim settlement techniques, replacement cost settlements, and actual cash value settlements. While the former covers the restoration and replacement cost, the latter thoroughly depends on the depreciation type and offers the depreciated cost of the item.

Several factors control the claims procedure, which might entail calling the agent, sending reports, utilizing the firm’s app, or a mixture of these steps. Also, it is based on deductible, i.e., how much the insured bears before the insurance carrier. The policyholder pays off the deductible, and the insurance provider reimburses the remaining amount.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Insurance Claim Process

Now, here are the steps to obtain the claim.

#1 – Disclosing Claim to the Insurer

The policyholders can report their claims both online and offline. After the insurance firm gets their claim, it will connect them with a claim adjuster for the right guidance through the procedure.

#2 – Claim Inquiry by the Adjuster

The insurance claim adjuster asks for the information needed to complete the investigation and release the check. Thus, the insured must list all the valuable information comprising photos or videos, take the adjustor to the loss scene, and recognize important witnesses.

#3 – Deciding the Coverage

The adjuster examines the insurance plan to verify whether the loss is covered (completely or partly) or uncovered.

#4 – Servicing and Renewal

Now, the repayment procedure can be initiated. Minor claims are managed effortlessly, while big losses likely involve contractors.

#5 – Claim Settlement

To clarify, the insurance company makes the final settlement and finances the cost of repairs up to the covered extent. It can also include mediation between the insurer and the insured concerning the amount in complicated claims.

Examples

Most importantly, let’s review a few examples to comprehend the concept.

Example #1

Say Claudia (insured) suffers from a major heart attack, and her husband David (claimant party) gets her admitted into the nearby hospital’s ICU. Now, David files the health claim to XYZ Insurance Co. (insurance firm) on behalf of Claudia and asks for indemnification of $55,000 ($50,000 for ICU, $5,000 for medications).

Once the insurance claim adjuster confirms it after adequate documentation, XYZ Insurance Co. justifies the claim and releases the check.

Example #2

On August 16, 2022, Credit Suisse (CS) declared the filing of 18 insurance claims by the asset management branch in connection with the Greensill-associated frozen supply chain finance funds (SCFF). In addition, it filed claims for the CS Nova (Lux) Supply Chain Finance High Income Fund and CS (Lux) SCFF.

These claims had a relative exposure of roughly USD 2.2 billion. Now, the claims are filed toward every SCFF program with insurable damages. Moreover, the bank will manage to rely on the insurer’s requests for details on the filed claims in a couple of months.

Insurance Claim Types

To clarify, below-mentioned are the four most typical categories of claims.

#1 – Life Insurance

The claimer files this type of claim after the insured dies. In addition, the claimer must present authenticated copies of the policyholder’s death certificate and suitable claim forms.

#2 – Health Insurance

There are different health claims, such as prescription medicines, operations, hospital admissions, emergency care, etc. Therefore, it assists protect patients against the economic burden of healthcare costs.

#3 – Homeowner Insurance

Under this type of claim, the insurance firm offers payment for covered damages like wind, wildfire, hurricanes, tornadoes, etc., as approved by the claim adjuster. The insured must instantly communicate with the insurance company to acquire prompt repayment after the mishap.

#4 – Car Insurance

Notwithstanding who was at fault, the policyholder must file for the car insurance claim in case of an accident. It may vary from personal injury and coverage for the rental car throughout the service period to loss of vehicle value and indemnity against property reconstruction.

Please note that the listing is non-comprehensive and can incorporate natural disasters, unemployment insurance claims, etc. Policyholders can also apply for third-party insurance if harmed due to someone else’s fault.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What Happens When An Insurance Claim Is Made Against You?

When an insurance claim is made against you, the third-party demands compensation for injuries in a tragedy involving you. The claimed losses may incorporate a physical injury with a doctor’s bill and claims for suffering and distress and income loss.

Can You Cancel An Insurance Claim?

Yes, you can cancel any claim, be it a car, Health, Property, or unemployment insurance claim. However, it would help if you connect with the insurer’s spokesperson for claim cancellation, as different insurers have different conditions.

Should I File Insurance Claim For Bumper Damage?

You should file an insurance claim for bumper damage only after contemplating the outcomes and the following factors,

– Possible injuries

– Involvement of another driver

– Expenses of damage in comparison with the deductible

Most importantly, you can consider filing the claim if you didn’t cause the accident, you can’t bear the costs, or when you need to fund liability coverage for another driver.

Recommended Articles

This has been a guide to What is Insurance Claim and its meaning. Here, we explain how it works, its process, types, and examples. You can learn more about it from the following articles –