What is Hypothecation?

Hypothecation is a process where a lender receives an asset which is offered to him/her as a collateral security and it is largely done in the case of assets that are movable in nature for the purpose of establishing the charge against collateral security for a particular loan.

Key Takeaways

- Hypothecation is a financial arrangement where an asset, such as securities or property, is pledged as collateral to secure a loan or credit facility.

- The borrower retains ownership and possession of the hypothecated asset while granting a security interest to the lender. This allows the lender to seize and sell the asset to recover their funds if the borrower defaults.

- Hypothecation is commonly used in margin trading, where investors borrow funds from a broker to buy securities. The securities purchased with the borrowed funds serve as collateral for the loan.

Explanation

It is almost similar to the mortgage, but there’s a thin line between Mortgage and Hypothecation. In hypothecation, the assets are not immediately transferred to the lender. It does remain in the interest of the borrower. Now, if the borrower is unable to pay the money, then the lender would take possession of it. And then maybe the lender would sell it off to get back the money. There is another difference between the two. In hypothecation, the property that is at stake isn’t immovable property, but movable property like car, vehicle, accounts receivable, stocks, etc.

Also, in this, the amount of loan is also much lower than the home loans. So, the terms and conditions are not as stringent as in the mortgages.

Example

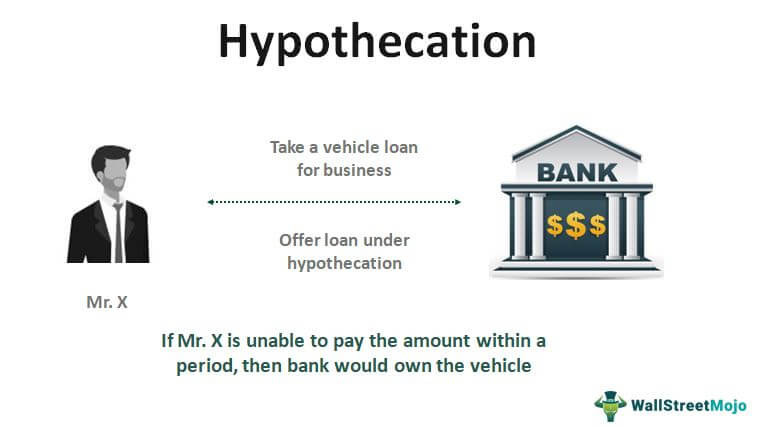

Let’s take a hypothecation example to illustrate the concept. Let’s say that you have decided to take a vehicle loan for your business. This would be used for your business. So, you went ahead and approached a bank.

The bank said that they would offer you a loan, but you need to take the loan under hypothecation. The bank further explained that the vehicle that you want to take would be used by and owned by you only. The bank will help you and will assist in the loan. But the vehicle that you own would be hypothecated, and if you aren’t able to pay the amount due to the bank within a certain period of time, the vehicle would be possessed by the bank.

You agreed to the proposal of the bank, and the bank has offered you a loan.

What is the Hypothecation Agreement?

The hypothecation agreement between the borrower and the lender isn’t done in a verbal agreement. Rather it is done through a document called hypothecation deed.

Here is the list of things that are included in the hypothecation agreement –

- Definitions

- Insurance to ensure that the asset is in great condition.

- The lender’s rights to check out the asset before giving her/his nod.

- The rights, conditions, and terms should be adhered to by both parties.

- The security

- Insurance proceeds.

- Realizations from sales.

- The liability that lies in each party.

- Jurisdiction etc.

This deed is so very important since, on the basis of this deed, the whole agreement is done and adhered to. And two parties are equally responsible for abiding by the terms and conditions mentioned in the hypothecation agreement.

Benefits of Hypothecation

In this, the borrower has many advantages. Let’s have a look at them one by one –

- Ownership: This is a much better option for an individual who has just been starting out in business or career. Of course, there are terms and conditions that need to be followed, but one of the most important advantages is ownership. As a borrower, you can keep the ownership of your movable property, and at the same time, you will get assistance from the bank for the loan. The only condition is you need to pay the due amount on time.

- Lower interest rate: Since there is an option of possessing the movable property if the money isn’t paid on time, the bank/financier charges less interest rate. Two reasons are responsible for charging lower rates. Firstly, the option of possessing the vehicle offers the lender a sense of security that the money would be paid back. Secondly, it is not an unsecured loan as there would be the signed hypothecation agreement between two parties.

- Small loans: Unlike a mortgage, this is done for a small number of loans. As a result, it’s easy to use and easy to pay off. As a business owner, it’s a great opportunity, and often this is used more than mortgage loans.

Frequently Asked Questions (FAQs)

Can I use hypothecated assets for other purposes while they are pledged?

In most cases, while an asset is hypothecated, the borrower cannot use or dispose of it without the lender’s permission. The lender maintains control over the asset until the loan is fully repaid.

What happens if I default on a hypothecated loan?

If you default on a hypothecated loan, the lender can take possession of the pledged asset and sell it to recover their funds. The proceeds from the sale are used to repay the outstanding loan balance, and any remaining amount is returned to the borrower, if applicable.

Are there any alternatives to hypothecation?

Yes, alternatives to hypothecation include unsecured loans, where no collateral is required, or other forms of secured loans that use different types of assets as collateral. The availability of alternatives depends on the borrower’s creditworthiness and the lender’s policies.

Recommended Articles

This has been a guide to What is Hypothecation, along with practical examples. Here we also discuss the Hypothecation agreement and its benefits. You may also have a look at the following fixed income articles –