Part of our Budgeting and Planning guide

Budgetary Control Meaning

Budgetary control is known as setting up a particular budget by management to know the variation between the company’s actual performance and budgeted performance. It also helps managers utilize these budgets to monitor and control various costs within a particular accounting period. The change in production, sales, or any function within the organization will impact the control functions.

Budgetary control techniques involvea process of planning and controlling all the functions of an organization through comparison and analysis of budgeted numbers to actual results. Comparing the budgeted numbers with actual results identifies the areas that need improvement and where cost reduction is feasible or budgeted numbers need to be revised.

Budgetary Control Explained

Budgetary control is a crucial financial management tool that allows organizations to plan, monitor, and manage their financial resources effectively. It involves creating a detailed budget that outlines expected revenues and expenses over a specific period.

Once the budget is in place, ongoing monitoring and comparisons with actual financial performance are conducted. This process helps in identifying discrepancies and allows for timely corrective actions to be taken.

A budgetary control system aids in financial decision-making, cost management, and overall organizational performance improvement. It enables companies to stay on track with their financial goals and make necessary adjustments in real-time to achieve financial stability and success.

The basis of cost allocation becomes important at micro-level analysis, so if there is a change in the basis of cost allocation, it should be analyzed fully before putting it in place. It identifies if there is any issue or chance of improvement with input material procurement, the desired output from the material, any processing issue, or sales team administration. So, to understand the business functions completely and root causes analysis of various outcomes, budgetary control is one important tool in the hands of parties associated with the organization.

Objectives

Let us discuss the objectives of budgetary control systems through the explanation below.

- Budgetary control sets the stage for a well-structured financial plan, providing a roadmap for how financial resources will be allocated and utilized over a specific time frame.

- It assists in defining clear financial goals and objectives for an organization, allowing for a shared understanding of what needs to be achieved.

- Budgets allocate resources efficiently by assigning funds to different departments and projects based on their strategic importance and financial requirements.

- Budgets act as benchmarks for measuring actual financial performance against planned figures. This evaluation helps identify areas where performance deviates from expectations.

- By highlighting areas of cost overruns or inefficiencies, budgetary control supports proactive cost management measures to ensure that financial resources are utilised optimally.

- It aids in informed decision-making by providing financial insights and data to guide choices about investments, cost-cutting, and resource allocation.

- Budgets enable organizations to assess the profitability of different segments of their operations, helping them focus on the most lucrative areas.

- It assists in maintaining a healthy cash flow by forecasting revenue and expenditure, ensuring that the organization can meet its financial obligations.

- Budgetary control fosters a culture of continuous improvement by identifying areas for operational enhancement and efficiency.

Types

There are various types of control an organisation can implement depending on the nature of the business, developmental stage, and management style. Let us understand the different types of budgetary control techniques through the detailed discussion below.

#1 – Operational Control

It covers the revenue and operating expenses, which are essential to running a day-to-day business. The actual numbers to a budget are compared monthly in most cases. It helps achieve control over EBITDA – Earnings before interest, taxes, depreciation, and amortization.

#2 – Cash Flow Control

This is an important budget that controls the working capital requirement and cash management. Therefore, cash crunches could be detrimental to everyday functioning, which is an important aspect.

#3 – Capex Control

It covers capital expenditures, like buying machinery or constructing a building. Because it involves a huge amount of money, the control here helps eliminate waste and reduce costs.

How is It Prepared?

The budget is prepared based on previous expenses and considers any foreseeable expenses that are bound to occur. Nowadays, in a computerized environment, financial statements are prepared in Excel sheets. We have the option of selecting the quarterly average or yearly average.

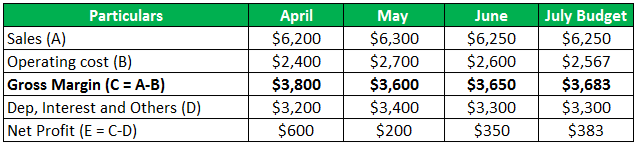

For example – if we want to prepare the budget for July 2019 based on Q2 results, it will look like this –

- Here, July Budget Formula = (April + May + June)/3, i.e., the average of April, May, and June.

- Based on April, May, and June’s actual results in the above table, we expect the sales to be $6,250 and the net profit to be $383 for July.

Now let’s assume that we got actual results for July and compare them with the July Budget to get the difference –

In this case, the actual sales for July have exceeded the budget by $150. This could be because more quantities were sold or the sales price per unit has increased slightly. If the sales price per unit remained constant in July, it means that the sales team has performed better than average, which is why sales have increased.

Further analysis will show which region and which product the sale has increased. In the same way, the operating cost has gone up by $33, which could be due to an increased cost of any input material or incidental to extra sales.

Importance

Now that we understand the intricacies of a budgetary control system, let us understand its importance through the points below.

- Budgetary control instills financial discipline within an organization by setting clear spending limits and financial goals, which, when adhered to, prevent unnecessary expenses and financial mismanagement.

- It helps organizations align their financial resources with strategic objectives, ensuring that financial activities are focused on achieving predefined goals.

- Budgets enable effective allocation of resources, ensuring that departments and projects receive the necessary funding to meet their targets.

- By providing a basis for performance evaluation, budgetary control allows organizations to identify variances between planned and actual results, aiding in early corrective actions.

- It facilitates cost control by monitoring and managing expenses, preventing overruns, and optimizing cost structures for enhanced profitability.

- Effective budgeting ensures healthy cash flow, reducing the risk of financial crises and enabling organizations to meet their financial obligations on time.

- Budgets promote employee motivation and accountability as they establish clear performance expectations and financial targets.

- Budgets provide transparency and accountability, fostering trust among stakeholders, including investors, lenders, and shareholders.

Advantages and Disadvantages

Most concepts and phenomenon in finance and life in general have two sides of the coin. Let us discuss the advantages and disadvantages of budgetary control techniques through the explanation below.

Advantages

- An effective tool for performance measurement of departments, individuals, and cost centers;

- Identification of areas for reduction and efficiency improvement;

- Increased efficiency and cost reduction result in profit maximization;

- It also helps in introducing incentive schemes based on performance.

- Cost reduction is always the primary target.

- Improves coordination between departments as the results and costs are interrelated.

- It provides insight for in-depth analysis and any corrective action.

- Helpful in achieving an organization’s long-term goal.

Disadvantages

- Budgeted numbers often need revision as future prediction is difficult.

- Time-consuming and costly process, need people and resources Budgetary control processes.

- This process sometimes requires coordination between various departments and is a difficult task.

- This process requires approval and support from top senior management.

- Always comparing the actuals with a budget is detrimental to employees’ motivation.

- Ignores demographics and many other economic factors

- Government policies and tax reforms are not always predictable

Budgetary Control Vs Standard Costing

Let us understand the differences between budgetary control system and standard costing through the comparison below.

Budgetary Control

- It emphasizes financial planning and setting targets for overall revenues and expenses.

- Primarily concerned with monitoring an organization’s financial performance against its budgeted figures.

- Typically looks at financial performance over a specific period, such as a fiscal year.

- Widely used in planning and controlling an organization’s overall finances and operations.

- Allows for adjustments to the budget as circumstances change, providing a broader perspective on financial management.

Standard Costing

- It centres on setting predefined costs for individual products, services, or activities within an organization.

- Concerned with monitoring and analyzing the actual costs of producing goods or services against predetermined standard costs.

- Often assessed on a more granular, ongoing basis, measuring efficiency and cost control for specific operations.

- Commonly applied in manufacturing and production settings to control costs and improve operational efficiency.

- Typically involves fixed standard costs, which may not be adjusted easily, providing a more detailed perspective on cost management at the operational level.

Recommended Articles

This has guide to Budgetary Control and its meaning. Here we explain its objectives, types, and advantages and compare it with standard costing. You can learn more about budgeting from the following articles –