What is Forward Premium?

Forward Premium is when the future exchange rate is predicted to be more than the spot exchange rate. So if the notation of the Exchange Rate is given like Domestic/Foreign and there is a forward premium, then it means that Domestic currency will depreciate.

- A forward premium occurs when the expected future exchange rate is higher than the current spot exchange rate. In this case, if the notation of the exchange rate is domestic/foreign, the domestic currency is predicted to depreciate in the future.

- The forward premium serves as an indicator of currency depreciation.

- It also provides insights into the direction in which a specific currency is heading. Therefore, monitoring whether currencies are trading at a premium or discount is essential for investors and businesses engaged in foreign exchange transactions.

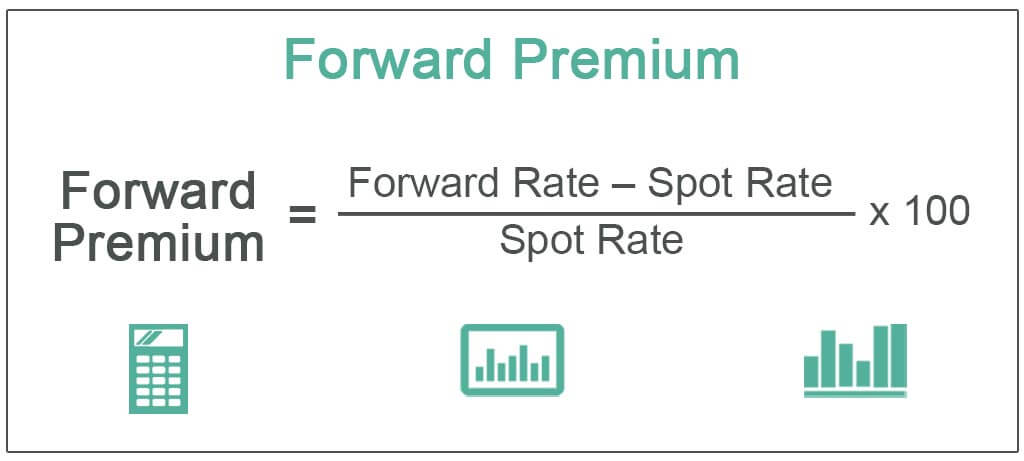

Forward Premium Formula

Formula = (The Future Exchange Rate – The Spot Exchange Rate) / The Spot Exchange Rate * 360 / No. of Days in the Period

How to Calculate Forward Premium?

Step 1: Here we need a forward exchange rate.

Step 2: For the calculation of forward exchange rate we need:

- The Spot Exchange Rate

- Interest Rate prevailing in the Foreign Country

- Interest Rate prevailing in the Domestic Country

Step 3: The formula for Forward Exchange rate-

Forward Exchange Rate = Spot Exchange Rate * (1 + Interest Rate in Domestic Market) / (1 + Interest Rate in Foreign Market)

Step 4: For calculation of the forward premium we need:

- Spot Exchange Rate

- Forward Exchange Rate

Step 5: Apply the formula

Premium = (Forward Rate * Spot Rate) / Spot Rate * 360/Period

Examples

Example #1

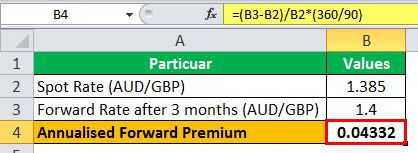

John is a trader, and he lives in Australia. He has sold some goods in London and expects to receive GBP 1000 after three months. John wants to estimate how much more AUD he is expecting to receive, as he is receiving after three months instead of now.

- Spot Rate (AUD/GBP) = 1.385

- Forward Rate after 3 months (AUD/GBP) = 1.40

Annualised Premium = (Forward Rate – Spot Rate) / Spot Rate * (360/90)

The FP is 0.04332

- So, as John is receiving the payment of GBP 1,000 after three months, he is getting more AUD as the AUD is depreciating in 3 months. The total gain, if annualized, is coming out to be 0.04332%.

- So if John had received the payment now, he would have got AUD 1385, but he is receiving the payment after three months. So the AUD will depreciate, and he will receive a payment of AUD 1400. So he is receiving AUD 15 more.

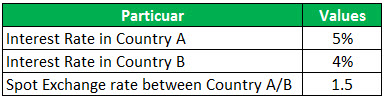

Example #2

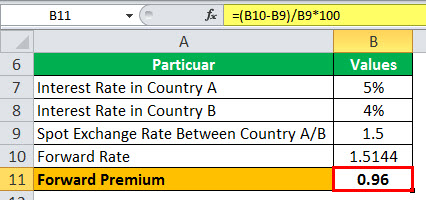

Country A is providing more interest rate than country B. Then why isn’t everyone borrowing from Country B and investing in country A? Information is given below:

Solution:

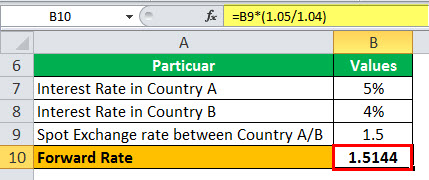

This arbitrage is impossible because there will be a forward premium whenever the Interest Rate is more than others. Say a particular person did this transaction. He borrowed 100 units of currency from country B and invested that in Country A.

So he will get 1.5 * 100 = 150 units of currency in country A.

As we know that at the end of the period the exchange rate will be

Forward Rate = Spot Rate (A/B) * (1 + Interest Rate in Country A) / (1 + Interest Rate in country B)

- So the Exchange Rate after the period will be 1.5144. So now, after the period, the person will receive

- 150 units * 1.05 = 157.5 units of currency A. He will have to convert that in currency B with the new exchange rate of 1.5144

- So he will receive currency B of 157.5 / 1.5144 = 104 units of currency B

- He will have to repay the 4% charged for borrowing 100 units of currency B. So 4 Units of currency B returned as Interest, and 100 units of currency B returned as principal. So the net is zero

Forward Premium = (Forward Rate – Spot Rate) / Spot Rate * 100

- = (1.5144 – 1.50) / 1.50 * 100

- = 0.96

Due to this, the arbitrage was not possible.

Conclusion

Forward Premium is a situation when the future exchange rate is more than the spot rate. So it is an indication of currency depreciation. It determines where the currency of a particular currency is heading. So it is very important to check if currencies are trading at a premium or discount.

Frequently Asked Questions (FAQs)

1. What is forward premium vs. forward discount?

Forward premium refers to the situation when the forward exchange rate for a currency is higher than its spot exchange rate. Conversely, a forward discount occurs when the forward exchange rate is lower than the spot exchange rate. These terms are used in the context of foreign exchange markets to describe the pricing difference between future currency contracts and the current spot rate.

2. What causes forward premium?

Forward premium is caused by various factors, such as differences in interest rates between two countries, market expectations, and supply and demand for foreign currency in the forward market. If interest rates are higher in one country compared to another, investors seeking higher returns will create a demand for the currency, leading to a forward premium.

3. What is the difference between forward premium and spot rate?

The difference between forward premium and spot rate lies in the timing of the currency exchange. The spot rate represents the current exchange rate for immediate currency conversion, while the forward premium represents the cost or benefit of agreeing to exchange currencies at a future date. The forward premium reflects the market’s expectations of currency movements and helps investors manage currency risks in international trade and investment.

Recommended Articles

This has been a guide to what is Forward Premium & its definition. Here we discuss the formula to calculate the Premium along with examples. You can learn more about from the following articles –