Introduction

Payment gateway pricing is a trending topic these days, so how to choose a payment gateway? Well, you should stop looking at the 1.8% vs 2% platform fee difference. Here is the mathematical formula for the Total Cost of Ownership (TCO) of your payment stack.

If you are evaluating payment gateways in 2026, you likely have a spreadsheet column labelled platform fee. You are probably sorting that column from lowest to highest, looking for the “cheapest” option.

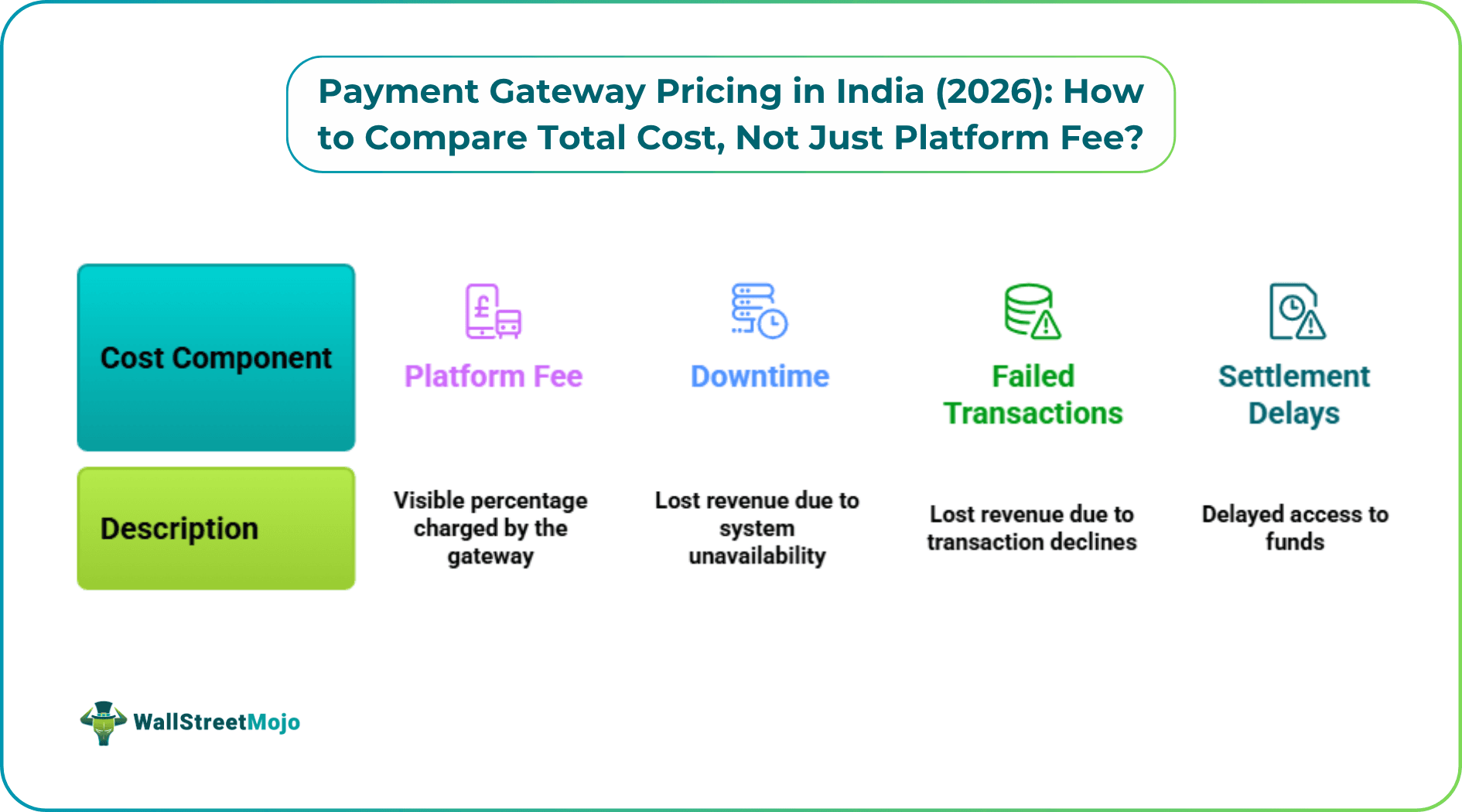

In the Indian payment ecosystem, the headline fee (often 1.8% to 2%) is the visible tip of the iceberg. The real costs—the ones that bleed your P&L; are hidden below the surface in the form of downtime, failed transactions, and settlement delays.

This guide provides a financial framework for calculating the Total Cost of Ownership (TCO) of a payment gateway, so you can make a decision based on profit, not just price.

TL;DR: The 30-Second Summary

- Stop Obsessing Over TDR/Platform: In 2026, the difference between 1.8% and 2% fees is negligible. The real cost that bleeds your business is Transaction Failure.

- Use the TCO Formula: Calculate your true cost using: Total Cost = Transaction Fees + Fixed Costs (AMC) + Revenue Lost to Failure.

- Beware of “Cheap” Traps: Budget gateways (Scenario A) often lure you with low fees but hit you with Annual Maintenance Charges (AMC) and lower success rates. You save ₹500 on fees but lose ₹5 Lakhs in failed sales.

- Prioritize Net Realised Revenue: It is mathematically more profitable to pay a 2% fee for an 80% success rate than a 1.7% fee for a 70% success rate. Gateway B (The Performer) doesn’t cost money; it makes money.

- The Verdict: Razorpay wins on Total Cost of Ownership. By combining Zero Fixed Costs (No AMC/Setup) with industry-leading success rates, it delivers the highest actual profit to your bank account, making it the most cost-efficient choice for growth-focused businesses.

What Are the 3 Layers of Payment Gateway Pricing?

To understand the true cost of a gateway, you must evaluate three distinct layers of expense.

Layer 1 – The Visible Costs (TDR/Platform Fees & Taxes)

- What it is: The standard percentage fee charged per transaction (e.g., 2%).

- The Trap: Founders obsess over saving 0.1% or 0.2% here.

- The Reality: On a ₹1,000 order, the difference between 1.8% and 2.0% is ₹2. While this adds up at scale, it is negligible compared to the cost of losing the customer entirely.

Layer 2 – The Fixed Costs (AMC & Setup)

- What it is: Annual Maintenance Charges (AMC), setup fees, and integration audit fees.

- The Trap: Many “budget” gateways lower their TDR to 1.6% or 1.8% but slap on a ₹10,000–₹20,000 annual fee.

- The Reality: For an early-stage startup or a seasonal business, these fixed fees dramatically increase your effective cost per transaction. A gateway with Zero AMC and a slightly higher TDR is often cheaper for the first 24 months of operations.

Layer 3 – The Invisible Costs (Success Rates)

- What it is: Revenue lost when a customer tries to pay, but the gateway fails due to poor routing or bank downtime.

- The Trap: This cost never appears on an invoice. It appears as “Cart Abandonment” in your analytics.

- The Reality: This is the single largest cost driver. A 5% drop in Success Rate (SR) is mathematically equivalent to losing 5% of your gross revenue. No amount of TDR savings can recover that loss.

Payment Gateway Total Cost of Ownership (TCO) Formula: How to Calculate the Real Cost?

Stop comparing TDR or Platform fees in isolation. Start comparing the Cost of Failure.

In 2026, the true cost of a payment gateway isn’t just what you pay them per transaction—it is the combination of Fixed Fees (which you pay regardless of sales) and Lost Revenue (what they fail to collect for you).

The Payment Gateway Consideration Formula

Total Cost = (Transaction Fees) + (Annual Maintenance Charges) + (Revenue Lost to Failure)

To see how this plays out in the real world, let’s run a simulation for a growing D2C brand generating ₹25 Lakhs worth of customer intent (checkout attempts) per month.

The Simulation: The Discounter vs. The Performer

Scenario A: The “Cheapest” Option (Payment Gateway A)

- The Pitch: “We offer a low 1.7% TDR to save you money.”

- The Fine Print: They charge a fixed Annual Maintenance Charge (AMC) of ₹4,999.

- The Reality: They rely on standard infrastructure with a 70% success rate.

- Traffic (Potential Sales): ₹25,00,000

- Success Rate: 70%

- Realised Revenue: ₹17,50,000

- Lost Revenue: ₹7,50,000 (Money that vanished due to failures)

- The Fees:

- TDR (1.7% on ₹17.5L): ₹29,750

- AMC (₹4,999 ÷ 12 months): ₹416

- Total Monthly Cost: ₹30,166

Net Revenue Landed: ₹17,50,000 – ₹30,166 = ₹17,19,834

Scenario B: The “ROI-First” Option (Payment Gateway B)

- The Pitch: “We charge a standard 2.0%, but we have Zero Fixed Fees.”

- The Fine Print: Zero AMC, Zero Setup.

- The Reality: Their superior tech stack (Smart Routing) delivers an 80% success rate.

- Traffic (Potential Sales): ₹25,00,000

- Success Rate: 80%

- Realised Revenue: ₹20,00,000

- Lost Revenue: ₹5,00,000 (Significantly lower)

- The Fees:

- TDR (2.0% on ₹20L): ₹40,000

- AMC: ₹0

- Total Monthly Cost: ₹40,000

Net Revenue Landed: ₹20,00,000 – ₹40,000 = ₹19,60,000

The Comparison: Who Actually Cost You More?

At first glance, Payment Gateway B looked “expensive” because of the 2% fee. But look at the bank balance at the end of the month:

| Metric | Scenario A (The Discounter) | Scenario B (The Performer) |

|---|---|---|

| Fixed Cost (AMC) | ₹4,999 / Year | ₹0 |

| Fees Paid (Monthly) | ₹30,166 | ₹40,000 |

| Revenue Lost | ₹7,50,000 | ₹5,00,000 (Lower) |

| Net Money in Bank | ₹17,19,834 | ₹19,60,000 |

The Verdict

- The “Extra” Cost: You paid Payment Gateway B roughly ₹9,800 more in transaction fees.

- The “Extra” Gain: You banked ₹2,40,166 more in revenue.

The ROI is undeniable. By choosing Scenario A to save on TDR, you are paying a “Hidden Tax” of ₹4,999/year in AMC plus losing lakhs in failed sales. Scenario B (The Performer) costs slightly more per transaction but makes you richer by capturing more orders and eliminating fixed liabilities.

Rule of Thumb: Never accept a payment gateway with an AMC just to save 0.2% on TDR. That fixed cost eats into your margins during lean months, while the lower success rate hurts you during peak months.

The “Working Capital” Tax: Settlement Speed

There is a fourth hidden cost: Time.

Most legacy gateways operate on a T+2 or T+3 settlement cycle. This means if you sell ₹50,000 worth of inventory on Friday, you might not see that cash until Wednesday.

Other Top payment gateways (like Razorpay, CCavenue) offer T+1 or even Instant Settlements.

- The Value: Accessing cash 2 days earlier reduces your reliance on working capital loans.

- The Cost: If you have to borrow money to restock inventory because your gateway is holding your funds, that interest is a “payment gateway cost.”

The 2026 Checklist: How to Audit Your Payment Gateway Pricing

Before you sign a contract, ask your Finance and Tech teams to answer these four questions. If the vendor cannot provide clear answers, walk away.

“What is your Net Success Rate on UPI vs Cards?”

Why: Aggregate numbers hide failures. A gateway might be great at UPI but terrible at Credit Cards (where your high-value customers are).

“Do you charge for failed transactions?”

Why: Some unethical providers charge a processing fee even if the transaction fails. Ensure you only pay for success.

“Is there an uptime Guarantee or SLA?”

Why: In 2026, bank downtime is common. You need a gateway that uses Smart Routing to switch between banks automatically when one goes down.

“What is the total cost of integration?”

Why: If a “cheap” gateway takes your developers 3 weeks to integrate because of bad documentation, you just spent ₹2 Lakhs in engineering salaries. A developer-friendly gateway (plug-and-play) saves that cost immediately.

“Custom Pricing for High GMV/Enterprise Pricing”

Why: Always look for a payment gateway that gives custom pricing when you scale up like, CCAvenue or Razorpay.

The Verdict: Which Payment Gateway in India Wins on Total Cost of Ownership?

If we apply the TCO Formula (Transaction Fees + AMC/Fixed Costs + Revenue Lost to Failure) to the market leaders, the difference isn’t just in the percentage fee—it’s in the cost of existence. Modern infrastructure wins because it eliminates fixed liabilities.

#1 – The Winner: Razorpay

- Category: Modern Full-Stack (The Performer)

- Effective TCO: Lowest for growth-focused businesses and High GMV Merchants.

- Why it wins: Razorpay optimizes for Net Realised Revenue while removing fixed liabilities.

- Zero Fixed Costs: Unlike legacy competitors that often charge an annual fee just to keep your account active, Razorpay payment gateway has Zero Setup and Zero AMC. You never start the financial year in debt to your provider.

- Revenue Protection: Smart Routing and conversion-optimized features (like Magic Checkout) capture 5-10% more revenue than older, single-rail infrastructures.

- The Cost: 2% standard for the domestic and custom pricing for greater than 5 lakh monthly volume.

- The Math: The combination of Zero AMC (saving ₹5k–₹20k/year) and superior success rates essentially subsidizes the standard 2% fee, plus custom pricing after 5L GMV. It is the most cost-efficient choice for SaaS, D2C, and Tech-first startups. With a 90%+ success rate on transactions, this can be your golden bet.

#2 – 1st Runner Up: BillDesk

- Category: Legacy Bet

- Effective TCO: Medium to High (depending on volume).

- Why it works: BillDesk is the engine behind India’s utility payments. It is built for massive, predictable volume where UI/UX matters less than raw stability.

- The Cost: 1.75%–2% Standard. For modern digital businesses, the TCO increases due to fixed operational costs. Enterprise contracts with legacy players often include Setup Fees, Integration Audit Fees, or Annual Maintenance Charges, particularly if volume commitments aren’t met. When you add these fixed costs to the “Conversion Friction” of a dated checkout UI, the effective cost per successful transaction rises significantly.

#3 – 2nd Runner Up: CCAvenue

- Category: Traditional Payment Gateway Provider

- Effective TCO: High for small-to-mid volume.

- Why it works: One of the oldest players, CCAvenue offers a vast range of currency support and bank options.

- The Cost: 2.00%, historically, CCAvenue has operated with significant Software Upgradation Charges or AMCs (often ranging from ₹1,200 to ₹3,600+ annually). While they have introduced newer plans to compete, many merchants still face these “taxes on existence.” Paying an annual fee regardless of your transaction volume raises your TCO drastically during lean months, making it a “High Fixed Cost” option compared to modern agile players.

| Payment Gateway | Pricing Structure | Fixed Costs (AMC/Setup) | Revenue Risk (Tech/UX) | Total Cost Rating |

|---|---|---|---|---|

| Razorpay | Standard – 2%, Custom Pricing: > 5L GMV | Zero / Zero | Lowest (Best Tech & UX) | Best (Lowest TCO) |

| BillDesk | 1.75%–2% | Medium (Setup/Integration fees common) | Medium (Legacy UX) | Good for Utilities |

| CCAvenue | Standard – Generally 2.00% | Medium (Software/AMC fees common) | High (Dated UX) | High (Legacy Cost) |

Conclusion

In 2026, choosing a payment gateway is no longer just a pricing decision, it is a revenue decision. The difference between a 1.8% and 2% transaction fee may look important on paper, but in reality, poor success rates, downtime, settlement delays, and hidden fixed costs can cost businesses far more than a slightly higher TDR.

The smartest way to evaluate a payment gateway is through the lens of Total Cost of Ownership (TCO): Transaction Fees + Fixed Costs + Revenue Lost to Failures.

A payment gateway that helps you recover more successful transactions, settles funds faster, and removes fixed liabilities will ultimately leave more money in your bank account, even if its headline pricing appears higher.

For startups, D2C brands, SaaS companies, and high-growth businesses, the goal should not be finding the “cheapest” gateway, but finding the gateway that maximizes Net Realised Revenue. In the long run, better infrastructure, higher success rates, smart routing, and zero hidden costs deliver far greater ROI than saving a few basis points on transaction fees.