Part of our Derivatives Basics guide

What Is Debit Valuation Adjustment (DVA)?

Debit Valuation Adjustment (DVA) is a financial concept used in derivatives and risk management. It aims to accurately reflect the credit risk associated with a company’s liabilities, particularly when valuing products and other financial instruments.

It provides a more comprehensive and realistic assessment of the value of these liabilities by considering the potential changes in market value resulting from the company’s creditworthiness. It helps companies quantify and manage the credit risk associated with their weaknesses.

Key Takeaways

- Debit Valuation Adjustment represents the adjustment made to the value of a company’s liabilities. This represents the account for the potential credit risk.

- It aims to provide a more accurate valuation of liabilities. Especially in the context of derivatives and other financial instruments, by considering changes in the company’s creditworthiness.

- It estimates credit spreads, probabilities of default, and potential loss given default. It incorporates them into the valuation of liabilities and derivative cash flows.

- It is relevant for risk management, as it allows companies to assess and manage their credit risk. And make informed decisions regarding risk mitigation strategies.

Debit Valuation Adjustment Explained

Debit Valuation Adjustment (DVA) is a concept that originated in the aftermath of the 2008 financial crisis, which highlighted the importance of assessing and managing counterparty credit risk. It emerged as a response to the need for a more accurate valuation of liabilities, especially in derivative transactions.

It emerged as financial institutions recognized the need to incorporate credit risk into valuing derivative positions. During the financial crisis, the collapse of major financial institutions and the subsequent increase in counterparty credit risk exposed the limitations of traditional valuation models that failed to account for credit risk adequately.

The concept gained prominence as regulators and standard accounting bodies sought to address the deficiencies in existing valuation practices. As a result, the International Accounting Standards Board (IASB) and other regulatory bodies introduced guidelines and standards to ensure that companies appropriately accounted for credit risk in their financial statements.

It improves the accuracy of liability valuation by considering the credit risk associated with a company’s debt. This adjustment provides a more realistic reflection of the actual economic value of liabilities, especially in cases where the company’s creditworthiness fluctuates.

It aligns with regulatory guidelines and accounting standards, such as IFRS (International Financial Reporting Standards) and FASB (Financial Accounting Standards Board), ensuring companies adhere to transparent and consistent reporting practices. Compliance with these standards enhances financial reporting transparency, comparability, and accountability.

It facilitates a better assessment of counterparties’ creditworthiness in derivative transactions. Considering a company’s credit risk provides insights into the overall credit exposure, enabling firms to make informed decisions regarding counterparties and their associated risks.

How To Calculate?

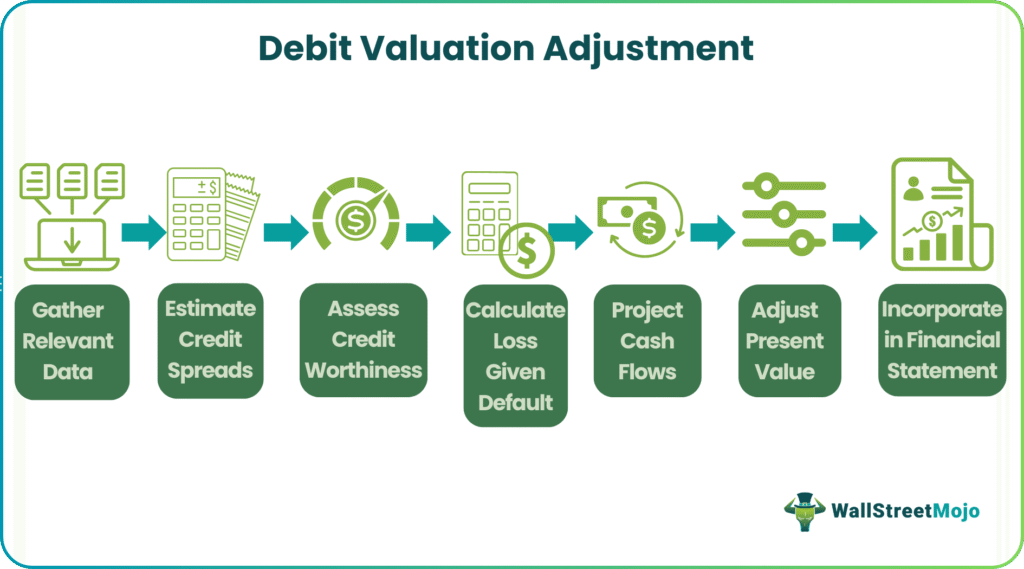

Debit Valuation Adjustment (DVA) calculation involves several steps and considerations. While the specific methodology may vary among financial institutions and accounting frameworks, let us outline a general approach to understanding the same.

- Credit Spreads: The first step is determining the credit spreads for the company’s debt. Credit spreads represent the additional yield investors demand to compensate for the credit risk of holding the company’s debt. These spreads are market data, credit rating agencies, or credit default swaps (CDS).

- Risk-Free Rates: Next, the risk-free rates need to be identified. These rates represent the yield on risk-free government bonds with similar maturity periods. Risk-free rates provide a benchmark against which credit spreads can be compared.

- Probability of Default: The possibility of default is the likelihood that the company will default on its debt obligations within a time frame. It can be estimated using various methodologies, including credit rating agency assessments, market-based approaches, or internal credit risk models.

- Loss Given Default: It refers to the potential loss incurred by creditors in the event of a default. It depends on factors such as the recovery rate on the company’s debt and the legal framework governing creditor recovery.

- Exposure Profiles: The exposure profiles of the company’s derivative positions need to be determined. This includes understanding the cash flows, terms, and contractual obligations associated with these derivatives.

- Monte Carlo Simulation: A Monte Carlo simulation is often used to calculate DVA. This simulation models potential scenarios for credit spreads, risk-free rates, and other relevant factors. The simulation considers the possible changes in the company’s creditworthiness over time.

- Present Value Adjustment: The final step is to calculate the current value adjustment by discounting the cash flows of the derivative positions. This uses simulated credit spreads and risk-free rates.

Examples

Let us understand it better with the help of examples:

Example #1

Suppose a fictional company, ABC Corporation, has issued bonds with a market value of $100 million. However, due to deteriorating market conditions and decreased company creditworthiness, the credit spreads on ABC Corporation’s bonds increased. Correspondingly, the market value of the bonds decreases to $90 million. In this scenario, ABC Corporation would apply an adjustment of $10 million to adjust the value of its liabilities to reflect the increased credit risk associated with its debt.

Example #2

According to the news, Bank of America’s derivatives portfolio experienced a significant impact from Debit Valuation Adjustments (DVAs) in the fourth quarter. The DVAs resulted in a reduction of $193 million from the bank’s revenue, which was 14 times higher than the previous quarter (Q3) and the most significant impact since the second quarter of 2020.

Specifically, the net DVAs for Bank of America’s fixed income, currencies, and commodities division amounted to a negative $186 million. This signifies the adjustments made to derivatives assets and liabilities based on bank creditworthiness changes. In the equities division, the loss from DVAs was $7 million.

These figures highlight the significance of DVAs in the bank’s financial performance, reflecting the potential impact of credit risk and changes in creditworthiness on the valuation of derivative positions.

Credit Valuation Adjustment And Debit Valuation Adjustment

Here’s a comparison between Credit Valuation Adjustment And Debit Valuation Adjustment:

#1 – Definition And Focus

Credit Valuation Adjustment represents the adjustment made to the value of a derivative position to account for the potential credit risk of the counterparty. It measures the possible loss that a company may face if the counterparty fails to honor its contractual obligations.

Debit Valuation Adjustment represents the adjustment made to the value of a company’s liabilities to account for the potential credit risk associated with its debt. It reflects the possible decrease in the market value of a company’s liabilities due to its creditworthiness.

#2 – The Direction Of Adjustment

Credit Valuation Adjustment is added to the value of a derivative position to reflect the potential loss caused by counterparty credit risk. As a result, it increases the fair value of the derivative work.

Debit Valuation Adjustment is subtracted from the value of a company’s liabilities to account for the potential decrease in its value due to its credit risk. As a result, it decreases the fair value of the penalties.

#3 – Calculation

The calculation of Credit Valuation Adjustment involves estimating the potential exposure of the derivative position, the counterparty’s default probability, and the possible loss-given default. It also considers credit spreads, recovery rates, and correlation.

The calculation of Debit Valuation Adjustment involves estimating the credit spreads associated with the company’s debt, the probability of default, and the probable loss given default. In addition, it considers the exposure profiles of the derivative positions and incorporates factors such as risk-free rates and possible changes in creditworthiness.

#4 – Perspective

Credit Valuation Adjustment is primarily relevant from the perspective of the holder of the derivative position, as it measures the potential loss due to counterparty default.

Debit Valuation Adjustment is relevant from the perspective of the company or institution, as it accounts for the potential decrease in the value of its liabilities due to its own credit risk.

#5 – Risk Management

Credit Valuation Adjustment helps companies and institutions manage and hedge counterparty credit risk by incorporating it into derivative positions’ valuation and risk assessment.

Debit Valuation Adjustment helps companies manage their credit risk by adjusting the value of liabilities, allowing for a more accurate assessment of their financial position.

Frequently Asked Questions (FAQs)

1.Is debit valuation adjustment required for financial reporting?

The requirement to include Debit Valuation Adjustment in financial reporting depends on the accounting standards, such as IFRS or FASB. These standards guide the appropriate treatment of financial statements, and compliance may be mandatory for specific companies or institutions.

2.Can debit valuation adjustment be positive?

Yes, Debit Valuation Adjustment can be positive or negative, depending on the circumstances. For example, if a company’s creditworthiness improves, it can be positive, increasing the reported value of liabilities. Conversely, if the company’s creditworthiness deteriorates, it can be damaging, decreasing the declared value of liabilities.

3.How does debit valuation adjustment impact derivative pricing?

It impacts derivative pricing as it affects the valuation of liabilities. When subtracted from the value of liabilities, it decreases their fair value. This can lead to adjustments in the pricing of derivative contracts. In addition, it reflects the credit risk counterparties bear. This is due to the company’s creditworthiness, resulting in potential changes in the terms and pricing of derivatives.

4.Is debit valuation adjustment applicable only to OTC derivatives?

No, it can also apply to other financial instruments or liabilities where credit risk is significant. However, the specific applicability of DVA may vary depending on the particular financial instrument, accounting standards, and regulatory requirements.

Recommended Articles

This has been a guide to what is Debit Valuation Adjustment. We compare it with credit valuation adjustment, explain its examples, and how to calculate it. You can learn more about it from the following articles –