Part of our Taxable Income and Gains guide

Dividends Received Deduction (DRD) Meaning?

→ Explore all 34 Dividends articles

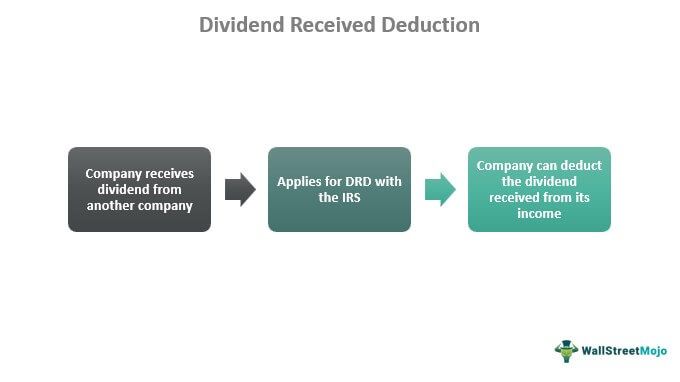

Dividends received deduction (DRD) refers to a tax provision that allows a company to deduct the dividend received from another company from the taxable income. In the United States, it applies to C corporations under the federal income tax law.

The provision results from strategies intended to reduce the impact of triple taxation. For example, when one corporation holds shares in another corporation, triple taxation exists, and the subsidiary’s income may be subject to three taxes.

Key Takeaways

- Dividends received deduction allows eligible companies to deduct the dividend from another company from the taxable income.

- In the United States, the provision is available under the federal income tax law. It does not apply to individual citizens but is provided only to certain companies that qualify and meet its requirements.

- If a C corporation owns less than 20% of the dividend-distributing company, the DRD will be 50%; if the ownership percentage lies between 20%-80%, then the DRD will be 65%, and if it owns more than 80%, the DRD will be 100%.

Dividends Received Deduction Explained

Dividends received deduction is a simple yet specific tax provision for US corporations to deduct the dividend they receive from another company. This tax provision is only given to companies and not to any individual. Additionally, the company must meet specific requirements and be a C corporation to qualify for the DRD.

The corporate dividends received deduction is a tax benefit a corporation can apply and reduce their taxable income by eliminating a certain percentage of it that they received as a dividend from another company. It varies per the rules the TCJA and IRS established, making it complex and challenging to interpret. Over time, many changes have been made in the tax provision to ensure that it benefits the company and the federal government. In this endeavor, the official bodies also found loopholes and regulations companies misused to reduce their tax liability.

Dividends Received Deduction Rules

- Companies cannot apply DRD if it is a capital gain dividend from a regulated investment company.

- After 2017, the aggregate deduction allowed under IRC 243, 245, and 250 limits it to 50% if the recipient company owns less than 20% of the offering company.

- If the recipient company owns more than or equal to 20% but less than or equal to 80% of the dividend-distributing company, a 65 % deduction is allowed by IRC 246 (b).

- The receiving corporation cannot avail DRD if the company delivering the dividend is exempt from taxes under sections 501 or 521 of the IRC for the distribution’s tax year or the prior year.

- For foreign companies, the recipient company must have held their stock for at least 365 days for the deduction qualification.

Calculation Example

Corporation A receives $10,000 from corporation B. Corporation A is entitled to a deduction of 50 percent of its dividend, which is $5,000. If corporation A owns 40% of corporation B, the deduction amount increases to 65 percent, which is $6,500. Finally, if corporation A owns 80% of corporation B, it is allowed to deduct 100 percent of the dividend received, which is $10,000.

It is a simple DRD example, but several rules and regulations restrict corporations from getting such tax provisions parallelly in the real world. The above example also indicates that getting a 100% dividend deduction is possible.

Limitation

The dividends received deduction limitations are:

- The deduction is only available to C corporations and is not provided to LLCs, individuals, or S corporations.

- The recipient company must hold the common stock for at least 45 days.

- A company is entitled to a 100% DRD only if the company owns more than 80% of the dividend-distributing company.

- The corporate shareholder‘s taxable income impacts the amount of the DRD. According to IRC section 246(b), a company entitled to a 70% DRD may only deduct the dividend amount up to 70% of the corporation’s taxable income. Additionally, only 80% of the corporation’s taxable income can offset the dividend amount for a business entitled to an 80% DRD. The taxable income limitation has two exceptions. First, a corporation with a 100% DRD is not subject to any restrictions on taxable income. Second, the limitation does not apply if the DRD rises and results in a net operating loss.

Tax Reform

The TCJA minimized the corporate tax rates to 21%, earlier, up to 35%, but it did not share the intent of decreasing the effective tax rate on dividends received by a company. To correct this, the TCJA lowered the DRD percentages from 80% to 65% only if a C corporation holds stock between a bracket of 20% to 80%.

Before TCJA, the DRD tax on affiliate dividends of 35% x (1-80) = 7.0% but in comparison, after TCJA, the lowered DRD induces a tax on affiliate dividends of 21% x (1-65%), which is equal to 7.35%. At the same time, there is no material difference in the dividends tax. If a C corporation owns less than 20%, the DRD will be 50%, and if it owns more than 80%, the DRD will be 100%.

Frequently Asked Questions (FAQs)

What qualifies for dividends received deduction?

A 50% deduction is typical if the dividend-paying company is also a US organization. Still, it can increase to 65% if the recipient company owns at least 20% but less than or equal to 80% of the dividend-distributing firm. Apart from this, multiple layers called tiers separate the deduction percentage.

Where do the dividends received deduction go on 1120?

In general, Line 9, Column (c) of Schedule C may not exceed the sum from the Dividends Received Deduction Limitation Worksheet, according to the guidelines for that line.

What is the exemption limit to DRD?

The corporate shareholder’s taxable income impacts the amount of the dividends received deduction. According to IRC section 246(b), a company entitled to a 70% DRD may only deduct the dividend amount up to 70% of the corporation’s taxable income. Additionally, only eighty percent of the corporation’s taxable income can offset the dividend amount for a business entitled to an eighty percent DRD.

Recommended Articles

This article has been a guide to what is Dividends Received Deduction & its meaning. We explain its rules, limitations, calculation, example, and associated tax reforms. You can learn more about it from the following articles –