Part of our Consumer Behavior guide

Disposable Income Meaning

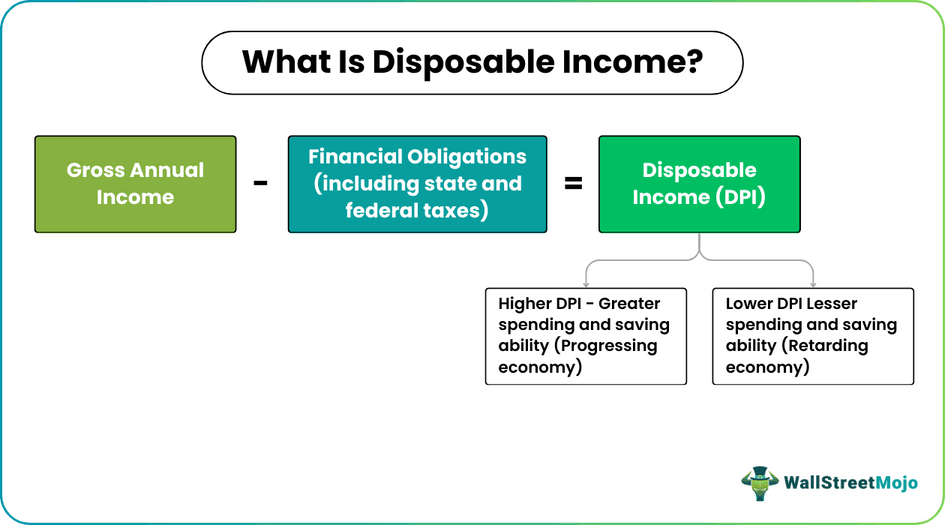

Disposable income (DPI) is the portion of the gross annual income left with individuals after paying off all their financial liabilities, including federal and state taxes. The DPI is the real income that people can spend on fulfilling their household needs and investing in different savings schemes.

Also referred to as disposable personal income, this amount determines the spending capability of an individual. Therefore, a higher DPI would mean a better ability to spend, signifying a healthy economy. Thus, having a good DPI is important to ensure a nation’s economy is up to the mark.

- DPI, also known as the net pay or disposable personal income, is the amount individuals are left with after taxes and other deductions from their gross annual income.

- When the DPI is higher, the spending and saving capability of the population is more. As they spend more, the market improves, and so does the economy.

- Financial analysts use the DPI as an indicator to figure out if a nation’s economy is improving or is becoming stagnant.

- DPI is an important factor in calculating other financial metrics, including discretionary income, MPC formula, MPS, and personal savings rate.

Disposable Income Explained

Disposable income (DPI) is the amount that wage or salary earners are left with after making the necessary deductions. It is different from the gross income which is the total amount that individuals receive as their wage or salary, including certain financial obligations to be paid off. The DPI is the remaining amount that individuals have after the financial liabilities are taken care of.

The DPI is also known as the net pay a person receives. It determines how capable one is of handling household expenses or spending on lifestyle. It plays a vital role in making citizens decide what to spend on, how much to spend, and save for a financially secure future. However, in both instances, disposable personal income determines how healthy an economy is.

When people have better disposable personal income, they have higher spending ability. As they can spend more, they have significant purchasing power. Therefore, they can buy consumer goods and services to meet their household requirements and have luxury items for use. When the market grows, the economy strengthens, and this is how the whole concept of DPI works.

Similarly, when the savings increase, it helps banks be more open to providing loans to people seeking them. As a result, the financial sector remains active, thereby enhancing the economic condition of any country across the globe. Therefore, calculating the DPI becomes an important factor as higher savings and greater spending abilities indicate a growing economy.

Disposable Income (DPI) Explained in Video

Related Metrics

The DPI acts as a factor that helps calculate or derive several other financial metrics. Some of them are as follows:

#1 – Personal Savings Rates

It is the percentage of income that goes into savings for retirement or other purposes.

#2 – Marginal Propensity to Consume (MPC)

It is the percentage of every extra dollar that one spends on disposable personal income. The MPC depends on raising or lowering levels of discretionary income, which serves as an important indicator for economists to gauge the levels of spending and increasing or waning interest of individuals in spending a greater amount of what they can choose to save or spend.

#3 – Marginal Propensity to Save (MPS)

It is the percentage of each additional dollar that one saves out of the disposable personal income. MPS also depends on changes in discretionary income levels available to an individual or household, depending on the DPI. It is yet another economic indicator often used to study individuals’ increasing or declining propensity to save in a specific economic environment.

Formula

DPI is the difference between the gross annual income and the sum of all deductions, including local, state, and federal tax liabilities. The disposable income formula to express the same is as follows:

Disposable Income (DPI)=Gross Annual Income-(Payable Taxes+Other Deductions)

This DPI becomes the net pay for an individual wage or salary earner.

Example

Let us consider one of the disposable income examples to understand how it works:

Joseph has a gross annual income of $80,000. He is liable to pay 10% tax on the amount, and other deductions are worth $4,000. Based on the information provided, the earner does the disposable income calculation:

DPI =Gross Annual Income – (Payable Taxes + Other Deductions)

= 80,000-(10% of 80,000+4,000)

=80,000-(8,000+4,000)

=$68,000

This $68,000 is Joseph’s disposable personal income or take-home pay, which he can use to meet household requirements and invest in different savings schemes.

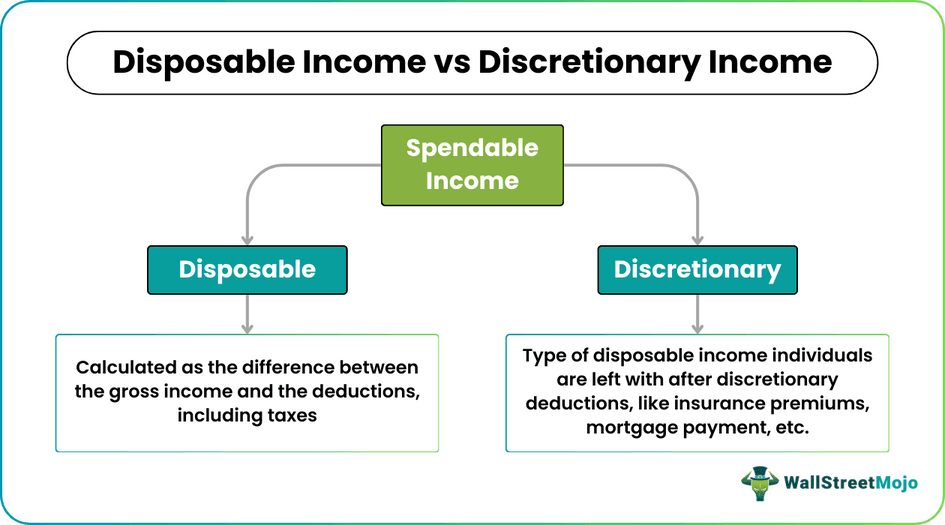

Disposable Income vs Discretionary Income

Disposable personal income is the individuals’ income after the current taxes and other deductions. It is the net pay received, which the salaried or wage staff and workers can spend to meet their everyday needs, including basic and luxurious necessities.

On the other hand, discretionary income is a type of DPI obtained by subtracting other financial obligations that individuals have from their disposable personal income. This is the deduction that people choose to go for at their will. Such deductions include paying for food, rent, mortgages, insurance schemes, etc.

Let us have a glance at the differences below to understand the discretionary income and disposable income definition properly:

| Category | Disposable income | Discretionary income |

|---|---|---|

| Expression | Gross income – Personal Taxes and other deductions | Disposable income – Discretionary spendings |

| Necessity | Yes, necessary | No, at will |

| Examples | Household requirements and basic needs | Food, rent, insurance schemes, luxury, etc. |

Frequently Asked Questions (FAQs)

What is disposable income?

Disposable personal income is the net pay individuals are left with after the taxes, and other deductions are made from their gross personal income. This amount is used to fulfil the necessary household requirements and savings needs of the earners.

Why is disposable income important?

Calculating the DPI is important as it acts as a parameter based on which the financial analysts figure out whether an economy is progressing or retarding with time. In addition, the DPI determines the capability of individuals to spend and save. When the DPI is more, an individual’s spending and savings ability are high. As a result, it indicates that the economy is on the right track.

How much disposable income should one have?

In the United States, the DPI per capita as of 2020 was worth $52,800.

Recommended Articles

This article is a guide to what is Disposable Income and its meaning. Here we explain the concept with calculation-based examples and its differences from discretionary income. You may have a look at the below useful articles: –