Part of our Budgeting and Planning guide

What Is A Master Budget?

A master budget can be defined as the aggregation of all the lower level budgets, which are calculated by various functional areas of the business and is a strategy that documents the financial statements, cash flow forecast, financial plans, and capital investments.

Master budget accounting becomes a tool for the management to identify its goals well in advance and channel the organization’s resources towards them. It provides a rough guideline for the company’s near-term expectations. It should be noted that the budget should be prepared with the utmost caution as it affects the operational performance of the entire organization.

Master Budget Explained

A master budget combines numerous expenses and expected income figures in one place to get a complete overview of the finances. Through this type of budgeting, they become aware of their financial obligations along with what remains with them after all deductions. This helps firms to decide on the allocation of assets and resources for business activities wisely, keeping in mind what to reserve for emergencies in the upcoming fiscal year.

In a company, various departments carry on different functions, and each of them prepares a budget, forecasting the expenses and revenues estimated to incur. It includes budgeted financial statements, forecasted cash flows, and financial planning estimates made by the company. Every company has set targets and goals for each year, and it is through these budgets the company prepares the plan of action to achieve them.

The various budgets which are ultimately rolled up within a master budget are the direct labor budget, direct material budget, finished goods budget, manufacturing expenses budget, production budget, sales budget, cash budget, capital asset acquiring budget and selling, and administrative budget. It can be presented in the monthly or quarterly form as per the requirement and covers the entire fiscal year.

Purpose

Understanding the purpose makes the master budget definition and process clearer. It is a planning tool used by the management to direct and judge the performance of the various responsibility centers that reside within an organization to have proper control. This budget undergoes multiple iterations before it gets approved by the senior management to allocate funds accordingly. This budget is prepared under the guidance of the Budget director, which is usually the Controller of the company.

The central aspect to remember about this budget is the sum of all the individual budgets made within separate departments, thus providing a vital link between sales, production, and costs. It helps to ensure that all the departments work together to achieve the common objective of the overall business.

Components

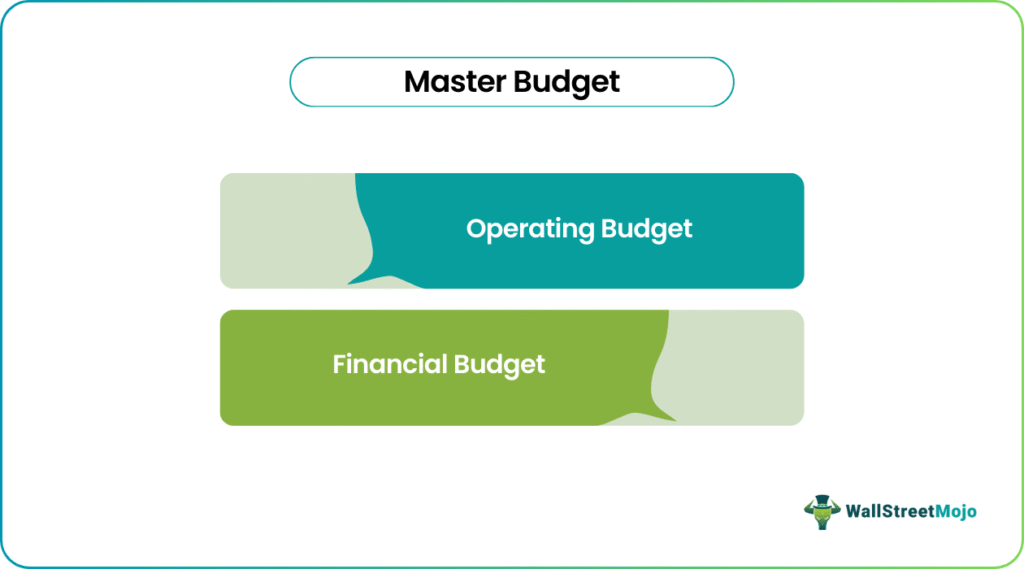

The main master budget components are the operating budget and the financial budget.

#1 – Operating Budget

It is related to the firm’s operating activities and includes the revenues generated and expenses incurred. This is presented in the form of the budgeted income statement representing the income-generating activities carried on within an organization.

#2 – Financial Budget

It shows information about the financial position of the firm. It also represents the cash budget, which gives information about cash availability. The financial budget is prepared by making a budgeted balance sheet that uses the operating budget information.

Example

When a company undergoes the merger and acquisition process, then the master budget is prepared to see what the company gains from the transaction of acquiring the target company. For instance, every company has an HR and Admin department. Therefore, when a company is acquired, this would result in two staff members in the same category.

Here, the company has to make the budget to decide who to keep and who to let go of for the betterment of the business. Thus, the management must prepare this budget before making any expansion plans. Thus, the master budget has detailed information about the future financial statements and cash flows estimated after considering current loan rates, cash flows, and debt limits.

Advantages

- It acts as a motivation to the staff as they can judge the actual performance with the desired one and thereby know the areas of improvement.

- It serves as a summary budget for the owners as they know what the business is estimating to earn and what it would incur to reach the goals.

- Since the budget is an estimate for the entire year, it helps identify the problems in advance and thus provides the management with the time to fix them. Therefore, it helps in overall planning in advance.

- With the proper budget, it helps to estimate the short-term and long-term goals of the organization and achieve them with proper channelizing of the resources.

Disadvantages

- While estimating cash or making a cash budget, it gets challenging to forecast the net change in working capital from one period to another. When the company is in the growth phase, the working capital could decline heavily, resulting in negative numbers due to cash outflow as investments increase. Thus, taking a steady number for working capital creates problems for management as it results in an unrealistic result in case the company is in the growth phase.

- A similar issue arises with an inventory. If the company forecasts more sales, this will increase inventory, resulting in negative working capital.

- Generally, while compiling the budget, to achieve the set budget, the employees lower the sales and estimate the higher expenses as management forces the organization to adhere to the budget, thereby deviating from the organization’s goals.

- Having a master budget leads to additional overhead expenses. The organization needs an additional financial analyst who could track the variances and prepare a detailed analytical report on deviations.

- Managers are more focused on achieving the budget goals; as their incentives are tied to it, they ignore new opportunities.

- Another problem with the master budget is that it is not easy to modify. Even a small alteration requires a lot of steps, thereby shaking the entire organizational planning.

Master Budget Vs Flexible Budget

A master budget format forecasts financial affairs, while a flexible budget is a type of budgeting where changes can be incorporated to live up to the requirements, depending on the availability of finances. Let us have a look at the differences between them briefly:

| Category | Master Budget | Flexible Budget |

|---|---|---|

| Definition | Financial forecast to list down the expenses and income applicable for the upcoming accounting year | Financial adjustments per availability of assets and existing obligations |

| Purpose | Combines sub-budgets into one major format | Compares actual results against the activities carried out to achieve the same. |

| Applicability | Entire organization or entity | Different departments individually |

| Consideration | All costs | Only variable costs |

Recommended Articles

This has been a guide to what is Master Budget. Here we explain its purpose with an example, components, advantages, disadvantages, and vs flexible budget. You can learn more about from the Accounting following articles –

Recommended Articles

Continue with these closely related articles from the same guide.