Financial Institutions Meaning

Financial institutions are entities that help individuals and businesses fulfill their monetary or financial requirements, either by depositing money, investing it, or managing it. Some of the institutions labeled under this category include – banks, investment firms, trusts, brokerage ventures, insurance companies, etc.

As the financial institutions enable individuals and companies to save, manage, invest, and use the funds productively, the administrative authorities of a nation take due care of their regulations. If not dealt with well, these institutions might collapse, damaging the economy to a great extent. In short, a properly regulated financial entity will mean a healthy economy.

- Financial institutions are the economic entities that help individuals and businesses with several financial services, enabling them to deposit, save, invest, and manage their monetary resources.

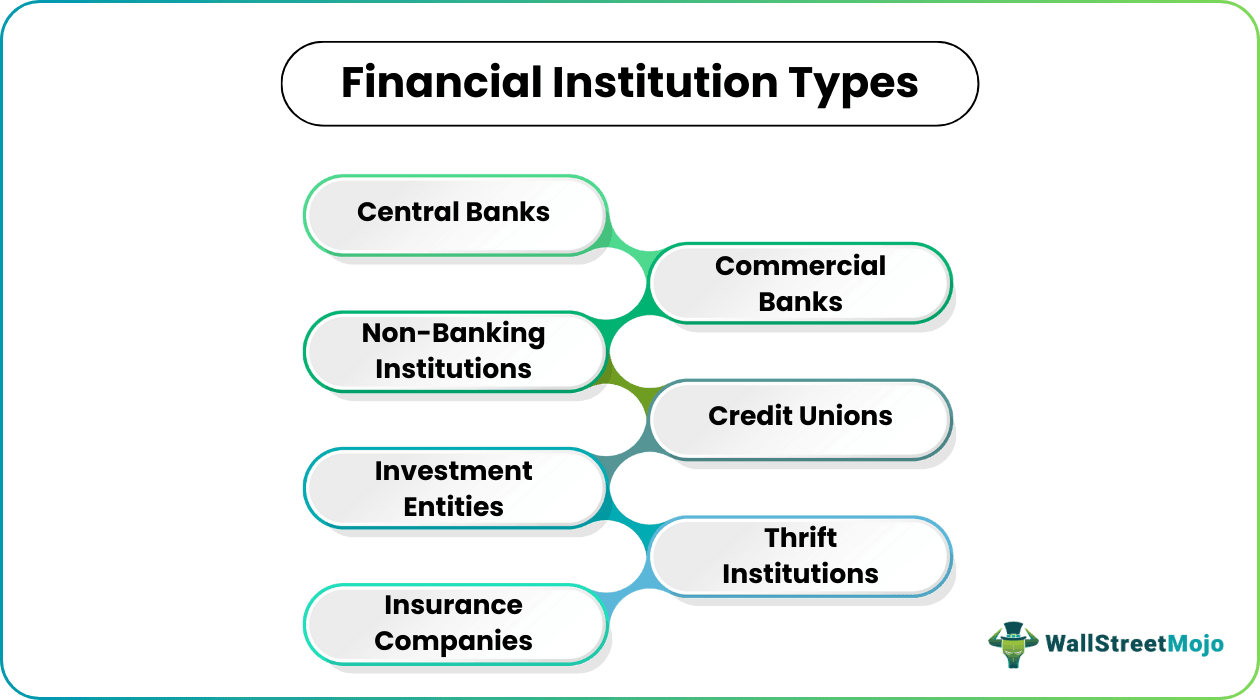

- Central banks, commercial banks, investment entities, credit unions, thrift institutions, insurance companies, etc., are some of the widely available financial institution types.

- They also offer consultation services to consumers who seek advice on the pros and cons of making a particular investment.

- These institutions are strictly regulated by national authorities to keep the financial structure and market active and efficient.

How Do Financial Institutions Work?

Financial institutions, as the name implies, are entities that deal in finances. They offer a wide range of monetary or financial services to individuals and businesses. From helping individuals save money to enabling them to invest in stocks, such institutions serve different functions simultaneously.

There are various types of financial institutions to fulfill different requirements of customers. They look into the customer’s financial needs, be it an individual or a company, and offer relevant services. These entities provide customers with valuable pieces of advice while choosing appropriate financial investment or savings options. The professionals explain the pros and cons of each alternative for their customers to decide which investment they should spend on.

The national and international financial institutions have a great role in ensuring a healthy economy. With the give and take of the monetary resources, the flow of transactions remains balanced, which keeps the economy going. Moreover, such entities in the nation make the market liquid, triggering more economic activities in the respective countries. Therefore, any damage to these financial entities can have a direct negative impact on the economic health of the nation.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Types of Financial Institutions

There is a wide range of such institutions operating around the world. However, the commonly identified types are as follows:

#1 – Central Banks

These are the financial entities that monitor and oversee the procedures of the other financial or banking institutions in the nation. They do not deal with individual customers directly. Instead, they finance other retail banks. In short, these are banks for the banks. Every economy has a separate central bank and is named differently. For example, in the United States, the Federal Reserve Bank is the central bank.

#2 – Commercial Banks

Retail and commercial banks are widely available to serve the financial needs of individuals and businesses. From depositing money to borrowing amounts to buy property, these banks act as saviors for people in need to secure their future financially. Some of the products that these banks offer include savings accounts, personal loans, mortgage loans, certificates of deposits (CDs), credit cards, etc.

#3 – Non-Banking Institutions

Non-banking financial institutions (NBFIs) are entities that neither acquire a valid banking license nor do they allow customers to deposit amounts. However, these entities can offer alternative financial facilities to customers, including investment, consultation, brokerage, transmission, and risk pooling services.

#4 – Credit Unions

The institutions offer traditional banking services but are not publicly traded entities. They are established and operated by the members, the ultimate shareholders. These associations use and reinvest the money received as an interest to keep the costs low. As a result, they become the better choices for members to fulfill their financial needs. These entities enjoy tax-exempt status as not-for-profit organizations.

#5 – Investment Entities

The investment banks and brokerage firms fall under this non-depository category. The investment firms help corporations, governments, and other entities build capital, raise funds, and gain financial advice. These entities, as brokerage ventures, let customers acquire finances by investing in securities, like stocks, mutual funds, bonds, and exchange-traded funds (ETFs). In addition, it acts as a guide to startups or companies in conducting complex transactional processes. They also offer advice for initiating fruitful mergers and acquisitions (M&A).

#6 – Thrift Institutions

Also referred to as savings and loan associations, these entities allow up to 20% of total lending to customers, who are also their owners. They help individuals enjoy opening accounts and acquiring personal loans and home mortgages.

#7 – Insurance Companies

These financial institutions allow individuals and businesses have policies against monthly premiums, which they are subject to pay at regular intervals. In addition, these schemes offer coverage or protection to assets against any financial risk they remain exposed to.

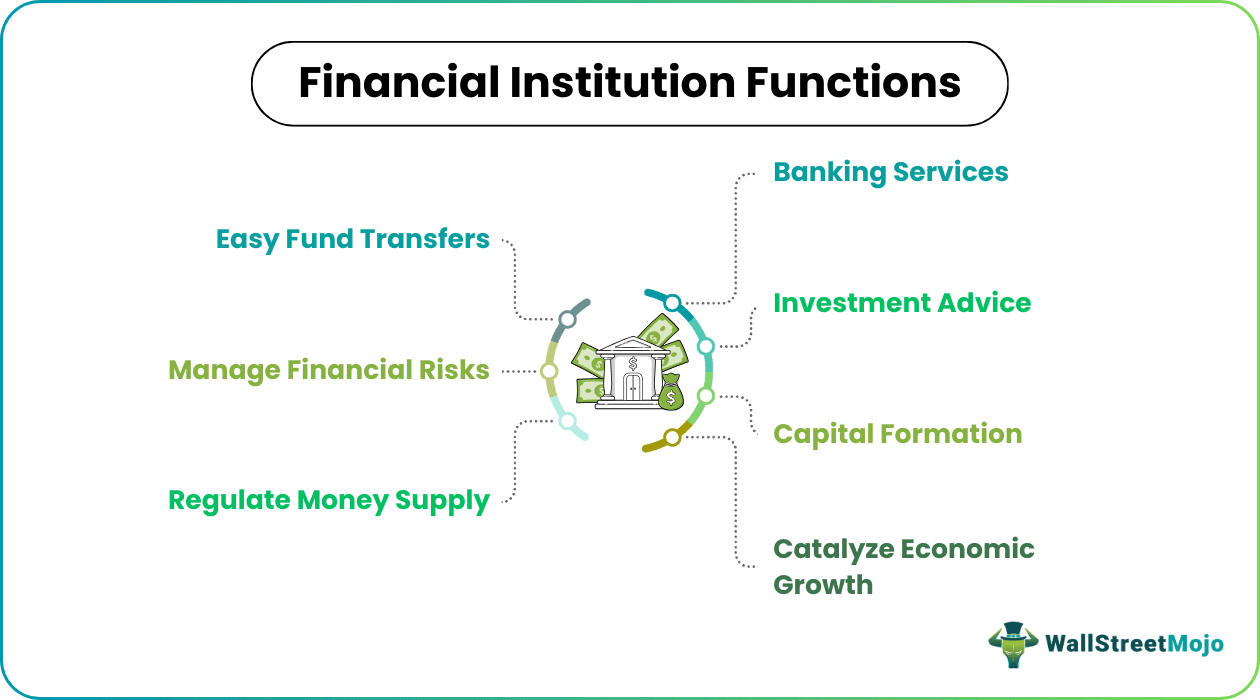

Functions

Though the financial institutions aim to ensure a healthy economy, there are other minor and major roles they play to ensure they achieve their final goal.

The primary function of these institutions is to regulate the money supply. With the regular flow of money, the financial entities keep the financial ecosystem active. The money supply process must be efficient, given the wide use of money in carrying out transactions.

One of the most common functions of these institutions is banking and investment services. They serve individual customer needs, be it a person or a business. They allow them to deposit their money, save it, earn interest, and invest further. In addition, as a non-banking institution, they also offer consultation facilities to customers and help them know the pros and cons of investing in a financial product, be it stocks, bonds, ETFs, mutual funds, etc.

For startups, their investment advice works and helps them build huge capital by opting for Initial Public Offering (IPO) to raise sufficient funds. Moreover, by keeping the financial ecosystem active, these institutions ensure being ready to manage any financial risk and foster the economic growth of a nation.

Above all, in this era of internet banking, financial entities make transferring funds from one account to another online easy, smooth, and safe.

Examples

Let us consider the following financial institutions examples to understand how they work:

Example #1

The importance of the financial institutions can be observed from the way governments interfere as and when these entities in their respective nations suffer turmoil. The authorities try their level best to protect them from the financial crisis and help them prevent their collapse. For example, in the 2008 financial crisis, the administrative authorities helped many financial institutions from getting bankrupt. These entities included the American International Group (AIG), Bank of America, Citigroup, etc.

Example #2

One of the most significant financial institutions in the United States is Wells Fargo. It operates almost 6% of the bank branches in the nation. Though there are many other institutions that the Americans may take into account, they prefer Wells Fargo over the rest. The only reason behind this is the significantly low monthly fees and higher transaction limits that it offers.

Regulations

These institutions need to be regulated strictly to ensure they keep doing their best to maintain the financial market. Therefore, every country has a specific regulatory mechanism to control and supervise how these entities perform. For example, in the United States, the Federal Deposit Insurance Corporation (FDIC) takes care of the depository financial entities. Others include the National Credit Union Administration (NCUA), Office of Thrift Supervision, Office of the Comptroller of the Currency, etc.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What are financial institutions?

Financial institutions refer to entities that have been established to offer financial services to customers, be it an individual or a business. They have an important role in maintaining the economic ecosystem of a nation as they regulate the money supply through the consistent movement of the monetary resources in the market.

Who uses financial institutions?

Individuals and businesses use these entities to serve their personal and professional financial requirements and commitments. These institutions allow customers to deposit money, withdraw when needed, transfer them online instantly, save them for future use, and manage them smartly for gains. They are also for those who want to buy and sell stocks, bonds, and derivatives to earn profits.

Who regulates financial institutions?

The nations have strict regulatory mechanisms for financial institutions. Though it differs from country to country, each regulatory authority aims to ensure these entities keep the financial market and the economy active and efficient. In the United States, the following bodies look after the institutions:

1. The Federal Deposit Insurance Corporation (FDIC) – Depository Institutions

2. National Credit Union Administration (NCUA) – Credit Union

3. Office of Thrift Supervision – Thrift Institutions or Savings and Loan Associations

4. Office of the Comptroller of the Currency – National Banks

5. Others

Recommended Articles

This article is a guide to what is Financial Institution and its meaning. Here we explain its types, functions, and regulations along with examples. You can learn more about corporate finance from the following articles –