Part of our Derivatives Basics guide

What Is Managed Futures Strategy?

Managed futures strategy is a part of an optional futures strategy which are handled on a managed futures account by an external expert who uses futures contract in their overall investments to manage the funds of the owners and hence it reduces various risk of the business entity.

Managed Futures Strategy Managed futures are part of an Alternative investment strategy, especially in the U.S. through which professional portfolio managers make extensive use of Futures contracts as a part of their overall investment strategy. Such strategies aid in mitigating portfolio risks, which are difficult to achieve indirect equity investments.

Key Takeaways

- Managed futures strategies involve professional investment managers trading futures contracts on behalf of investors.

- These strategies aim to generate returns by capitalizing on price movements across various asset, including commodities, currencies, interest rates, and equity indexes.

- Managed futures strategies often employ systematic trading models and rely on technical analysis, quantitative research, and trend-following methodologies.

- These strategies offer potential benefits such as diversification, liquidity, the potential for positive returns in both rising and falling markets, and professional management.

Managed Futures Strategy Explained

A managed futures strategy fundor managed futures fund is a type of alternative investment through which trading in the futures market is managed by another person or entity instead of the fund’s owners. These accounts are not necessarily limited to commodity pools and are operated by Commodity Trading Advisors (CTA’s) or Commodity Pool advisors (CPO’s), which are generally regulated in the U.S. by the Commodity Futures Trading Commission (CFTC) through National Futures Association before they can offer services to the general public. These funds can take either a buy (long) or sell (short) positions in Futures contracts and options in the Commodities (cotton, coffee, cocoa, sugar) Interest rate, Equity (S&P futures, FTSE futures), and Currency markets.

Source: Arrow Funds

Managed futures are one of the oldest hedge fund styles, having been in existence for the past three decades. The CTA’s are required to go through an FBI background check, which is required to be updated every year and to be verified by the NFA.

Also, check out Hedge Fund Strategies

source: Arrow Funds

The strategies and approaches within “managed futures” are extremely varied. The one common unifying characteristic is that these managers trade highly liquid, regulated, exchange-traded instrument s, and foreign exchange markets. This permits the portfolio to be “marked to market” every day.

- Trend following CTA’s develop algorithms to capture and hold longer-term trends in the markets, which may last from several weeks to a year. They make use of proprietary technical or fundamental trading systems or a combination of both.

- Countertrend approaches attempt to capitalize on the dramatic and rapid reversals which take place in such long-term trends.

Being in possession of more information never hurts, and it can help avoid investing in CTA programs that do not fit investment objectives or risk tolerance ability, an important consideration before investing with any money manager. Given the proper due diligence about investment risk, however, managed futures can provide a viable alternative investment vehicle for small investors looking to diversify their portfolios, thereby spreading their risks.

Example

Let us look at an example to understand the concept.

During times of inflationary pressure, investing in managed futures which trade in commodities and foreign currency futures can provide a counterbalance to the losses which may occur in the equity and bond market. If stocks and bonds are underperforming in inflationary scenarios, managed futures might outperform in the same market conditions. Combining managed futures with other asset classes may improve risk-adjusted portfolio returns over time.

Benefits

Let us look at some of the benefits of the concept that we should keep in mind while making investments in such avenues.

One of the benefits of including managed futures in a portfolio is risk reduction through portfolio diversification by means of low or negative correlation between asset groups. As an asset class, managed futures programs are uncorrelated with stocks and bonds.

The benefits of managed futures strategy fund can be summarized as follows:

- Potential for returns in Up and Down markets with the flexibility of taking long and short positions, which allows for-profit in both rising and falling markets.

- No- Correlation to traditional investments like equities and bonds.

- Enhanced diversification of the portfolio.

- Decisions are determined by computer models, which guide in maintaining a consistent and disciplined investment approach by removing emotional hurdles and reliance on manager discretion.

- Allows for the historical study of price data to research, develop, and test strategies so that results in a repeatable process can be quantified and studies to improve consistency.

- Construction of the portfolio using various markets and sectors to increase diversification.

- Investing in a passive manner reduces the impact of certain traditional obstacles of investing in CTA’s. It also reduces the burden of how to find and monitor the best CTA managers

Thus the above were some important points that highlights the positive side or usefulness of the method of investment.

Drawback

Despite these benefits, there are certain drawbacks of managed futures hedge fund strategy. Let us try to analyse them in details.

- Returns may be biased upwards: The returns for indexes of CTA managers tend to be biased upwards due to the voluntary nature of self-reporting of performance. A CTA with a less impressive performance for a length of time is less likely to report unfavorable returns to such databases, resulting in an index that mostly includes impressive performance.

- Lack of natural measuring stick: Other asset classes like Equities or bonds have a natural benchmark for performance reporting. Market capitalization-weighted benchmarks for traditional investments mathematically represent the average return applicable to the investors. Such aggregate performance measures are difficult to apply in the case of managed futures space.

- CTA’s are known to charge very high fees for their services. Generally, the fee structure is similar to that a hedge fund utilizing the 2/20 structure (2% Management Fees and 20% Performance fees on achieving a high water-mark)

- System-based trading is unable to adapt to news or environments which are different from past environments through which the models were initially derived.

- The amount of fees charged is very high, which may not necessarily balance out the effects of any downfalls, which can be caused due to choppy conditions.

While discretionary CTA managers still exist, the majority of managed futures trading advisors comprise strategies that rely on systematic, computerized approaches to generate market trading decisions. Theoretically, systematic trading strategies strive to eliminate any chance of generating alpha. However, with investment decisions, there are certain strengths and weaknesses associated with systematic strategies.

It is necessary to understand and estimate the pros and cons of every strategy or method of investment that are used in the financial market. It is advisable to take the help of professional experts who will not only have the required skill and knowledge, but will also keep track of the latest changes in rules and methods of the process. This will help in taking informed decisions.

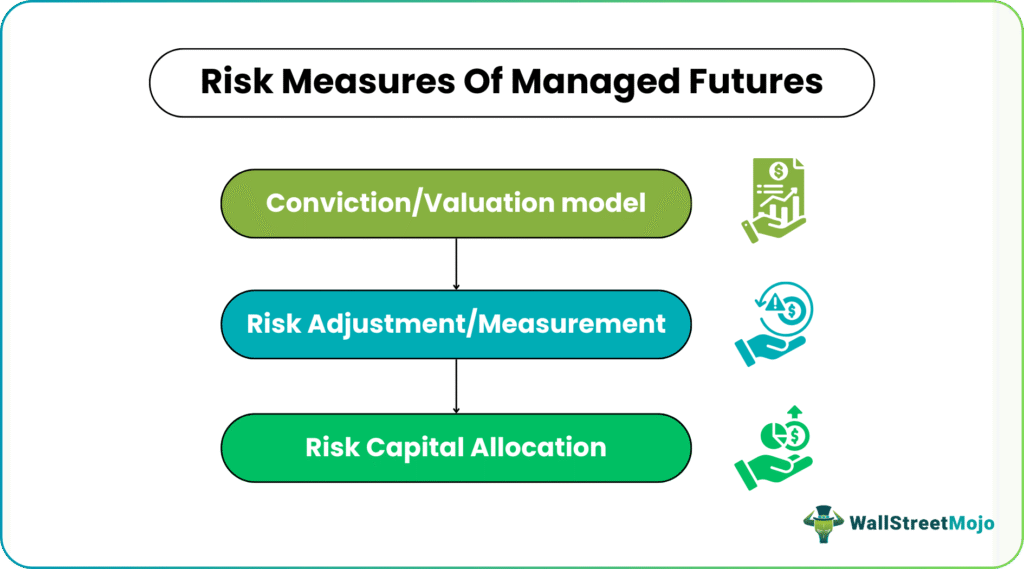

Risk Measures

Risk management is often seen as a key success for CTA strategies. A futures portfolio is built by taking positions/exposures in futures contracts across various markets.

A simple way to determine the position size of managed futures hedge fund strategy is the below equation:

Portfolio size = Portfolio scaling factor * (Market Conviction * Market Risk allocation) / Volatility of the market

Market conviction defines the direction (buy or sell) and the level of confidence of each market. The market risk allocation is the quantum of risk allocated to an individual market or industry. Given these factors, each position in the number of contracts is set by the amount of volatility in each market. For instance, if Salt is less volatile and Oil is highly volatile, the position taken will be smaller, all other aspects remaining equal.

For many CTA’s portfolio constructions can be simplified into a 3 step process which can be displayed with the help of the below diagram:

source: caia.org

If the portfolio construction process is simplified into the above stages, stage one is a Model conviction, while stages two and three indicate risk management.

Risk Management

→ Explore all 147 Risk Management articles

Once stage one is separated from risk management and kept constant, risk management decisions can be isolated for creating risk management based factors. The risk management process is dependent on the below factors:

- The Liquidity factor measures the effect of allocating relatively more risk to highly liquid markets like the money markets. Liquidity is defined by the volume and volatility for each market. In terms of the liquidity factor, the risk allocation across markets will tilt more towards the liquid markets. When this factor indicates a positive return, it means that a portfolio that allocates more risk to more liquid markets outperforms the equal dollar risk portfolio.

- The Correlation Factor measures the effect of incorporating correlation into the risk allocation process. This allocation is determined by ranking the markets based on their “correlation contribution” for each market. When a market is highly correlated with multiple other markets, but the initial markets are not in an offsetting position, less risk shall be allocated to it. The idea is that if one market is falling, the other market should be in a position to compensate for the same. When the correlation factor returns are positive, it means that a portfolio incorporating correlation in risk allocation outperforms an equal dollar risk portfolio.

- The Volatility Factor measures the effect of reacting more slowly to changes in the market volatility through the “volatility of market” mentioned in the above equation. The strategy will generally involve a three month look-back period, which means the volatility will be analyzed in the past say 3-6 months. A positive return for this factor means that over that time frame, the portfolio with the slower volatility adjustment outperforms the baseline.

- The Capacity factor measures the effect of re-allocating risk based on capacity constraints. This factor compares the performance of a portfolio, which trades at $20 billion in the capital, with the baseline strategy trading at $5billion in the capital. The same volatility target, limits, and restrictions are applied to each of the $5bn and $20bn strategies, except a few of these limits are more binding for a larger portfolio. In response to these limits, a larger portfolio will re-allocate risk to other positions for achieving the total risk target. When the capacity factor returns are positive, it is an indication that the portfolio shall outperform the baseline portfolio.

For every individual factor, the impact of each risk management aspect can be measured across the set of included markets (equities, commodities, fixed income, and currency).

The below table indicates the performance statistics for the benchmark strategy and the above risk management factors.

| Management | Mean (%) | Median (%) | Standard Deviation (%) | Sharpe | Skew | Max Drawdown (%) |

|---|---|---|---|---|---|---|

| Baseline | 10.33 | 13.01 | 13.10 | 0.74 | -0.39 | 27.58 |

| Liquidity | 0.23 | 0.18 | 1.11 | 0.19 | 0.12 | 6.88 |

| Correlation | 0.23 | -0.15 | 1.45 | 0.16 | 0.26 | 4.85 |

| Volatility | -0.08 | -0.18 | 0.94 | -0.06 | 0.40 | 6.22 |

| Capacity | -0.94 | -1.01 | 2.85 | -0.30 | 0.06 | 26.38 |

Since 2001, the liquidity and correlation factor returns have been positive on average, while the volatility and capacity factors have been on the negative trend. The Capacity factor has the most negative realized Sharpe ratio during this period indicating re-allocation of risk due to capacity constraints underperforming the baseline strategy by 0.94% per year on average from 2001-2015.

The correlation factor became more positive post-2008 though the element of volatility continues to exist, suggesting that adjusting risk for correlation would have improved portfolio performance post-2008. The liquidity factor was positive prior to 2005 and again post 2011. There seem to be certain time periods where the capacity-constrained portfolio either underperforms or outperforms the targeted baseline strategy (trading at $5billion). This suggests that exposure to capacity constraints can cause performance to deviate from the baseline strategy.

Sharpe Ratio

The Sharpe Ratio is a measure for calculating the risk-adjusted return and has become an industry standard for such calculations. It is calculated using the below formulae:

Sharpe Ratio = (Mean Portfolio Return – Risk Free Rate) / Standard deviation of portfolio return

A drawdown is a period of negative positions, i.e., the percentage change in the NAV between a high peak and subsequent trough. It takes into account the accumulated losses over a period of time, i.e., multi-period risk measures. A drawdown is not necessarily a sign of distress, but tightly connected to the fact that the markets are not always trending, and managed futures programs, in general, are expected to generate positive returns during such periods.

A maximum drawdown is a worst-case scenario a CTA manager has experienced for a specified period of time most commonly, since inception. For correct evaluation, corrections should be made to account for track length, frequency of measurement, and volatility of the asset.

Calmar Ratio

The Calmar ratio was developed as an alternative to the Sharpe ratio, which is known to have its own shares of flaws. This ratio is used to evaluate a return from one period to against the maximum drawdown the program has experienced during the mentioned period.

Calmar Ratio = (Annualised Return t) / (Maximum drawdown t)

A high Calmar ratio indicates that for a given annual return, the manager had attained a low drawdown.

Frequently Asked Questions (FAQs)

What are the advantages of investing in managed futures strategies?

Managed futures strategies provide access to diverse markets and asset classes, offering the potential for uncorrelated returns to traditional investments. They can enhance portfolio diversification, provide liquidity, and offer the expertise of professional managers with specialized knowledge in futures trading.

What are the risks associated with managed futures strategies?

Managed futures strategies involve risks such as market volatility, the potential for losses, and the reliance on the performance of the underlying futures contracts. The use of leverage in futures trading can amplify gains but also magnify losses. Additionally, these strategies are subject to management fees and expenses.

How are managed futures strategies different from traditional investments?

Managed futures strategies differ from traditional investments, focusing on trading futures contracts rather than buying and holding securities. These strategies can benefit from both rising and falling markets and often have a low correlation with other asset classes.

Recommended Articles

This article has been a guide to what is Managed Futures Strategy. We explain it with example, benefits , drawback, risk measures and risk management procedures.