Part of our Accounting for Leases guide

What Is Tenant Improvement Allowance (TIA)?

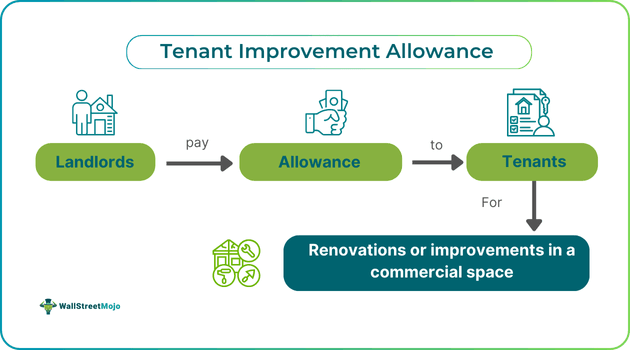

Tenant Improvement Allowance (TIA) refers to the funds allocated to tenants by the homeowners (landlords) for improvement purposes in a commercial space. The sole purpose of the TIA is to enable renovation and construction in the house (or property), intending to benefit the tenant.

A typical tenant improvement allowance becomes applicable as soon as the tenant moves into the property. If the house is not in a condition to live in, the landlord provides the tenant with this allowance to update the property (like doors, windows, or floors). The tenant pays for the improvement activities conducted in the property, and the landlord reimburses the amount incurred later on. TIA further has an accounting treatment in the books of both parties, followed by tax implications.

Key Takeaways

- Tenant improvement allowance refers to the reimbursement paid by the landlord to the tenant for improvements (renovations or constructions) made in a commercial space.

- When a tenant moves into a new property, the landlord agrees to pay this allowance to upgrade the property and benefit the tenant in the long term.

- The popular methods of calculating the TIA include per-square-feet-basis, percentage of total eligible costs, and fixed amount. The average square foot rate for TIA is $10-$40.

- Some of the common costs included under TIA cover hard costs like framing, doors and windows, electric wiring, plumbing fixtures, walls, and HVAC systems.

How Does Tenant Improvement Allowance Work?

The tenant improvement allowance is the remittance released to the tenant for renovation purposes on the property. This fund solely aims to retain the tenant’s interest in the rented space. Also, it helps attract lessees and ensures the leasing premises align perfectly with the tenants’ needs. Therefore, the tenant improvement allowance clause is very common in lease agreements. During negotiations, the landlord may include a TIA to support property construction if required. Once the work is completed, the owner reimburses the tenant for the agreed allowance amount. At times, the landlord may agree to TIA in exchange for a longer lease or even the removal of deferred payments, if any.

As per Accounting Standards Codification (ASC) 842, the accounting for tenant improvement allowance appears in the books of both landlord and tenant. However, before recording, it is necessary to look at the nature of the TIA asset and the relationship between landlord and tenant. If the TIA is provided to extend the useful life or fair value of the asset, it must be recorded separately. It does not attract any asset or liability for the tenant. On the contrary, for non-capitalizable improvements (cosmetic repairs like paints and lighting), the landlord must pay for the expenses incurred. This situation may or may not create a liability for the tenant, depending on lease terms.

Moreover, if the landlord gives the amount in advance, it will act as an amortization expense for the tenant. They can choose to amortize the shortest of either the useful life of the improvements or the lease term. If the tenant owns the improvements, they may treat it as capital expenditure. Since it is an expense made for assets like property, it acts as a capital expense that remains amortized for the rest of the life of the asset. However, there is no salvage (end value) obtained as the assets then remain with the landlord after the lease period.

Coverage And Exclusion

Even when considering accounting for the tenant improvement allowance, it is vital to know if the expenses account for TIA or not. Below is the required information to determine the items covered and excluded from this allowance.

#1 – Coverage

A typical tenant improvement allowance includes both hard and soft costs associated with the property leased out. Hard costs comprise those expenses that remain even after the tenant moves out, such as framing, doors and windows, electric wiring, plumbing fixtures, walls, and HVAC (Heating, ventilation, and air conditioning) systems. Apart from hard costs, soft costs include management fees, legal fees, and post-construction project expenses not directly related to the physical construction.

#2 – Exclusion

Costs that are usually excluded or ignored from the TIA include miscellaneous expenses applicable to the current tenant only. Costs related to furniture, inventory, equipment, and moving expenses do not fall under TIA coverage as such expenses do not benefit the landlord and are only meant to increase the productivity of the tenant. Likewise, any alternations outside the premises (or rented space) are also excluded. However, in some cases, there can be exceptions to any of these items if the tenant decides to reside for a long term.

How To Calculate?

The calculation of an average tenant improvement allowance depends on the expense and the square foot (sq ft) area of the property. It ranges from $10-$40 square feet. However, the TIA can drop to $10-$20 sq ft. This allowance amount is fixed, depending on other factors as well, including market conditions, the newness (condition) and type of the space, length of the lease, and financial budget.

There are three ways to decide the TIA amount. Let us look at them in brief:

- Fixed amount: In cases where the tenant has initiated the improvements, the landlord reimburses the fixed amounts. These are mostly 25% to 150% of the total first year’s rent. However, the amount applicable will depend on the condition of the space.

- Per-square-foot basis: Landlords also negotiate the TIA amount based on the per-square-foot basis method. This means multiplying the agreed sq. ft rate by the total square footage of the property space. For example, if the square footage area is 3,500 sq ft and the agreed rate is $10, then the TIA amount is $35,000 for the improvements occurring during the period.

- Percentage of total costs: Lastly, the percentage of total costs is also preferred as an alternative method of calculation. Here, the landlord uses this tenant improvement allowance calculator to calculate the renovation costs and determine the TI allowance. For instance, if the agreed rate is 50% and the total eligible expenses are $55,000, then the TIA is $27,500.

Examples

Let us look at the instances to understand different aspects of a tenant improvement allowance:

Example #1

Suppose James is a chef and wishes to operate his own restaurant business in the town. So, he contacts Stella to get a lease property for $50,000. However, the property requires some renovation in the lighting and cosmetic area. As a result, Stella agrees to an improvement allowance of $25,000 for the repairs listed. Following comprised James’s improvement plan:

- Painting: $5,000

- New flooring: $10,000

- Kitchen equipment (commercial-grade stove, refrigerator, etc.): $15,000

Total Estimated Cost: $30,000

After completing the above renovations, Stella reimburses James the agreed amount of $25,000, while James pays the rest $5,000 himself.

Example #2

In August 2024, the Coldwell Banker Richard Ellis (CBRE) analysis reported a reduction in free rent and TIA for the first time in the past four years. The length of free rent has dropped to 9 from 9.6 months since 2023. Also, the average tenant improvement allowance fell by nearly 3% to $94.69 per sq. ft. in the first half of 2024 from $97.55 in 2023. Furthermore, rents for the lower tier buildings dropped by 1.2% since 2023.

Tax Treatment

For most landlords and tenants, state and country laws have made tax treatment easy, considering the individual impact of TIA. For instance, the Tax Cuts and Jobs Act allows a qualified improvement property (QIP) to have a life of 15 years with bonus depreciation. This phase-out for QIP started in 2023 with an 80% reduction in bonus depreciation initially, and the rest (20%) continues each year until 2027.

These tax implications apply to the person actually paying the TIA amount. In short, the party paying and owning the improvements is eligible for taking deductions. Thus, if the landlord constructs and pays for improvements, they own the property and related depreciation. Hence, there are no tax implications for tenants.

Likewise, most lease improvements are tenant-specific, and if tenants make the payments and own the improvements, they receive a tax deduction; this tax treatment is also possible when the landlord does not reimburse the tenant for any TIA amount.

Frequently Asked Questions (FAQs)

Do we have to pay back the tenant improvement allowance?

No, there is no need to repay the TIA amount to the landlord for the improvements done. Instead, the premise holder will provide the same to the tenant unless it is an amortized TIA. An amortized TIA occurs when the improvement allowance is combined with the loan.

Can we capitalize on the tenant improvement allowance?

Capitalization of costs refers to the scenario where the cost appears on the asset side of the balance sheet and when the depreciation in TIA is applicable if certain conditions are met. If improvements occur in long-term assets, adding value to the property and capitalizing the cost are possible. Landlords can also capitalize on TIA if the amount paid to the tenants exceeds the amount the latter pays for the improvements.

Is it necessary to issue a 1099 for tenant improvement allowance?

If the tenant (or lessee) has paid for any improvements the landlord was supposed to make, the tenant must fill out form 1099 in that case. However, issuing and filing a 1099 is vital only when the commercial space has a business name rather than an individual’s name.

Is tenant improvement allowance a lease incentive?

Yes, TIA is a type of lease incentive made to or on behalf of the lessee. It provides sufficient funds to the tenant to cover the costs arising from the premise improvements.

Recommended Articles

Continue with these closely related articles from the same guide.