Part of our Costing Methods guide

What is a Variable Costing Income Statement?

→ Explore all 32 Income Statement articles

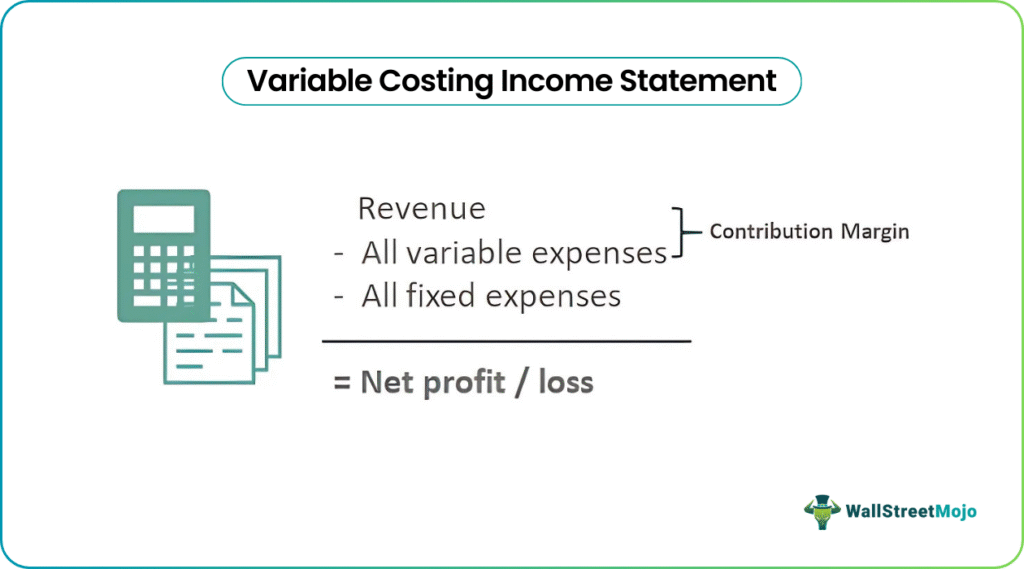

The variable costing income statement is one where all variable expenses are subtracted from revenue, which results in contribution margin. From this, all fixed expenses are subtracted to arrive at the net profit or loss for the period. It is useful to determine the proportion of expenses that varies directly with revenues.

In many businesses, the contribution margin will be substantially higher than the gross margin because such a large amount of its production costs are fixed, and a few of its selling and administrative expenses are variable.

The formula for Net profit or loss is:-

- Contribution Margin =Revenue – Variable Production Expenses – Variable Selling and administrative expenses

- Net profit or Loss = Contribution Margin – Fixed production expenses – Fixed Selling and administrative expenses

Examples of Variable Costing Income Statement

Example #1

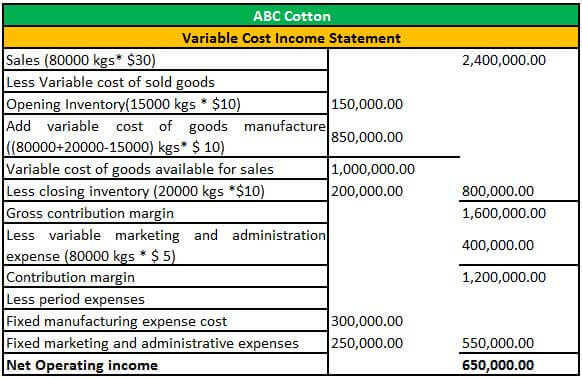

A company named ABC Cotton sells cotton for $30 per Kg. The data for the year 2016 is given below:-

- Sales in Kg- 80,000 kgs

- Finished goods inventory at the beginning of the period- 15,000 kgs

- Finished goods inventory at the closing of the period-20,000 kgs

Manufacturing costs-

- Variable costs- $10 per Kg

- Fixed manufacturing expense cost- $ 3,00,000 per year

Marketing and administrative expenses-

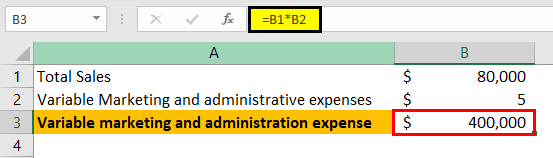

- Variable expenses- $5 per kg of sale

- Fixed expense- $2,50,000 per year

Through the above information, we have prepared a variable cost income statement.

Example #2

Let us understand how this statement is prepared.

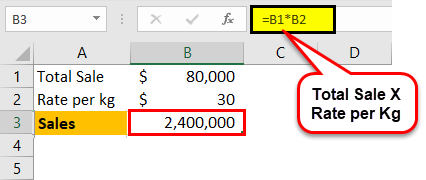

Sales are calculated, which is a total sale in kgs, i.e., 80000 multiplied by per kg cost, i.e., $30.

=Total Sale*Rate per kg

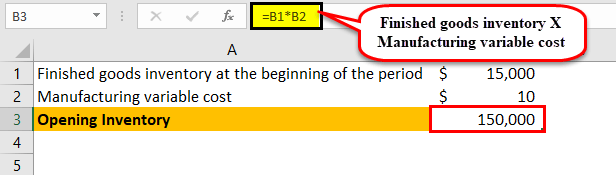

Calculate variable Opening Inventory

Opening Inventory is finished goods inventory at the beginning of the period, i.e., 15000 kgs multiplied by manufacturing variable cost, i.e., $ 10. So,

= finished goods inventory at the beginning of the period* manufacturing variable cost

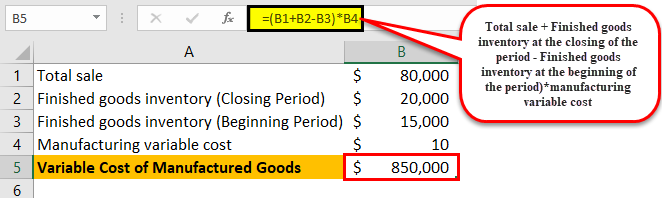

The variable cost of manufactured goods is

=(Total sale + Finished goods inventory at the closing of the period – Finished goods inventory at the beginning of the period)*manufacturing variable cost

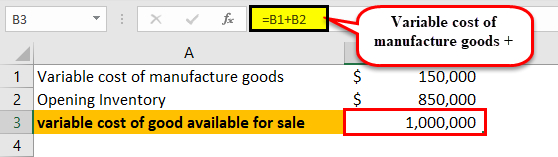

The variable cost of good available for sale

=Variable cost of manufacturing goods + Opening Inventory

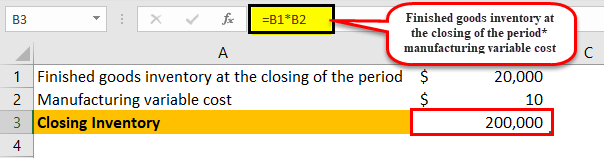

Calculate the closing inventory that is

=Finished goods inventory at the closing of the period* manufacturing variable cost

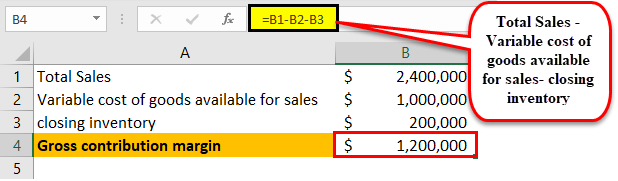

Now, we will get the Gross contribution margin.

Gross contribution margin = Total Sales – Variable cost of goods available for sales – closing inventory

Calculate variable marketing and administration expenses, which is

=Total sale*Variable Marketing and administrative expenses

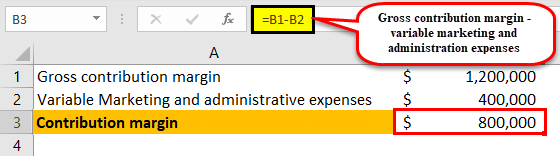

Contribution margin calculated i.e.

=Gross contribution margin – variable marketing and administration expenses

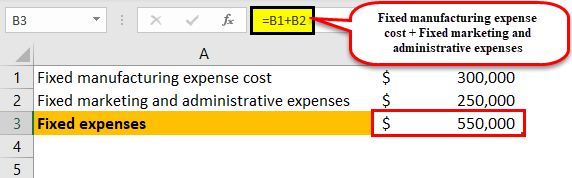

Now, we have to calculate fixed expenses

= Fixed manufacturing expense cost + Fixed marketing and administrative expenses

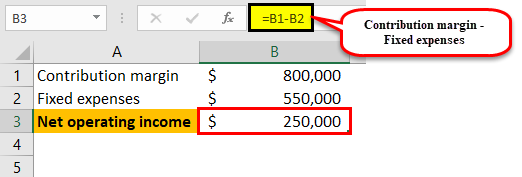

Finally, we will get net operating income

= Contribution margin – Fixed expenses

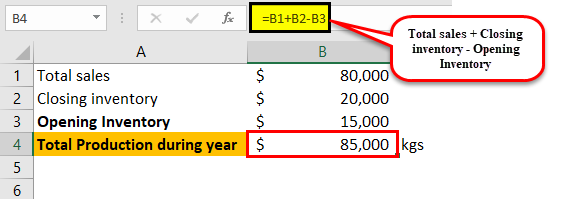

Total Production during year = Total sales + Closing inventory – Opening Inventory

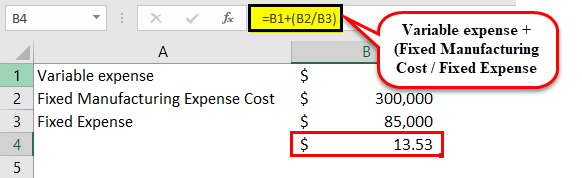

Manufacturing expenses per unit=Variable expense + Fixed Expense

Hence, we found that net operating income with variable costing income principle.

Normal Income vs. Variable Costing Income Statement

- The Normal income statement has a gross margin, whereas variable costing income statements have a contribution margin.

- In variable costing income statements, all variable selling and administrative expenses are a group with variable production costs. It is a part of the contribution margin.

- All fixed production costs aggregate lower in a statement after the contribution margin in variable costing income statements.

The key difference between gross margin and contribution margin is that in gross margin, fixed production costs are included in the cost of goods. Whereas in contribution margin, fixed production costs do not include in the same calculation. This means that variable costing income statements are sorted based on the variability of the underlying cost information rather than by functional areas or expenses categories found in a typical income statement.

Under both statements, the net profit or loss will be the same.

Advantages

- Variable cost provides a better understanding of the effect of fixed costs on the net profit in variable cost income statements.

- Companies get the necessary income for cost volume profit (CVP) analysis. Management cannot extract this data from traditional methods.

- The net operating income figure is close to the flow of cash. It is useful for businesses that face problems in cash flow.

- Other methods change with a change in inventory level, period, etc. Sometimes sales and income move in the opposite direction, but this does not happen in the variable cost method.

Disadvantages

- The variable cost income statement is not per the GAAP standard (Generally accepted accounting principle).

- The tax law of many countries uses other method statements like absorption costing.

- It does not assign a fixed cost to a unit of production. Hence, a production cost cannot be matched with revenue.

Variable cost-income statements help companies in various analyses like cost volume profit, prepare flexible budgets for better variance analysis and help in decision making to accept or reject special orders.

Recommended Articles

This has been a guide to Variable Costing Income Statement. Here we discuss steps to prepare the variable costing income statement along with practical examples and its advantages and disadvantages. You may learn more about Accounting from the following articles –