Part of our Financial Markets Basics guide

What is a Custodial Account?

A custodial account is a savings account at a financial institution like banks, mutual funds, insurance companies, non-banking financial institutions, stockbrokers, etc., maintained mainly for the benefit of beneficiaries. At the same time, continuously administered by a person termed as the responsible person, custodian, or legally recognized guardian.

According to the above definition, it is quite clear that two parties are involved: the custodian and the beneficiary. One can open a saving account with a financial institution or bank, which allows the responsible party to invest the number of other parties for a specific period in this type of account in exchange for a custodial account brokerage.

Key Takeaways

- A custodial account is a savings account at a financial institution such as a bank, mutual fund, insurance company, non-banking financial institution, stockbroker, etc., maintained mainly for the beneficiary’s benefit.

- Uniform Transfers to Minor Act Accounts (UTMA) and Uniform Gifts to Minor Act Accounts (UGMA) are custodial accounts.

- In a custodial account, the banks hold investments on the responsible person’s behalf for another person’s benefit. Typically, minors, as the person does not have legal rights on the investments.

- Still, a deposit account is where the banks and the financial institutions are responsible for holding the funds, e.g., the savings bank accounts.

How Does a Custodial Account Work?

A custodial account is like a regular savings account. A custodian makes decisions about when and how much money to invest in a custodial account. Here, the account manager is a person who makes a continuous contribution to the find.

Further, one can use it to invest funds in various assets, but it depends on the financial institutions accepting the investment in a particular asset. In the case of a custodial account for a minor, one can invest the amount in the account by the minor’s legal guardian or parent. The amount is kept in a custodial account till the minor reaches the age of majority.

Moreover, one can open a custodial account using various forms, including one for minors where the custodian is usually the minor’s parent. Another form is operated and owned by companies, individuals, or institutions to distribute funds in such accounts rapidly.

Thus, a custodial account becomes very important for opening a special fund for children or minors by providing their funds at the right time when they attain the majority. Thereby, keeping them apart from their funds from the beginning, provided they abide by the custodial account rules.

How Do You Open a Custodial Account?

- Firstly, one can easily open a custodial bank account since it has straightforward procedures. The services are provided in exchange for a custodial account brokerage which is similar to charges for other type of accounts.

- An individual can open an account online on the broker’s website or other financial institutions. Else, a person can go individually to the broker’s branch and request to open a bank account. Before opening a custodial bank account with any broker, the fees, payment and contribution structure, and interest rate are essential.

Types

The following are the major types one could open with a financial institution based on their requirements and the custodial account rules that fit their vision the best. Let us briefly discuss the types through the discussion below.

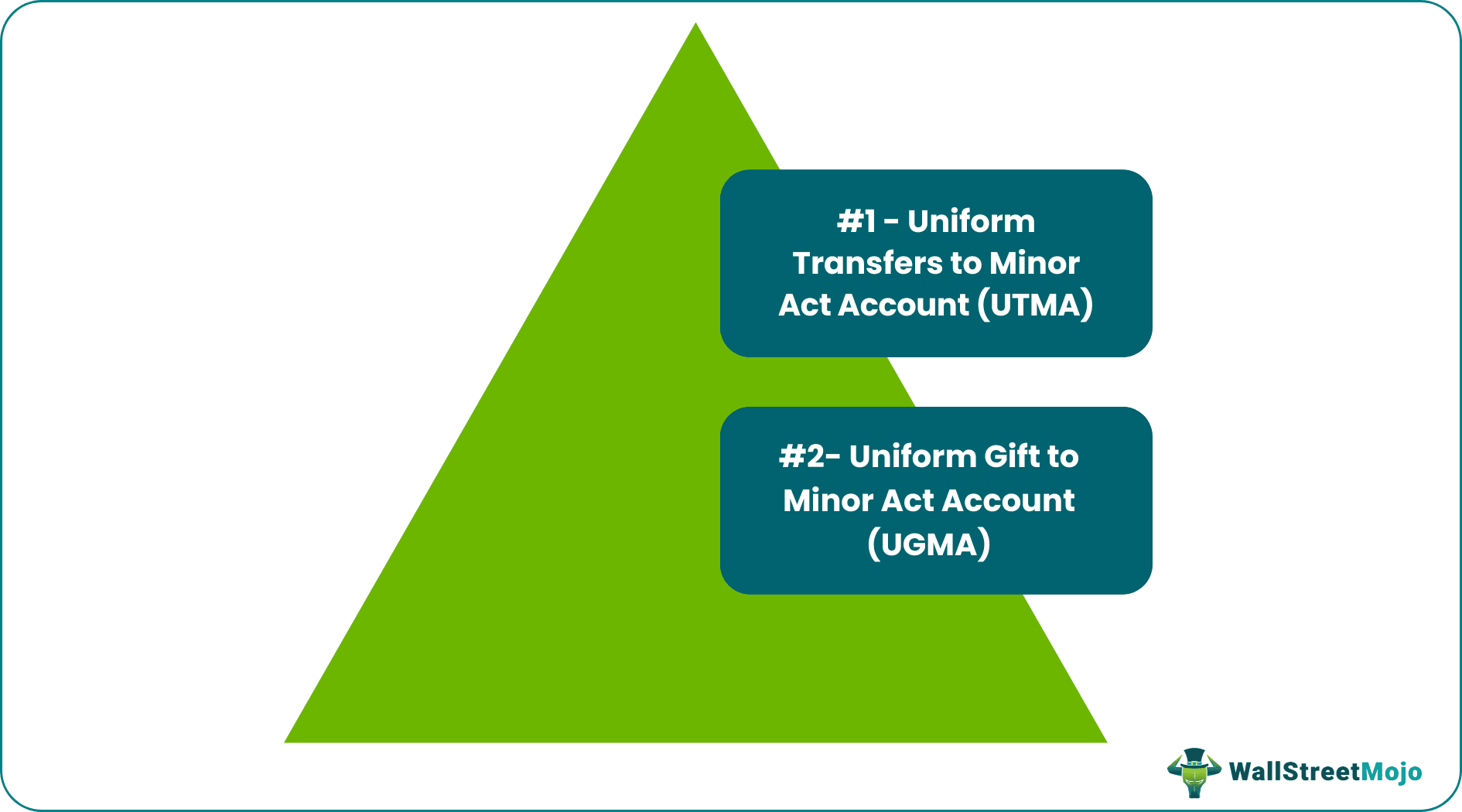

#1 – Uniform Transfers to Minor Act Account (UTMA):

This account can hold almost all types of assets in the pool of investments, including real estate, Intellectual Property (IP), etc. It is, hence, the most significant benefit of this investment. Almost all the financial institutions in the U.S. allow this type of account.

#2 – Uniform Gift to Minor Act Account (UGMA):

This type is used as a gift to the minor once they attain the age of majority. It is pertinent to note that the UGMA account is limited to stocks, cash, bonds, shares, etc., against all the assets under the UTMA account.

Examples

A custodial account is an excellent way of providing a facility to children. Let us understand the ebbs and flows of this concept with the help of a couple of examples.

Example #1

Joe and Maria prepare a Trust fund

for their children of minority age, Aaron and Ben. The trust provides the funds at the age of majority as a gift to them. Thus, $10 million is being invested in a trust fund for two children in a family by their parents; the age of maturity is ten years from opening a custodial account for both children.

After adding up interest over ten years to $10 million, the amount adds up to $35 million. The $35 million Shelby now divided between the children pre-specified the specified ratio of 4:3. Thus, Aaron will secure $20 million, and Ben will get $15 million from the trust fund.

Example #2

Since custodial account rules do not restrict the savings only for educational purposes, parents can choose to invest their hard-earned money towards their child’s education and a better lifestyle through either UTMA or UGMA accounts to ensure a gift that contributes towards a life beyond college.

These accounts are considered one of the top 5 investments in the U.S. made towards the betterment of their child’s future.

Benefits

The benefits of spending on a custodial account brokerage go beyond just education expenses. Let us understand the benefits through the discussion below.

- The most significant advantage of this kind of account is that it keeps the money of dependent people safe and secured until the right time. For example, the achievement of the majority age.

- The custodial account comes with a significant level of flexibility since there are no specific income or contribution limits.

- It has the option of investing contributions to various kinds of assets. However, exceptions are always there.

- Establishing a trust fund is more beneficial and cheaper than setting up a trust fund in a bank or other financial institution.

- Further, there are also various tax benefits to individuals.

Limitations

The Custodial account rules might be a hinderance for most parents or individuals looking to invest towards their child’s future. Below are a few points to consider before investing in accounts of this nature.

- Once one deposits the money in a custodial account, the capital’s ownership is transferred instantly to the beneficiary or the child. Thus, a person can do no action to restore the money.

- It counts the fund in the asset fund of the child even though the money is receivable on a future date when the child is a beneficiary.

- Even though tax advantage is received, it is comparatively lesser than other accounts.

Custodial Account vs. Deposit Account

In a custodial account, the banks hold investments on behalf of the responsible person for another person’s benefit. Generally, the minors, since the person does not have the legal rights on the investments.

However, a deposit account is an account where the banks and the financial institutions are responsible for the accounts, for example, the saving bank accounts.

Frequently Asked Questions (FAQs)

How to get money out of a custodial account?

There is another legal way to start funds from this account type when one wants to withdraw money from a custodial account and demonstrate that the funds will be used only for the minor and the minor: a UGMA or a UTMA.

Can you day trade with a custodial account?

No, one cannot day trade with this account, such as UTMA or UGMA accounts, primarily designed for a minor’s benefit. Day trading typically requires active trading, rapid decision-making, and frequent trades. Hence, these activities are not aligned with the purpose and restrictions of custodial accounts.

Can a grandparent open a custodial account?

A parent or grandparent generally creates a custodial account to benefit a minor child or grandchild. If one puts money into a custodial account, one gives a gift to the minor beneficiary, although the minor does not regulate the account.

Recommended Articles

This article is a guide to Custodial Account and what is it. Here, we discuss how to open it, types, and have compared it with deposit accounts. You can learn more about financing from the following articles: –