Introduction

The “Annual Income” field is confusing when filling out a credit card application. Many people aren’t sure how to write this. Sometimes stay-at-home parents, freelancers that receive varying incomes each month or partners sharing all family funds do not know whether they should only be claiming their own income or whether they can claim all of the family funds.

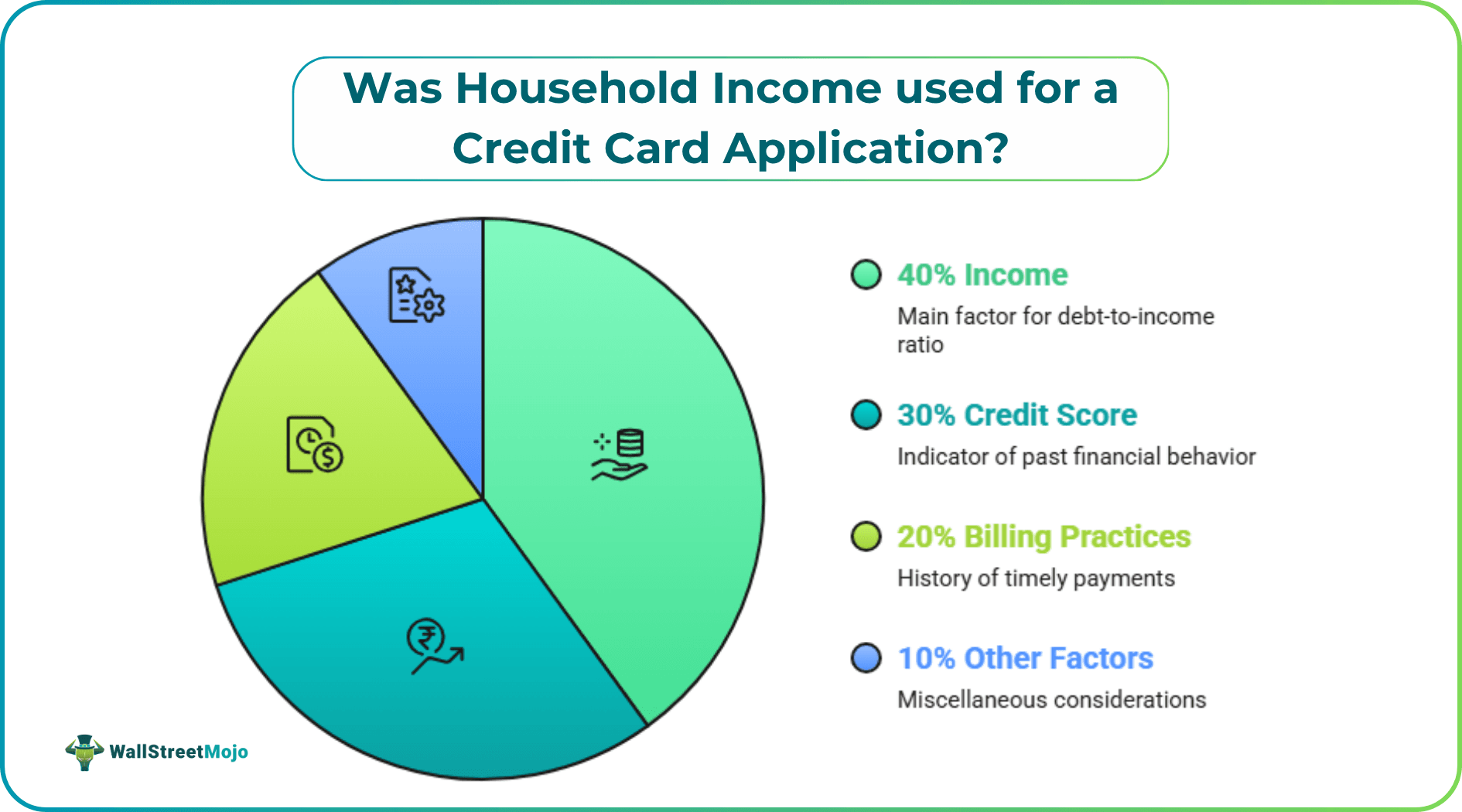

The credit card companies take a look at your credit score and past billing practices to determine whether you are a good spender or not. But, the income you say on your application is the main thing they use to work out your debt compared to what you earn. This number is also used in determining a starting credit limit. If you know the rules for reporting income in your home, you can have a better chance of getting approved. You will also be able to be certain that your application remains legal.

What is Considered Income on a Credit Card Application?

Regular work paychecks are not the only type of income that lenders will recognize. When making checks on your loan, or when you are inputting your figures into a title loan calculator, they will examine any regular or stable cash that streams in. All funds received can be applied toward bills on a monthly basis.

This can consist of: Biased wages, sales wages, and additional wages for good work

- Income from self-employment, self-employment on own account or gig economy

- Income from the regular renting out of property or real estate.

- Funds to be paid out under a retirement plan, pension or investment plan.

- Official spousal support, alimony or payments from a trust fund.

- Frequent government support, distribution of public benefits

Who is Legally Entitled to Household Income?

Under a set of consumer protection rules, the ability to count income from other household members varies. In some states, changes in the laws of lending permit someone age 21 or older to add shared household income to an individual credit card application as long as they have a “reasonable expectation of access” to the income.

#1 – Permissible Scenarios

Married or Domestic Partners: If earnings are kept in joint bank accounts, used to pay for shared living expenses, food costs, and housing.

Stay at home spouses: those who do not earn a salary. However, they have a legal right to have the money brought to the family and home by their working partner.

Adult Dependants: Family members of different ages who are co-residing in the same household. They receive a regular, written allowance or direct money assistance from the primary breadwinners of the family.

#2 – Non-Allowed Scenarios

If your finances are kept totally separate, you can’t add in the income of a roommate, flatmate or family member. Even with an above-ground cohabiting relationship, renting and utility costs being split evenly between you (through a peer-to-peer payment app), you don’t have direct, legal access to their underlying income pool. If you include your income on your application it would be considered to be misrepresenting your financial situation.

Personal Income vs. Household Income

| Key Feature | Stating Personal Income Only | Stating Combined Household Income |

|---|---|---|

| Primary Definition | Earnings generated exclusively by the individual applying for the card | Combined accessible earnings of family members |

| Legal Constraint | Verified via individual W-2 forms, payslips, or personal tax filings | Requires the applicant to be 21+ with a reasonable expectation of access to the funds |

| Underwriting Impact | Limits approval parameters strictly to individual earning capacity | Strengthens application depth for individuals with modest personal income |

| Credit Line Impact | Typically results in conservative or standard credit limits | Often commands higher starting limits due to lower overall risk perception |

| Verification Requirements | Proven via basic personal documentation. | Complex; requires proof of joint financial access if an audit is triggered |

Lenders assess your total borrowing power in the following ways:

Income numbers are not in isolation. The amount that you earn is the basis for calculating your Debt-to-Income (DTI) ratio. The ratio compares what you pay each month to your pre-tax income. If you have a high debt-to-income ratio, for example, you have a large mortgage, car loan or student loan, paying more in your household could still result in your loan application being denied by the underwriter.

When considering other credit options, be sure to review the impact that new debts may have on existing home debts. Use a tool such as a title loan calculator to be able to see plainly the way your loan, which uses your things as backup, will affect the money you have each month. If you enter information in the title loan calculator, you will be able to see how much more money you will have in your budget after you pay off what you owe in your loan each month. Thereby, you can guarantee that any new lines of credit don’t strain your resources at home.

Examples

Here are practical applications and real-world scenarios to illustrate various concepts

Example #1

Sarah works as a freelance graphic designer and makes $35,000 a year. She is married to David. He works as a data expert and gets $80,000 each year. All of the money they save goes into one checking account. As a result, they rely on this for their home loan, electricity bills, and the essentials.

If Sarah wants to apply for her own premium rewards credit card, she can simply put in the amount of $115,000 for her yearly income. This is because her take home is $35,000 and her family contributes $80,000. She is an adult (more than 21) and has all the required documents to pay what she’s due, from the shared family money that she has. The card company can be certain when they agree to her card. They compare her income and her family and think that if they have that amount, it is sufficient.

Example #2

Larger credit card companies, such as American Express, Discover and Chase, utilize new computer systems. These systems verify the amount you enter as your annual income for a card with the average income of people in your area. They might request documentation of income when the economy is weak, or if there are some typical risk checks. The group on the card will be interested in items such as your tax returns or bank statements to ensure that you have correct numbers.

A company will ask for more proof when a person writes their income on the application as $140,000, but only has tax papers for $15,000. A joint bank statement will be required to see that there is money in the home that both parties are contributing. The company will consider the application as fraud if it can’t get them. This will immediately lead to rejection of the application. The bank will also shut down any accounts the person has with them. The name of the person will also be added to a list so that they are not able to open new accounts with the bank.

Know the dangers of giving false answers to questions about earnings:

Using an eligible household income is a definite benefit (in fact, higher approval odds and higher initial credit limits), but there must be full transparency. Guessing or padding numbers to circumvent credit filters can have serious financial consequences:

Routine Review: If it is discovered that there are inflated numbers in the reports, the financial institution will cancel your current credit cards without telling you.

Income Credit Score Implication: Income is not included on credit reports. However, when a company closes your credit card, it decreases the amount of money available for you to use on your credit card. This can also reduce the time that you have had various cards open. Both can have a negative impact on your credit score.

Legal Jeopardy: If you falsely give an income on a credit form, this is illegal. This is considered as a lie to banks.

Conclusion

You can use money from your household on a credit card application. All you have to do is have the funds available and adhere to the age requirements if you have to pay what you owe.

Read the rules and words the card issuer provides you before you submit your application. Make sure your numbers are correct, clear, and easy to verify. This will help you establish a decent credit history and will also ensure following the preferences of most lenders.