Table of Contents

What Is X-Value Adjustment (XVA)?

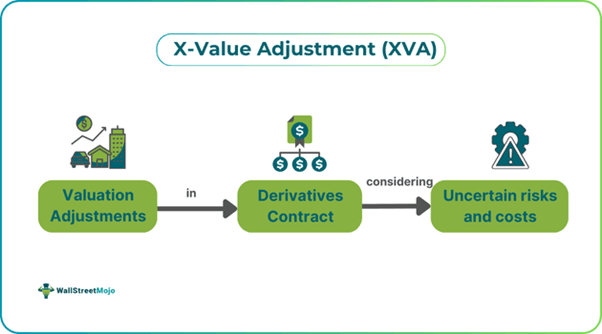

X-Value Adjustment (XVA) refers to adjustments made to derivatives contracts' value, considering uncertain risks and costs that are difficult to measure. This term is relevant when dealing with over-the-counter (OTC) derivatives contracts. It serves to hedge against possible losses when other parties fail to pay the amount owed on the derivative contracts.

XVA was introduced to overcome the shortcomings of the Black-Scholes pricing in determining the uncertain risks associated with a derivative contract. Banks and traders incorporate this model while handling counterparty credit risks and derivatives pricing, respectively.

Key Takeaways

- X-value adjustment (XVA) depicts a group of modifications made to the value of derivatives contracts to account for hard-to-measure expenses and unclear risks.

- It works as a hedge against potential losses in the event that third parties default on their obligations under the derivative contracts.

- The components of X-Value Adjustment include Credit Valuation Adjustment (CVA), Funding Valuation Adjustment (FVA),

- Debt Valuation Adjustment (DVA), Capital Valuation Adjustment (KVA), Margin Valuation Adjustment (MVA), and Collateral Valuation Adjustment (ColVA).

- XVA improves risk management, pricing accuracy, trading decisions, capital valuation, profitability, and market response.

X-Value Adjustment Explained

X-Value Adjustment collectively represents different adjustments applied to the valuation of derivative contracts, accounting for various risk and cost factors like collateral requirements, funding costs, and counterparty risks. These factors ascertain a highly accurate position of risks related to a derivatives contract and market conditions.

It involves sophisticated simulations, mostly using the Monte Carlo method, to incorporate all these factors in detailed risk-adjusted valuation and evaluate the effect of market situations on derivatives pricing. It also helps financial institutions accurately reflect the risks associated with different trades.

Moreover, these modifications of XVAs have impacted profitability by considering risks that were overlooked by traditional valuation techniques. With the exponential growth of this model's complexities, banks have been forced to set up centralized desks. As a result, they have successfully integrated these adjustments into pricing strategies to adhere to regulatory needs and optimize the allocation of capital.

Primarily utilized by large financial institutions and banks, X-Value Adjustment has examined derivatives portfolios precisely and fulfilled regulatory benchmarks. It has also aided in managing risk exposure and pricing decisions. It has also become vital for sell-side and buy-side firms. It has resulted in managing risks efficiently, bargaining better trading terms, and ascertaining competitive pricing concerning OTC derivatives.

In the financial field, its integration into trading has transformed risk management in the derivatives market. Therefore, it has compelled banks to invest more in advanced technologies to manage heightened data processing demands. As a result, the transparency related to different risks associated with derivative valuations has increased.

Components/Types

Let us discuss the components of X-Value Adjustment as listed below:

- Credit Valuation Adjustment (CVA) - It quantifies counterparty default risk, representing the discrepancy between the value of trade, considering counterparty risk and the risk-free value of trade.

- Funding Valuation Adjustment (FVA) - This adjustment takes into account the cost related to financing uncollateralized trades and shows the difference between the risk-free rate and the bank's funding rate.

- Debt Valuation Adjustment (DVA) - It modifies the credit risk related to institutions with trade, affecting their valuation according to the bank's self-creditworthiness.

- Capital Valuation Adjustment (KVA) - It mirrors the cost of holding regulatory capital with respect to trade, taking into account economic and capital costs.

- Margin Valuation Adjustment (MVA) - This reflects the cost related to posting the initial margin throughout the derivative while taking into account anticipated future margin calls.

- Collateral Valuation Adjustment (ColVA) - It resolves differences between posted market value and collateral value, impacting the overall valuation of the derivative.

Examples

Let us use a few examples to understand X-Value Adjustment (XVA):

Example #1

S&P Global shared a case study in 2023 that discussed how a leading investment bank updated its XVA platforms to enhance its comprehension of trading losses and profits. The report specifically centered on counterparty funding costs and credit risk. The selected bank's objective was to incorporate margin valuation and collateral adjustments while ensuring an attractive return on capital after the 2022 regulations.

Hence, using the new system, the bank could deliver full XVAs within a minute, permitting traders to carry out informed decisions quickly. The upgrade allowed access to quick cloud computing resources, revolutionizing the delivery of their technology.

Example #2

Let us assume that a bank in Old York City called Yorky Bank has a risk analyst, Kim, who calculates the bank's XVA. She has to do it for a sophisticated derivative contract between French Hedge fund Laligo Capital and Yorky Bank. Kim observes some credit risks associated with the contract. Hence, she considers credit valuation adjustment (CVA) to assess the credit risk of Laligo capital and funding valuation adjustment (FVA) and to represent the cost incurred by the bank.

While the contract has a notional value of 50 million francs, Kim adjusts it depending on the evaluation of the risk of credit funding. She, in her report, reveals an adjustment of 2 million francs. This revelation affects the entire risk management and valuation strategy of Yorky's bank portfolio and calls for modifications in the strategies to be implemented further.

Importance

Let us take a look at the importance of XVA in trading as follows:

- X-Value Adjustment (XVA) enhances risk management strategies and accurate pricing of derivatives for financial institutions.

- It allows for more improved trading decisions as it integrates various adjustments.

- Basel 3 regulatory pressures have led to the incorporation of capital valuation adjustments, which ensure that banks keep adequate capital reserves to withstand potential losses.

- It has facilitated an accurate reflection of cost pertaining to derivative trading, allowing firms to optimize capital allocation and enhance profitability.

- It has helped institutions to respond quickly to enhance trading strategies and market changes with evolving markets.