Part of our Financial Statements guide

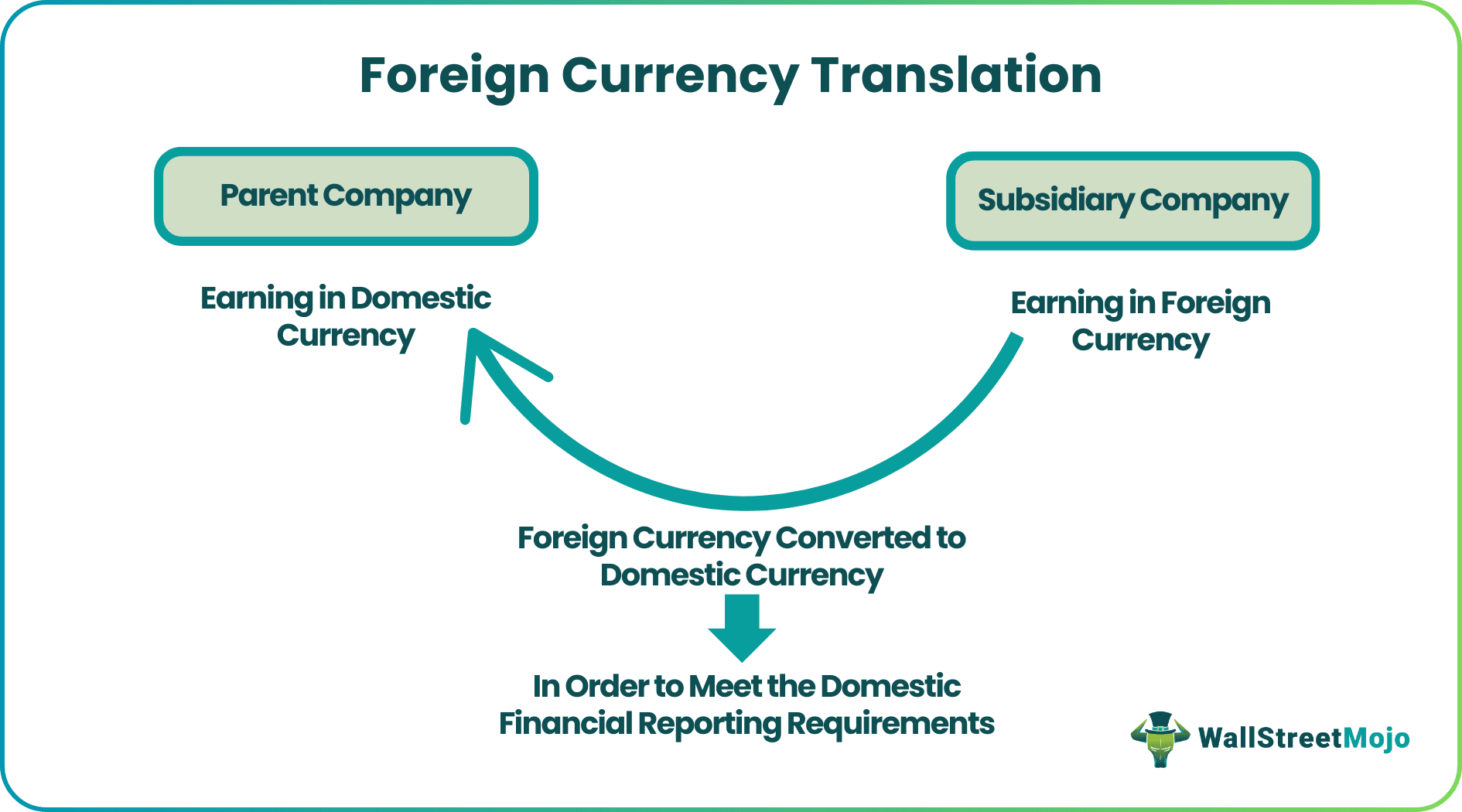

What Is Foreign Currency Translation?

Foreign currency translation refers to the accounting method in which companies having international businesses translate the financials of their international subsidiaries into its domestic or the functional currency with the motive of meeting the financial reporting requirements.

Any gains or losses arising out of such translation are to be recorded in the consolidated financial statements. All the translation adjustments arising from foreign currency translation are recorded in the shareholders’ equity section in the parent company’s consolidated balance sheet.

- Foreign currency translation is the accounting approach in which companies having international businesses translate the international subsidiaries’ financials into the domestic or functional currency to satisfy financial reporting needs. The consolidated financial statements record profits or losses from the translation.

- The current rate, temporal rate, and monetary-nonmonetary translation are the foreign currency translation methods.

- It is dissimilar from the functional currency. Therefore, every translation adjustment from foreign currency must be noted in the shareholders’ Equity section in the parent company’s consolidated balance sheet.

Foreign Currency Translation Explained

The foreign currency translation accounting is the process of converting the foreign currency earning of the subsidiaries in foreign countries to the domestic currency where the parent company is located. In the present world, many companies operate in different areas of the world, having different currencies, but to present a better picture of the company financial statement of the foreign subsidiary should be presented in the same reporting currency as the parent company.

Here, foreign currency translation adjustments comes into the picture, which is used in accounting to re-measure the financial statements of a foreign subsidiary. As per US GAAP, the balance sheet foreign currency translation items are converted at the rate of exchange prevailing on the balance sheet date, and the company’s income statement items are converted at the weighted-average exchange rate for the particular year. All the profits and losses arising from such currency translation will form part of the other comprehensive income.

Process

Let us look at the process of foreign currency translation adjustments.

- To translate the foreign subsidiary’s financial statement into the parent company’s reporting currency, it is to be ensured that the subsidiary’s financial statement is prepared according to GAAP. So, the foreign currency translation process’s first step involves matching the foreign entities’ financial statements to US GAAP.

- After that, the foreign entity’s functional currency is to be determined, i.e., identifying the currency in which financial statements of the foreign currency are reported.

- In the next step, foreign entities’ financial statements will be reassessed in the functional currency which is generally its domestic currency.

- Lastly, all the profits and losses from such currency translation will be recorded in the financial statements.

This process will be followed at each of the balance sheet dates.

Methods

Let us look at the various methods used to translate the foreign currency into the domestic currency.

#1 – Current Rate Translation

According to this method of balance sheet foreign currency translation, all the assets and liabilities of the foreign subsidiary are translated into the parent company’s functional currency at the current rate or the exchange rate prevailing on the company’s balance sheet date. However, the equity section items are translated using the historical foreign currency translation rates, and items of Income statements are translated using the actual exchange rates, i.e., rates prevailing on dates of actual recognition of revenues and expenses.

#2 – Temporal Rate Translation

This method is also known as the historical method, and according to this method, all the balance sheet items are not recognized at a single exchange rate. Rather, both the current and historical foreign currency translation rates are considered based on how the same are carried on the entity’s books.

#3 – Monetary-Nonmonetary Translation

This method distinguishes between the monetary and non-monetary assets and the company’s liabilities. The monetary accounts are translated at the current exchange rate because they are readily convertible into cash and values, fluctuating over time. All the non-monetary statements are translated at historical rates.

Example

Let us assume ABC Ltd is into manufacturing and selling medicines and other medical-related products. It has subsidiaries and branches in many countries. Thus, while reporting its financial statements, it has to consolidate the earning of all the branches and subsidiaries of all the countries for reporting.

However, to do so, it has to convert the financial statements into the country’s currency, where it has its main operation. This process involves a lot of hindrances concerning currency fluctuations, economic conditions of the different countries, consumption of time, etc. This is an ideal situation for foreign currency translation.

Adjustment

The company’s cumulative translation adjustment (CTA) should include all the translation adjustments arising from foreign currency translation. This CTA is shown under the translated balance sheet’s comprehensive income section (part of shareholders’ equity), which compiles all the gains or losses arising from exchange rate fluctuations.

However, it is important to remember certain points while making the adjustments. They are as follows:

- In case the functional currency of the company is a foreign currency, then it is necessary to translate the financial statement into the reporting currency.

- Any unrealized adjustment will not be a part of the income statement. They will be shown separately as a part of the equity in the balance sheet.

- During the liquidation of the company or if the entity plans to sell any of its investment to a foreign entity, the translation adjustment value that is shown as a part of the equity section would have to be removed from there and will be taken as an item in the income statement.

Advantages

- In case of the multiple operations of a company in different countries, the company will be using different currencies for its business operations. Still, from an accounting point of view, financial statements should be presented in a single currency, and for this, foreign currency translation is required.

- This foreign currency translation accounting process analyzes financial statements better if more than a single currency is used, making the analysis difficult. In addition, the process becomes very complicated because more than one currency has to be converted into a functional currency.

Disadvantages

- If there is a major change in the exchange rate, then considering them in income statements may cause significant fluctuations in the current year’s earnings. This is because the exchange rates influence the value of any currency to a large extent affecting the revenue and profit calculation after conversion of the currency.

- It ignores the changes in the exchange rates, and translation gains and losses are recognized in the income statement as soon as it occurs. However, the exchange rates are an important consideration, because it affects the currency value to a great extent.

Foreign Currency Translation Vs Foreign Currency Transaction

- Foreign Currency transaction refers to the operations conducted by the business entity in a currency that is different from its functional currency. In contrast, the foreign currency translation refers to converting the foreign currency transaction into the functional currency as the same is done in the currency other than its functional currency.

- The risks arising in both cases are different. For translation, the risk involved depends on the exchange rate’s influence on converting financial statements from one currency to another. In contrast, for the transaction, the risk involved depends on the exchange rate influence on the time lag between the beginning of the contact to order fulfilment and payment.

Frequently Asked Questions (FAQs)

What is a foreign currency translation reserve?

The foreign currency translation reserve means the accumulated gain or loss resulting from the translation of financial statements denominated in a foreign currency into the company’s reporting currency.

Can the foreign currency translation reserve be negative?

Yes, this translation reserve can be negative. However, it is vital to note that an unfavorable foreign currency translation reserve does not indicate an issue with the company’s financial position. Instead, it reflects the impact of foreign exchange fluctuations on a company’s financial statements.

Where does foreign currency translation go in cash flow?

If a reporting entity possesses cash and cash equivalents in a currency other than the reporting currency, then the resulting transaction gains, losses, and translation adjustments are not considered cash flows but must be recorded in the impact of foreign currency exchange rates on cash and cash equivalents.

Recommended Articles

This has been a guide to what is Foreign Currency Translation. We explain the adjustments, methods, example, differences with transaction & process. You can learn more about it from the following articles –