Part of our Accounting Concepts guide

What Is Accounting Equation?

The Accounting Equation is the primary accounting principle stating that a business’s total assets are equivalent to the sum of its liabilities & owner’s capital. It is also known as the Balance Sheet Equation & it forms the basis of the double-entry accounting system.

Accounting Equation Formula Excel Template

Download Excel Template

Accounting Equation is based on the double-entry bookkeeping system, which means that all assets should be equal to all liabilities in the book of accounts. All the entries made to the debit side of a balance sheet should have a corresponding credit entry on the balance sheet. Thus it is also known as the balance sheet equation.

- The accounting equation is a fundamental accounting principle that states that the total assets of a business are equal to the sum of its liabilities and owner’s equity. It forms the basis of the double-entry accounting system.

- The accounting equation is based on the double-entry bookkeeping system, which means that for every transaction recorded in the accounting system, the total debits must equal the total credits.

- The accounting equation is also known as the balance sheet equation. All entries to the balance sheet debit side must have a corresponding credit entry on the balance sheet, ensuring the equation remains balanced.

Accounting Equation Explained

The concept of accounting equation show us the main principle of accounting and represents the relation between assets, liabilities and equity. According to the equation, the assets of the business are equal to the equity and liabilities.

The assets of a business show the resources that the company has in the form of property, machinery and equipments, inventory, cash, etc. the liabilities are the obligations of the business or the funds that it owes to outsiders like creditors, investors, etc, in the form of loan, accounts payable or taxes.

The equity consists of the contribution of the owner and the retained earnings. The accounting equation format is the main foundation of the double entry system followed in accounting process. According to the system, every transaction has two effects, a debit and a credit that are equal and opposite in nature.

If we take the example of loans taken by the company, the asset side will increase by the amount of loan, but the liability side will also increase since the loan is a liability for the business which it has to pay back to the lenders.

Formula

The equation is an important concept used to assess the financial condition of the company. The formula for calculation is given below.

Assets = Liabilities + Shareholders Equity

The above accounting equation format provides the management and the stakeholders a clear snapshot of the asset, liability and equity position at a particular point of time.

How To Calculate?

Let us understand the different components of the equation in detail which will facilitate in understanding the calculation done by companies.

- Assets: This is the value of a company’s items; they may be tangible or intangible but belong to the company.

- A liability: This is a term for the total value that a company must pay in the short term or the long term.

- Shareholders’ Equity: Shareholder’s Equity is the amount of money a company has raised through its issue of shares. Alternatively, it is also the amount of retained earnings of a company. As the shareholders invest their money in the company, they must be paid with some amount of returns, which is why this is a liability in the company’s account books.

Hence, the total assets should always be equal to the total liabilities in a balance sheet, which fundamentally forms the basis of the whole accounting system of any company when it follows the double-entry bookkeeping system. Thus from the above details we can understand how to do accounting equation.

Rules

The equations has certain rules that every company should follow. They give us guidelines regarding how to do accounting equation.

- It is understood that the double-entry book-entry accounting system is followed globally and adheres to the rules of debit and credit entries. These entries should tally to each other at the end of a particular period, and if there is a gap in total balances, it needs to be investigated.

- This system makes accounting a lot easier by creating a relationship between the expense/liability and cause of expense/liability (or income/asset and source of income/asset). We need to understand the underlying concept and thumb rule of accounting, which relates to debit and credit entries at the root level.

- Another rule is that the total amount written on the debit of the transaction should be equal to the amount in the credit side. This will ensure that the equation balances.

- Any increase in the assets and expenses will be debited and increase in liability, revenue and equity will be credited.

- Similarly, any fall in assets and expenses are credited and fall in liabilities, revenue and equity are debited.

- Although the accounting equation formula seems like a one-liner, it contains a lot of meaning and can be explored deeper with complex expense entries.

The accountants should ensure that the concept of accounting equation and its rules are properly followed and the transactions are daily and accurately recorded.

Examples

Let us understand the concept with the help of an example.

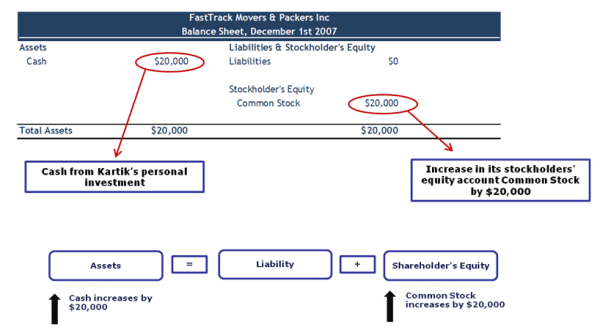

Example #1

On December 1, 2007, Kartik started his business, FastTrack Movers and Packers. The first transaction that Kartik will record for his company is his investment of $20,000 in exchange for 5,000 shares of FastTrack Movers & Packers common stock. There are no revenues because the company earned no delivery fees on December 1, and there were no expenses. How will this transaction get recorded in the balance sheet?

Cash & Common Stocks

- Common Stock will be increased when the corporation issues shares of stock in exchange for cash (or some other asset)

- Retained Earnings will increase when the corporation earns a profit, and there will be a decrease when the corporation has a net loss

- Core link between a company’s balance sheet and income statement

Example #2

A double-entry bookkeeping system helps us understand the flow of any particular transaction from the source to the end. Let’s take another basic, expanded accounting equation example.

When there is a purchase of an asset in a company, the purchase amount should also be withdrawn from some account in the company (generally a Cash account). Hence, the account from which the amount is withdrawn gets credited, and there needs to be an account debited for the asset purchased (the account related to the asset purchased gets debited).

Consider the below entries:

- On December 27, Joe started a new company by investing $15,000 as equity.

- On January 3, Joe purchased an office table for his company, which cost him $5,000.

- He paid wages for his labor on January 5, totaling $15,000.

- On January 10, he received a contract from his clients, and they paid him $2,000.

- On January 13, Joe received another contract for which the client paid $4,000 in advance.

- On January 15, he completed the service contract received on January 13, and the client paid the remaining amount of $8,000.

The Journal entries for the above transactions are as below:

| Date | Account Description | Debit | Credit |

|---|---|---|---|

| 27-Dec | Cash | $15,000 | |

| Shareholders Equity | $15,000 | ||

| 3-Jan | Office Table | $5,000 | |

| Cash | $5,000 | ||

| 5-Jan | Wages Expense | $15,000 | |

| Cash | $15,000 | ||

| 10-Jan | Cash | $2,000 | |

| Service Revenue | $2,000 | ||

| 13-Jan | Cash | $4,000 | |

| Accounts Receivables | $8,000 | ||

| Service Revenue | $12,000 | ||

| 15-Jan | Cash | $8,000 | |

| Account Receivables | $8,000 | ||

| Total | $57,000 | $57,000 |

The corresponding entries in a balance sheet as of January 15 should be as below:

| Assets | Amount | Liabilities | Amount |

|---|---|---|---|

| Cash | $9,000 | Service Revenue | $14,000 |

| Furniture A/C | $5,000 | ||

| Total | $14,000 | Total | $14,000 |

It is seen that the total credit amount equals the total debt amount. It is fundamental to the double-entry bookkeeping system of accounting, which helps us understand from the illustration above that total assets should be equal to total liabilities.

In this illustration, Assets are – Cash, Furniture A/C, and Accounts Receivable; Liabilities are Wage expenses and Service Revenue.

If we refer to any balance sheet, we can realize that the assets and liabilities and the shareholder’s equity are represented as of a particular date and time. Hence, as of January 15, only three accounts exist with a balance – Cash, Furniture A/C, and Service Revenue (the rest get net off during the period of the whole transaction by January 15). Only those accounts that exist with a balance (positive or negative) on a particular date are reflected on the balance sheet.

Alternatively, we can also understand that total liabilities can be derived if the only asset value is mentioned. The owner’s equity can also be determined if total assets and total liabilities are available. The basic accounting equation formula can also be used as below:

Total Liabilities = Total Assets – Shareholders Equity

Shareholders Equity = Total Assets – Total Liabilities

Hence, this forms the basis of many analyses for market investors, financial analysts, research analysts, and other financial institutions.

Accounting Equation In Income Statement

→ Explore all 32 Income Statement articles

Not only does the balance sheet reflect the basic accounting equation as implemented, but also the income statement.

- An income statement is prepared to reflect the company’s total expenses and total income to calculate the net income for different purposes. This statement is also prepared in the same conjunction as the balance sheet. However, a little differently applied.

- Here, we do not have total assets and liabilities. Still, the statement is prepared so that if an expense is credited, it will have an equal and opposite entry in debt in a related ledger account.

- The income statement includes the accounts which directly refer to a company’s income or expenses like Cost of Goods Sold, Tax expenses, and Interest Payable expenses.

Problems

There are some problems that company may face with implementing the accounting equation approach. They are given below:

- Asset valuation – The accuracy of the equation can be affected by the valuation of assets. It is often very difficult to accurately value them and different companies use different methods for this purpose.

- Accrual accounting – the equation assumes that every transaction is recorded based on accrual method of accounting. It means the expenses and revenue is recorded as and when they are earned, not when cash actually changes hands. This can create discrepancies between cash and accrual accounting, affecting the equation.

- Transaction timing – The accounting equation approach assumes that all transactions are recorded as and when they occur. But accountants may not always be able to record them on exact date of time, thus giving rise to timing problems or gaps.

- Non -monetary transactions– There are transactions that are non monetary in nature like some cases of services. They are difficult to value and may not reflect correctly in the equation.

Thus, these problems should be noted by all companies and strict method of valuation and recording of transactions should be done to control such problems.

Frequently Asked Questions (FAQs)

Which financial statement uses the expanded accounting equation?

The financial statement that uses the expanded accounting equation is the balance sheet. The expanded accounting equation provides a more detailed breakdown of the balance sheet’s components, including assets, liabilities, and equity.

What is an accounting equation cheat sheet?

An accounting equation cheat sheet is a reference tool that summarizes the accounting equation and its components. It can be helpful for students or professionals who need to quickly refer to the equation and its related formulas and concepts.

What are the objectives of the accounting equation?

The objective of the accounting equation is to provide a framework for recording and reporting a company’s financial transactions accurately. By ensuring that the equation remains in balance, companies can track changes to their assets, liabilities, and equity over time and ensure the accuracy of their financial statements. The accounting equation also helps companies make informed business decisions by clearly showing their financial position and performance.

Recommended Articles

This article has been a guide to what is Accounting Equation. We explain its formula along with examples, problems, rules & how to calculate it. You may also have a look at the following basic accounting articles for gaining further knowledge –