Dividends Meaning

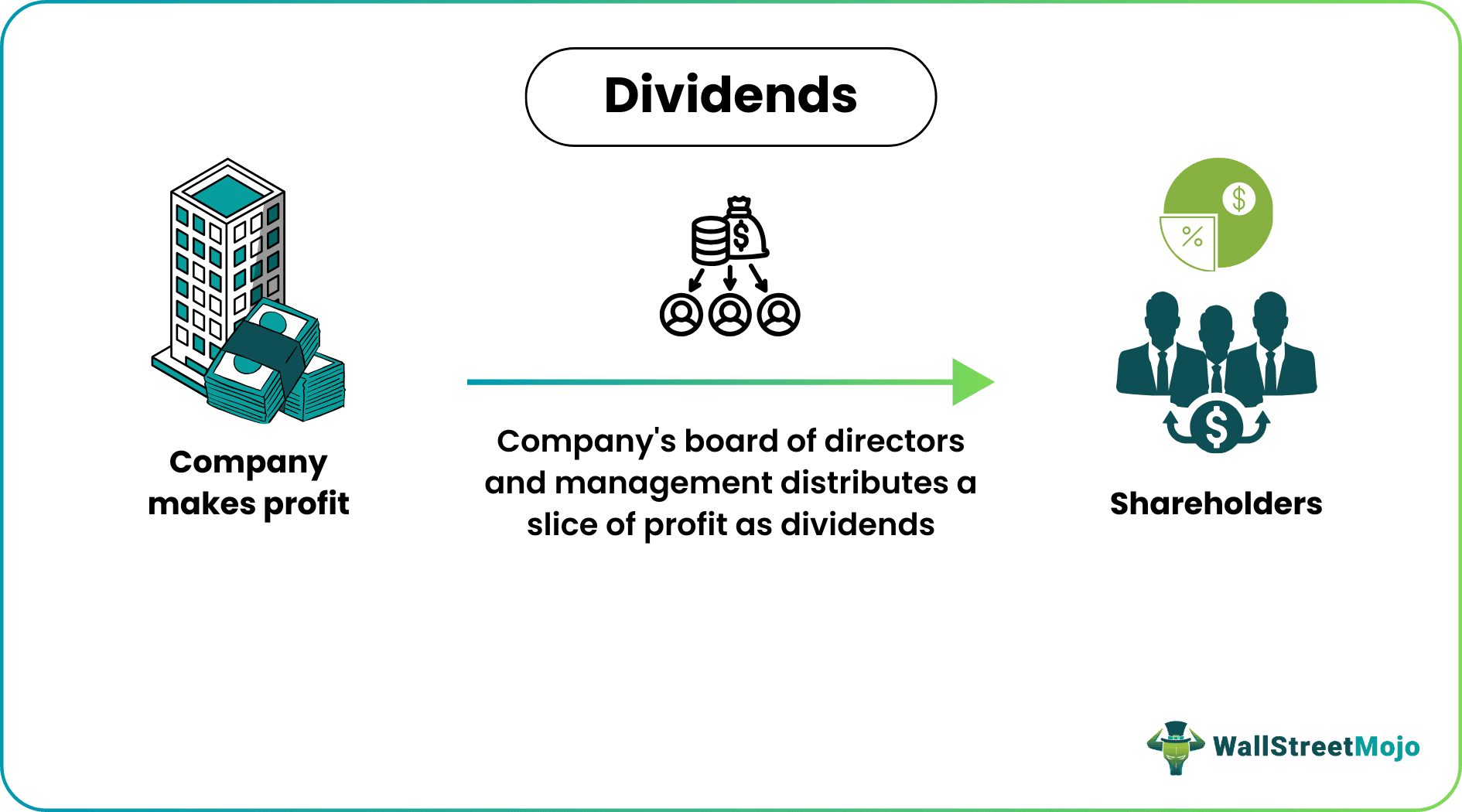

Dividends refer to the portion of business earnings paid to the shareholders as gratitude for investing in the company’s equity. They are issued in cash or as additional shares with the board of directors of a company taking such decisions.

Not all stocks offer them as it is an expense for a firm and brings down its retained earnings. Reinvestment of retained earnings is crucial for business growth. Investors prefer dividend-bearing stocks as they provide a relatively steady income over and above the earnings that can come off through share trading.

- Dividends are rewards paid to the shareholders of a company typically out financial earnings. Usually, preferred stockholder who have no voting rights hold a greater priority to receive them than the common stockholders who have the voting rights.

- The yield is determined by dividing the annual dividend on each stock by the price per share. Yield helps define profitability of the earnings by shareholders.

- The issue can take many different forms including cash, stocks, property, and scrip among others.

- It is a taxable income for the shareholders, and the tax amount on the same is deducted at source, i.e., by the company at the time of distribution.

Understanding Dividends

Dividends reflect a company’s earning capabilities being a source of income. They are usually paid out of a firm’s profits or accumulated earnings to keep the shareholders invested in the stock. However, being an expense, it reduces retained earnings which not all companies can afford. Also, when in loss, companies cannot issue them.

Since the law doesn’t obligate firms to issue dividends, many prefer to reinvest their earnings to overcome shortfalls or direct the funds towards business growth projects. Large-cap stocks and well-established public companies tend to issue them more as they are financially better placed. For instance, AT&T has over 30 years of history of providing dividends, with their 2021 yield being 7.43% at $2.08 per share.

Consequently, such stocks attract investors for offering a relatively steady income over and above the earnings that can come through their sales. Some companies also issue a one-time lumpsum payment to reward their shareholders. The board of directors is responsible for decisions related to profit distribution, which occurs in consent with major stakeholders.

It involves certain decisions based on the type of shareholders, the status of company earnings and the type of issue, among others. For example, preferred stockholders hold a stronger claim over these earnings than the company’s common shareholders.

Chronology of Dividend Issue

The frequency of dividend issues can be monthly, quarterly, annual or semi-yearly, and it involves following a calendar. A company marks certain dates on its calendar to make public announcements and also for charting out distribution details. The Board of directors, together with shareholders’ approval, are responsible for these decisions. Let us take you through them.

- Announcement/ Declaration Date: An important element of the calendar, a company’s management announces the upcoming dividend distribution with the declaration date. The payment amount or the type of issue is also decided by the board.

- Ex-Dividend Date: It can be taken as a cut-off date, prescribing the shareholders eligibility to receive them. For example: If a particular stock declares that the cut-off date is July 30, 2021, only the shareholders who possess the stock on July 30, 2021, will be eligible to receive payments. Investors purchasing the stock on July 30th and following dates will not make the cut.

- Date of Record: The company decides on the list of shareholders who will receive the payment and they are reported under the record date. The payment amount or the type of issue is also decided by the board.

- Payment Date: This is the date when the payment is made by the company to the on-record shareholders through direct bank transfer or mails depending on the type of issue.

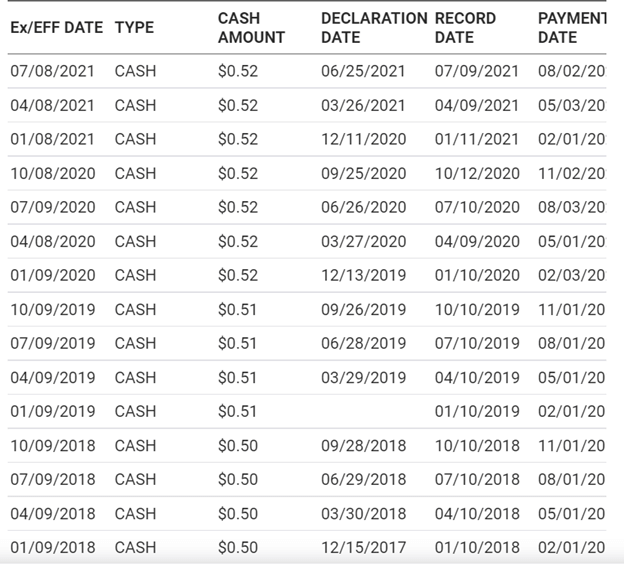

Below is an excerpt from the chronology of AT&T.

Source – NASDAQ

Dividend Stock Examples

Dividends also come from ETFs, mutual funds and index funds if the companies under the fund offer them. When it comes to stocks, oil giant, Royal Dutch Shell (RDS. B and RDS. A), holds an illustrious history of dividend payments.

It is important to note that Covid-19 led the company to cut the payment for the first time since the World War II. However, in July 2021, the company announced a 38% boost of the upcoming payments owing to enormous profits.

In that regard, S&P 500 companies that have consistently raised the payment amount from the last 25 years are called dividend aristocrats. Given below are some of these famous corporations:

- Abbott Laboratories (ABT)

- The Coca-Cola Co. (KO)

- Colgate-Palmolive (CL)

- Johnson and Johnson (JNJ)

- McDonald’s (MCD)

- Procter & Gamble (PG)

- S&P Global (SPGI)

- Walmart (WMT)

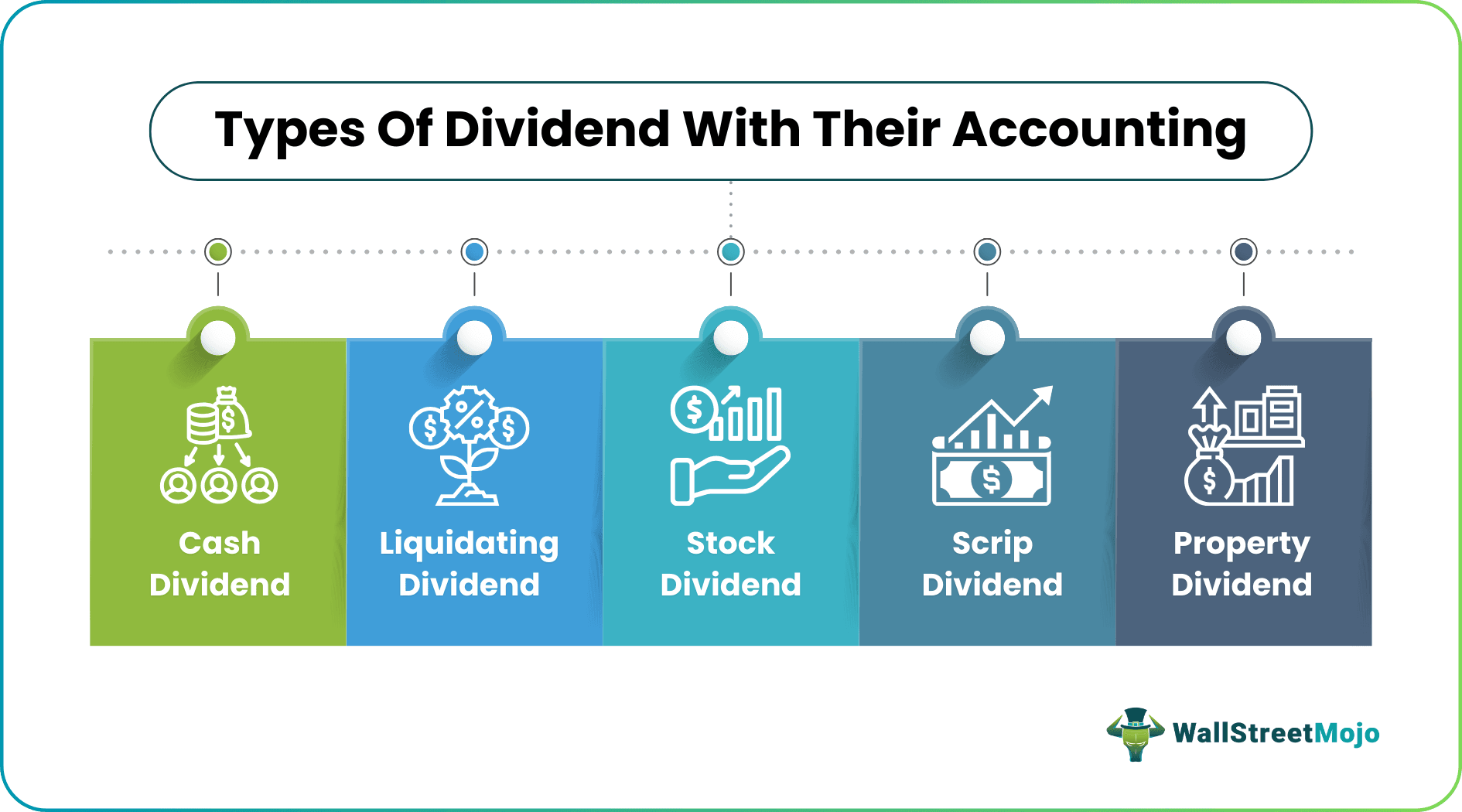

Types of Dividends with their Accounting

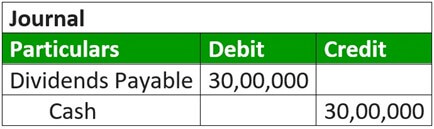

1. Cash Type

Here they are paid as cash either through a check or direct bank transfer.

Example

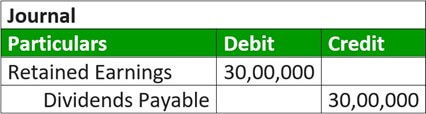

Midterm international Ltd, on January 1, 2019, held the meeting. The cash payment of $1 per share was declared on the company’s outstanding shares. The total outstanding shares of the company are $3,000,000. The initial journal entry that the company will record is –

Now on June 1, 2019, at the time of cash payment, the company will record the transaction as below –

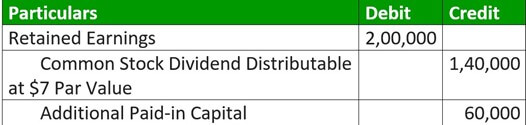

2. Stock Type

Here the company issues common stock to the present common shareholders. The treatment depends on the percentage of an issue concerning the number of the entire previous share issue. If the issue is more than 25%, it will be treated as a stock split.

Example

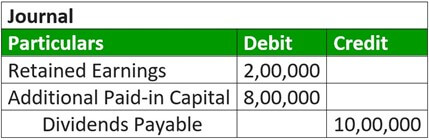

On January 1, 2019, Midterm international Ltd declared a stock dividend of 20,000 shares. The par value of the shares is $7, and the fair market value is $10.00 on the declaration.

Retained Earnings = 20,000*$10 = $2,00,000

Additional paid-in capital = 20,000*($10-$7) = $60,000

Journal entry after the declaration:

After distribution:

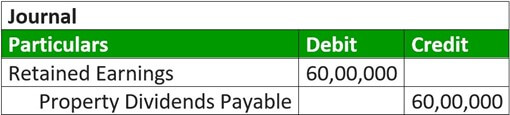

3. Property Type

Companies also grant physical assets, real estate, investment securities, etc., to their shareholders. They must record the distribution at the asset’s fair market value. If the fair market value of the assets distributed is different from the book value of assets, then the company has to record the variance in the form of the gain or loss.

Example

New Sports International Ltd plans to declare the issuance of 10,000 bonds. The fair market value of the bonds on the date of declaration of the dividend is $ 60,00,000, which originally the company acquired at $ 40,00,000.

New Sports International Ltd passed the following entries on the declaration date to record the change in assets value while issuing their allotment.

Gain = $ 6,000,000 – $ 40,00,000 = $ 20,00,000

Entry for recording the gain:

Entry to record the transfer:

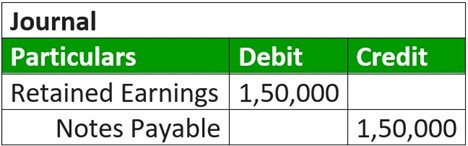

4. Scrip Type

It is a type of promissory note where the company commits to paying the shareholders at a later date. Then, it creates certain notes payable, which may or may not include interest.

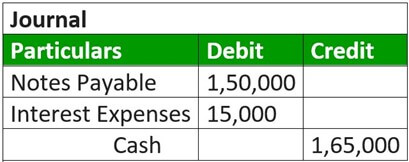

Example

Mid Term International declares a $ 150,000 scrip dividend to its shareholders with an interest rate of 10 per cent. The entries for the same are as follows –

Now suppose the payment date is after one year, so Mid Term International has to pay the notes payable amount and interest accrued during one year from the declaration date.

Interest Accrued = $150,000 * 10% = $15,000

On payment date entry will be:

5. Liquidating Type

It is a payment that allows shareholders to receive their originally contributed capital, primarily at the time of business liquidation.

Example

New Sports International Ltd declares liquidating payments of $10,00,000, out of which $2,00,000 is the income, and the remaining amount is the capital reimbursement.

The entry to record the declaration:

The entry to record the payment:

Advantages and Disadvantages

- Dividends often boost an investor’s trust, and confidence since such companies are considered more stable, profitable and reliable. Moreover, with regular payments, shareholders don’t feel the need to sell out their shares for quick returns.

- It is an essential source of income as pension earnings. For example, when Royal Dutch Shell cut back on these payments post Covid-19, it was expected to affect many pensioners who owned the stock either directly or through schemes.

- Apart from being a token of gratitude, they keep shareholders invested in the firm due to regular earnings. People tend to invest in these stocks more, driving up their prices and bringing more capitalization.

- Also, qualified dividends that are deemed so by the SEC, are taxed at lower rates being treated as long term capital gains. Certain corporates qualify for dividend received deduction. It is a type of tax deduction which certain firms are allowed when they receive a portion of profit as a shareholder of another corporate.

- However, regular delivering of slices of profits often causes cash crunch for business expansion and capital projects. Thus, it hinders growth in the long run. Also, their computation, tax preparation and distributions increase the overhead cost.

- Additionally, since earnings vary for years, sometimes distributions tend to be of meagre amounts, putting off investors.

FAQs

What is a dividend example?

An example of a dividend is cash paid out to shareholders out of profits. They are usually paid quarterly. For example, AT&T has been making such distributions for several years, with its 2021 third-quarter issue set at $2.08 per share.

How are dividends paid?

When a company makes a profit and has retained earnings, the corporate management proposes to offer a slice of profit to the company’s stockholders (preference, common or other ascertained class of shareholders). The board of directors approves this proposal and determines the payment amount, eligible shareholders, and final distribution.

Are dividends taxed if reinvested?

They account for the taxable income of the shareholders in the same year they are distributed if they are of the unqualified kind. The payments will receive taxation whether they withdraw or reinvest it.

Recommended Articles

This article has been a guide to what is Dividend & its definition. Here we discuss its types and accounting along with dividend stock examples. You can learn more about firms from the following articles –