Part of our Derivatives Basics guide

Introduction

Options occupy an unusual position in the high-net-worth advisory conversation. In most retail and institutional contexts, they’re understood as speculation instruments: tools for expressing a directional view on a stock or index, often with leverage. That framing is accurate for one segment of the market. It is almost entirely wrong for the conversation that matters most to HNW investors with concentrated equity positions.

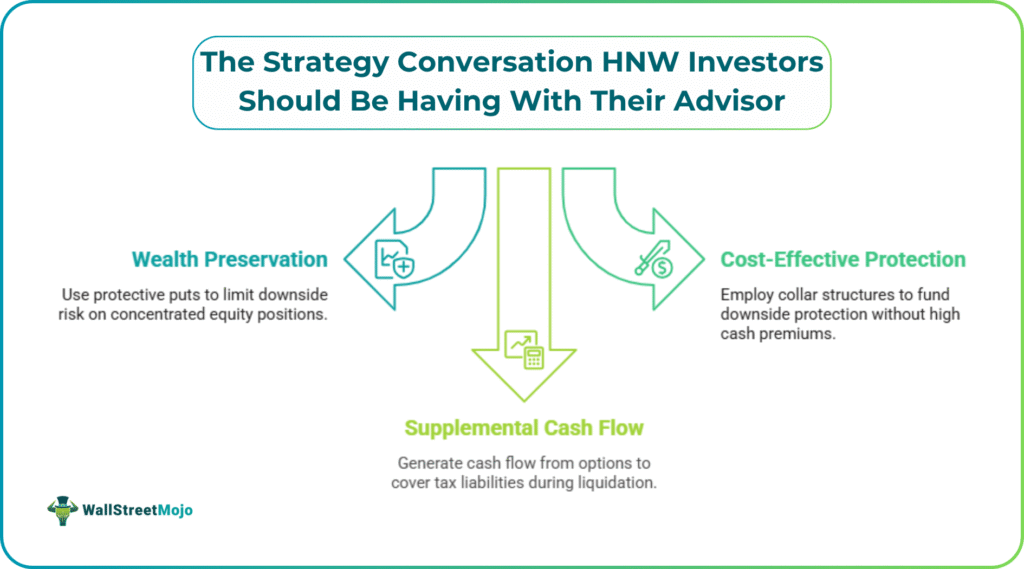

For a Bay Area executive holding $4M of company stock with a low cost basis, a protective put is not a speculative bet on the stock going down. It’s a wealth preservation mechanism that limits the downside of a position they can’t or won’t sell. For a tech founder with RSUs that have vested across multiple years, a collar structure is not an exotic trading strategy. It’s a way to fund downside protection without requiring the cash premium that a standalone put would cost. For a family managing a concentrated position through a multi-year tax-aware liquidation, options can generate supplemental cash flow to fund the resulting tax liability while the position is being systematically reduced.

These are planning instruments. Treating them as trading instruments – or, more commonly, not considering them at all – leaves a significant set of tools unused.

Options as a Planning Instrument vs. Options as Speculation

The distinction is not semantic. It determines who needs to be in the conversation, what considerations govern the decision, and how the strategy integrates with the client’s overall financial picture.

An options strategy used for speculation is evaluated primarily on its risk/reward profile relative to the underlying asset. The relevant expertise is in the trading or investment domain. The decision is relatively self-contained.

An options strategy used as a planning instrument is evaluated on its interaction with the tax situation, the estate plan, the client’s liquidity needs, and the long-term portfolio objectives. The relevant expertise spans investment management, tax planning, and — in some cases — estate planning. The decision is not self-contained. It requires the advisory team to have visibility across all of these dimensions simultaneously.

This is why most clients with concentrated positions who would benefit from options strategies don’t use them: their investment advisor doesn’t offer them, their CPA doesn’t raise them, and the coordination required to use them intelligently doesn’t exist in a siloed advisory structure.

Firms such as Lido Advisors in San Francisco, where concentrated tech equity positions are among the most common planning challenges, provide a useful example of how options can fit within a broader wealth plan. Their approach highlights the distinction that matters most: options used as planning instruments require a fundamentally different kind of advisory relationship than options used as trading tools.

Three Scenarios Where Options Change the Wealth Outcome

For high-net-worth investors with concentrated equity – particularly Bay Area executives and founders managing RSU accumulations or founding stakes – three planning scenarios occur with regularity where options materially affect the outcome.

The first is downside protection on a concentrated tech equity position. An executive or founder holding a large position in a single stock – whether from RSUs, options exercises, or a founding stake – faces asymmetric risk: the position represents a disproportionate share of net worth, and a significant decline would have an outsized impact. A protective put strategy provides a defined floor on that exposure for a defined period of time, funded by a premium that is weighed against the value of the certainty it provides. The decision requires knowing the cost basis of the position, the tax implications of purchase, and how the hedge interacts with the overall portfolio allocation – not just the put’s intrinsic value.

The second is a collar strategy for an executive who cannot or will not sell shares. A collar – buying a protective put while simultaneously selling a covered call at a higher strike – can be structured to be approximately costless by using the call premium to offset the put premium. The tradeoff is that upside beyond the call strike is forfeited. For an executive whose primary concern is catastrophic downside, not maximum upside, this tradeoff is often acceptable. The tax implications of the collar structure, its interaction with any 10b5-1 plan, and the estate planning context for the underlying shares all need to be part of the decision.

The third scenario is systematic tax-aware liquidation. For a family that has decided to reduce a concentrated position over a multi-year period, options can be used to generate cash flow that funds the tax liability associated with each tranche of sales, creating a self-financing liquidation program. This is a sophisticated strategy that requires precise coordination between the investment advisor, the tax advisor, and the client’s overall liquidity plan.

Why This Requires More Than a Trading Desk

The planning value of options strategies for HNW investors is not in the execution. It’s in the decision-making that precedes execution. And that decision-making requires a level of integration that most advisory structures don’t provide.

The tax implications of an options position are material and specific: premiums paid for puts are not immediately deductible; premiums received for calls affect the holding period of the underlying; certain collar structures can be treated as constructive sales under tax law. These are not abstract concerns. They determine whether a strategy that looks protective on a pre-tax basis is actually protective on an after-tax basis.

Estate planning context also matters. The cost basis of the underlying shares, the ownership structure through which they are held, and the intended disposition of the position at death or transfer all affect which options strategies are appropriate and how they should be structured. Advisors who integrate investment, tax, and estate planning approach options as one tool in a coordinated plan — not as a standalone investment decision. The conversation is not “should we buy a put?” It’s “given everything we know about this client’s tax situation, estate plan, liquidity needs, and concentration risk, what’s the right structure for protecting this position?”

The Question Worth Asking Your Advisor

For HNW investors with concentrated equity positions, the most useful question to put to your advisory team is not “do you offer options strategies?” Most firms with any investment sophistication will say yes. The useful question is: how would you think about managing downside risk on this position in a way that accounts for my tax situation, my estate plan, and my liquidity needs — simultaneously? The answer to that question reveals whether the advisory team has genuine integration across disciplines, or whether options, if they come up at all, will be addressed in a silo separate from the planning that gives them their value.

Recommended Articles

For more on Derivatives Basics, explore these related articles from our Derivatives Basics guide.