Part of our Bond Pricing & Yield Curves guide

TED Spread Definition

TED spread refers to a numerical value representing the difference between the interest rates on interbank loans (three-month LIBOR) and the interest rate on three-month U.S. Treasury bills. Furthermore, TED is the acronym for Treasury-EuroDollar rate.

The strategy was initially established by trading Treasury bill futures against Eurodollar futures, with the same maturity. Both of the items in this scenario are for short-term interest rates in U.S. dollars. The spread approach is based on the assumption that the three-month rates would move in opposing directions. A situation of falling spread is always an encouragement to investors and vice versa.

Key Takeaways

- TED (Treasury-EuroDollar rate) spread refers to the difference between the interest rate on three-month U.S. Treasury bills and the three-month LIBOR.

- The formula to calculate the spread: Three-month LIBOR rate – Three-month Treasury bill rate. It is expressed in percent or base points.

- The technical indicator throws insight into the overall level of credit risk in the economy, and entities like banks use this tool to enhance the decision-making process.

- An increase in the TED spread indicates that the default risk on interbank loans is also increasing and vice versa.

How TED Spread works?

TED spread is disclosing the difference between the interest rate appearing when banks lend to each other for a three-month duration and the interest rate the government offers to the public for their three-month treasury bill purchase. It throws insight into the overall level of credit risk in the economy, investors’ trust and confidence in the financial markets, and the U.S. government. Hence banks and investors use this tool to enhance the decision-making process.

The U.S. Treasury bills generally are of short-term duration and backed by the government; hence they are considered a low-risk investment option. At the same time, LIBOR reflects the credit risk of lending to commercial banks. An increase in the spread indicates that the default risk on interbank loans is also increasing. Hence, interbank lenders demand higher interest rates and are ready to receive the lower interest rate from government treasury bills. Conversely, if the default risk decreases, the LIBOR rate and the spread decrease, and investors act accordingly.

The spread value normally moves between 10 bps and 50 bps. According to various scholars, if the spread value crosses 48 bps, it indicates an economic crisis. However, it rarely rises above 100 bps, and it can surge considerably higher in times of economic crisis. For example, the TED value reached a very high rate in the 2008 financial crisis. In October 2008, it crossed above 400 basis points. The values are discernable from the ted spread chart based on the ted spread Fred data. For example, the current value of the spread as of 21 January 2022 is 0.09%.

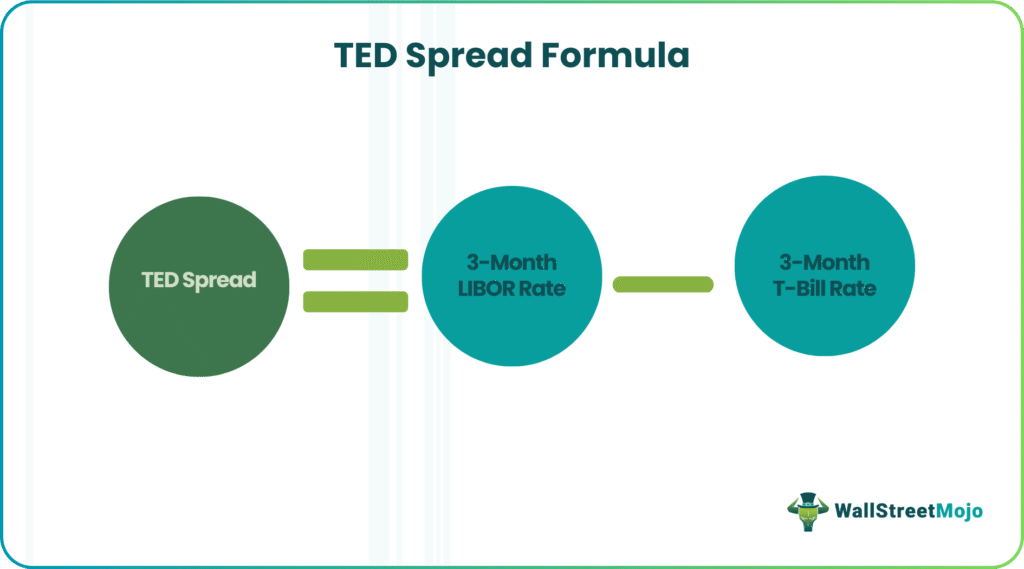

Formula & Calculations

The spread calculation is based on the following formula:

Let’s consider an example for better understanding the concept through calculation:

- Three-month LIBOR rate is 1.36%

- Three-month Treasury bill rate is at 0.92%

- TED spread = 3-month LIBOR rate – 3-month Treasury bill rate

= 1.36% – 0.92%

=0.44% (Percent)

=0.0044 (Decimal value)

=44 bps (Basis point) (1 Basis point is 0.01%)

How to Trade TED Spread?

It is challenging to time or beat the market, but there are many technical indicators with which an investor or trader can make good investment decisions and enjoy profits. One such indicator is the TED spread, but no investor should solely depend on it. Since banks are readily deciding to get off LIBOR and use a different rate, it is important to understand how it will affect its importance.

The spread indicator gauge the market and overall economic sentiment. If the yield curve steepens, it might indicate the market’s bullish orientation. It signals investors to invest specifically in banks. On the other hand, a flattening yield curve indicates a negative or recessionary trend. Investors should be wary of possible hazards returning to the credit market if the spread rises beyond 0.5 percent.

Frequently Asked Questions (FAQs)

What is a TED spread?

It refers to the spread between the three-month U.S. Dollar LIBOR interest rate and the three-month U.S. Treasury bill. TED is the acronym for Treasury-EuroDollar rate. The London Interbank Offered Rate, or LIBOR, is the foundational interest rate used in interbank lending on the London interbank market and acts as a baseline for determining interest rates on other loans.

Why is the TED spread important?

Investors use it to analyze the overall level of credit risk in the economy. Higher or increasing spread value points to the rising default risk on interbank loans and vice versa. Banks may change the interest rate offered during interbank lending based on the spread value.

What is ted spread today, and how to calculate it?

According to the observation from Fred Economic Data, the current value of TED Spread as of 21 January 2022 is 0.09%. It is derived by subtracting the three-month Treasury Bill interest rate from the three-month LIBOR interest rate based on U.S. dollars. Also, it can be represented in units like percent and base point. Traders also use online base point calculators to arrive at the spread value in base point units.

Recommended Articles

This has been a Guide to TED Spread and its Definition. We explain its formula & calculation, reference to Fred Ted spread chart, & today’s (current) value. You can learn more from the following articles –