Debit Meaning

Debit represents either an increase in a company’s expenses or a decline in its revenue. There is either an increase in the company’s assets or a decrease in liabilities. Debit is the part of a financial transaction recorded on the left side column.

This word is derived from the Latin, “debere,” which signifies “to owe,” therefore commonly abbreviated as “Dr” in financial transactions. In the double-entry system, every debit value is accompanied by an equal credit amount to counterbalance the entries.

- Debit is contradictory to credit. This means credit is recorded on the right side of the financial book.

- Debit is the part of a financial transaction recorded on the left side of accounting books. The records follow the double-entry bookkeeping system. Its accounting abbreviation is “Dr”

- It exhibits an upsurge in expenses. At the same time, it shows a decline in revenue.

Debit in Accounting Explained

It is an essential component of accounting. Be it journal entries, ledger accounts, Trial balance, income statements, cash flow statements, or balance sheets; every accounting book has a left side or column recognized as Debit. To understand its significance, we need to understand its application as per standard accounting rules.

Listed below are the account types and conditions:

#1- Increase in Assets:

Additions to a company’s fixed or current assets are recorded as debited items. These include cash, cash equivalents, receivables, building, machinery, and stocks. For example, if a construction company buys a crusher, then it is an asset for the business and will appear on the debit side of the books.

#2 – Decrease in Liabilities:

Whenever there is a decline in bonds, loans, payables, mortgages, accrued expenses, or deferred revenue, it is mentioned as a debited item. Suppose a company pays off its bondholders, then this reduction in liability, i.e., bond, appears on the left side.

#3 – Decrease in Equity:

The owner’s equity or invested capital decreases when the company goes into a loss. Equity also decreases when the owner withdraws funds for some reason. Therefore, it is shown as a debited item. For instance, if one of the partners disinvests his funds from a company, the diminished equity will be recorded on the left side.

#4 – Increase in Expenses or Loss:

A corporate expense consists of salary, rent, insurance premium, advertising, and electricity bills; all shown as debited items. Similarly, any loss incurred would be recorded as a debited item. For example, if an organization pays rent to the premises owner, the rent will be shown as a debited item.

#5 – Decrease in Income or Revenue:

Revenue refers to income from operations and non-operating income, i.e., interest received, tax rebate, royalty, rent received, etc. The left side of accounting books records a decline in these revenue items. For example, in sales return, the sales account is treated as a debited item.

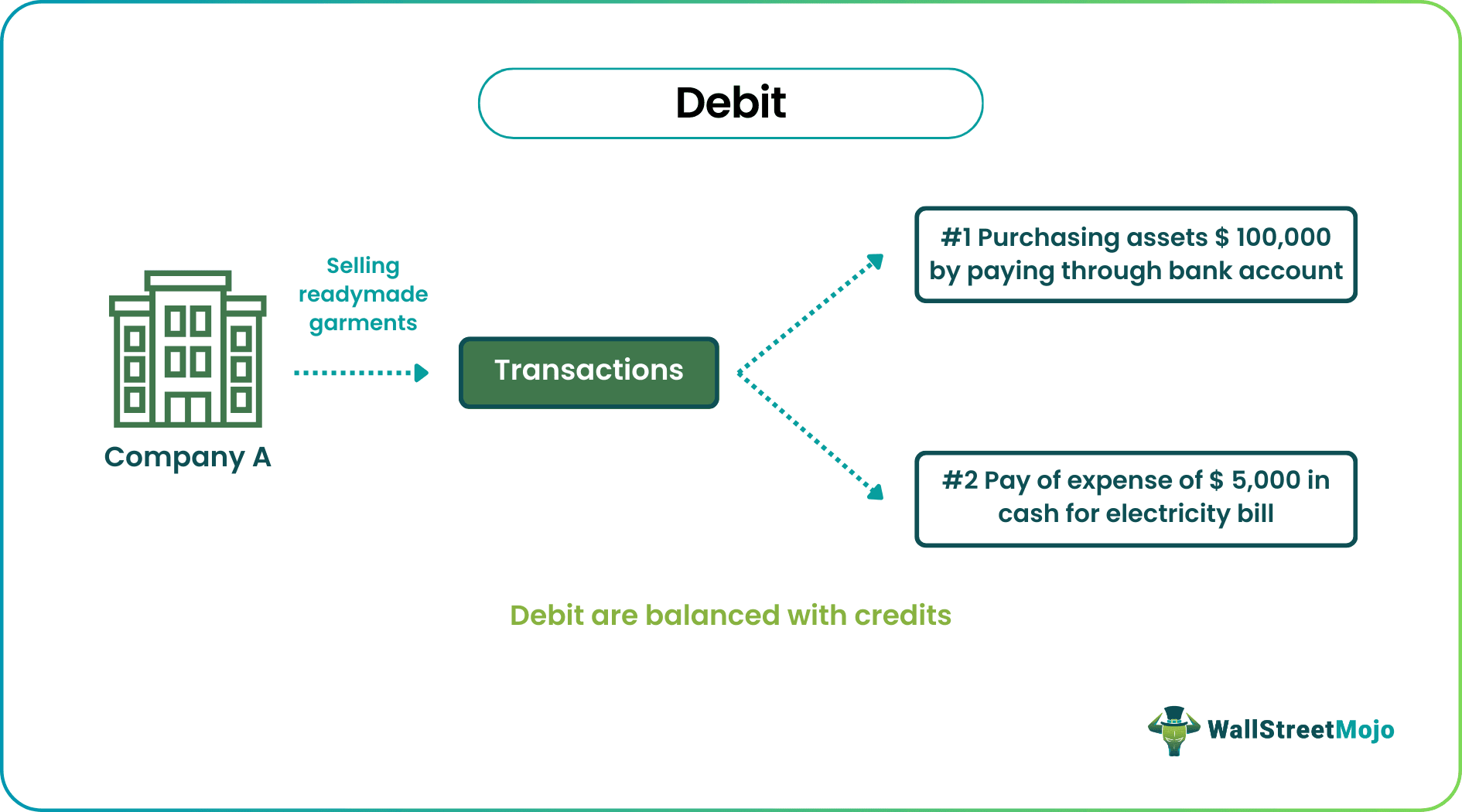

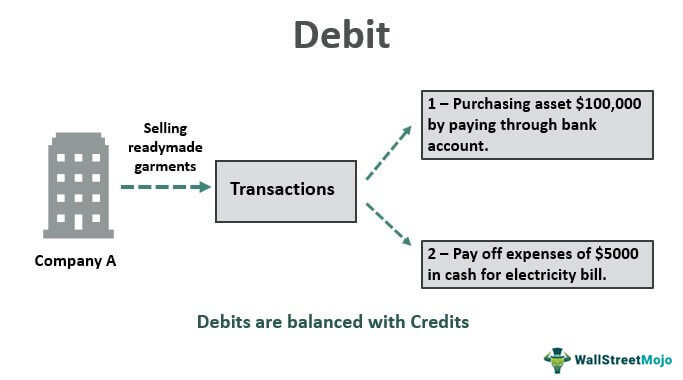

Example of Debit Entry in Accounting

To further understand Debited items in accounting, consider the following example.

A. ltd. Deals in readymade garments. The company purchased machinery worth $ 100,000 by cheque and paid off the electricity bill of $ 5,000. How to record the transaction in the books of accounts, and what accounts will be debited?

Solution:

Below will be the accounting treatment for the transactions:

#1 Purchase of machinery worth $ 100,000 by check

In this case, there is an addition of one asset, i.e., machinery; therefore, the entry will show a debited item. But, at the same time, another asset, the bank account, will be entered as credit because there is a decrease in its balance.

| Particular | Debit ($) | Credit ($) |

|---|---|---|

| Machinery A/c Dr. | 100000 | |

| To Bank A/c (Machinery purchased) | 100000 |

#2 Paid electricity bill of $ 5,000 in cash

Here, the electricity bill is entered as a debited item because the company’s cost increased by $5,000. In contrast, the cash account will be entered as credit as there is a decrease in cash assets.

The journal entry would be:

| Particular | Debit ($) | Credit ($) |

|---|---|---|

| Electricity Bills A/c Dr | 5000 | |

| To Cash A/c (Electricity bill paid) | 5000 |

Real-World Applications

Debited entries are commonly made in finance and banking as well. The term has various real-world applications. For example, a debited balance shows excess debit total over the credit total.

A debit card is a form of plastic money used to withdraw funds from a checking account through an ATM. A checking account is usually a savings or a current account. It can also be used to transfer money, pay loans, or buy products electronically. This expense comes from the cardholders’ balance. Whereas a credit card is also plastic money, but the user doesn’t spend the saved or deposited funds. Instead, the amount withdrawn through such a card is loaned. It is a credit offered by the financial institution. This amount is to be repaid with interest within a narrow timeframe.

Debit and Credit in Accounting

According to the double-entry system of accounting, every transaction is recorded in at least two different accounts. When assets are recorded as debited items, it signifies an increase in assets. However, when liabilities are entered as debited items, there is a decrease in liability.

Equity debited represents a decrease, income debited represents income decrease. In contrast, if an expense is recorded as a debited item, the company’s expenses increase.

Alternatively, if an asset is credited, it reflects a decrease in the asset. For example, the credit amount could be from the partial sale of the asset. When liability is recorded as a credit, it represents an increase in liability. Similarly, equity credited signifies an increase.

| Account Type | Increase | Decrease |

|---|---|---|

| Asset | Debit | Credit |

| Liability | Credit | Debit |

| Equity | Debit | Credit |

| Expense | Credit | Debit |

| Income | Credit | Debit |

In banking, a debit shows the decrease in account balance. A debit balance refers to a negative balance in the checking account. In other words, the customer has overdrawn. In contrast, credit represents the deposit or increase in an account balance. The credit balance indicates a positive or surplus fund in the checking account.

Let us now go through a simple accounting transaction example to understand both sides. A company purchases goods worth $12500 from ABC Ltd. and immediately pays $5000 in cash. The following journal entry is made in the company’s books:

| Particular | Debit ($) | Credit ($) |

|---|---|---|

| Goods A/c Dr | 12500 | |

| To Cash A/c | 5000 | |

| To ABC Ltd. A/c (Goods purchased and $5000 paid in cash) | 7500 |

In the above example, goods are an asset recorded as debited items. This is because buying goods results in increased assets. Paying in cash decreases cash assets; therefore, it is a credit entry. Now ABC Ltd. is a creditor to the company, which is a liability. Thus, an increase in liability is a credit entry.

Frequently Asked Questions (FAQs)

What is a debit account?

It is an asset or expense account that has a trial Balance. It allows the holders to deposit funds to purchase products or services. A balance shows the amount that can be spent for the purchase of products and services. For example, if a company purchases a building, then this asset is shown on the left side of the Balance Sheet.

Is expense a debit or credit?

The accounting rule says all expenses or losses are recorded on the left side; thus, any cost or loss is considered a debit.

Is Debit positive or negative?

Debit is a positive item on the Balance Sheet. In contrast, on a result item, it turns out to be on the negative side.

Recommended Articles

This article has been a guide to Debit and its definition. Here we discuss an example of the debit entry along with applications and types. You can learn more about accounting & bookkeeping from the following articles –