Part of our Microeconomics guide

Economic Depreciation Definition

→ Explore all 77 Fixed Assets and Depreciation articles

Economic depreciation is defined as the wear and tear of an asset beyond its expected capacity or utility, which means that suppose we have an asset and expect the depreciation run to go for four years. Still, it becomes obsolete and scraps in only three years it is said to be economically depreciated.

- Economic depreciation refers to an asset’s wear and tear beyond its expected capacity or utility. For instance, if an asset is expected to depreciate over four years but becomes obsolete and discarded in three years, it is considered economically depreciated.

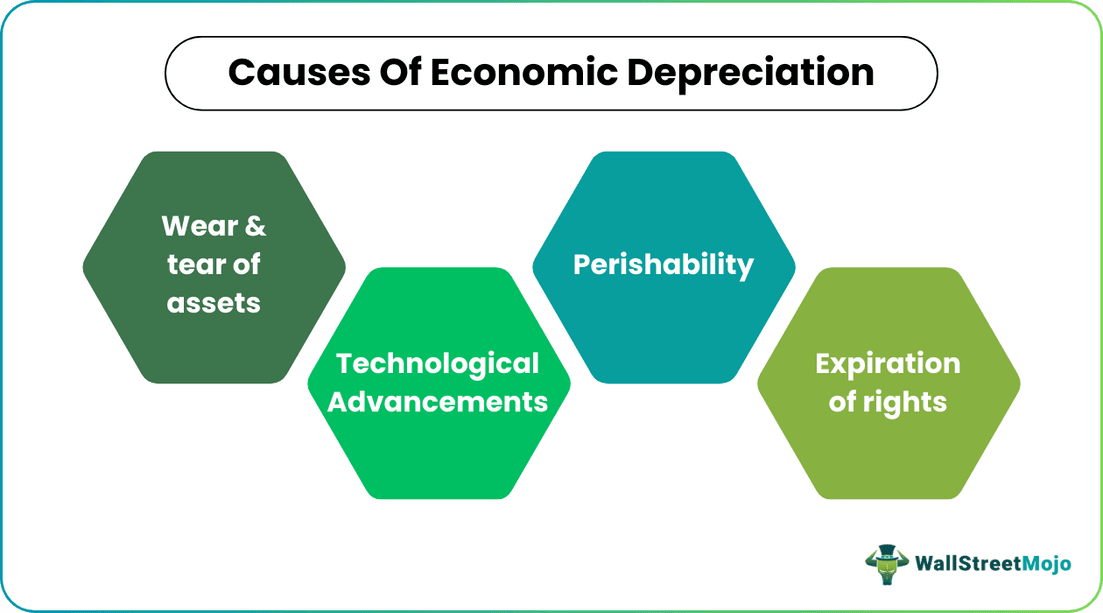

- Causes of economic depreciation include wear and tear of assets, technological advancements, perishability, and the expiration of rights.

- The economic depreciation rate is generally lower than the accounting depreciation rate, resulting in a subsidy that allows for earlier capital replacement.

- Economic depreciation is primarily based on the capital investment concept, while tax laws or IRS rules influence accounting depreciation.

Short Explanation

Economic depreciation is the gradual decrease in the value of assets in a period due to some major changes in the factors crucial to the economy. These types of depreciation are specifically linked to real estate where the property can drastically change its valuation due to sudden events like the road’s closure, depleting neighborhood, or unfavorable conditions. Economic depreciation stands to be different from normal accounting depreciation because, in accounting depreciation, the value of an asset gets depleted over a set period based on a planned schedule. Still, in cases of economic depreciation, the asset becomes scrapped way before the planned schedule due to some unforeseen events.

How does Economic Depreciation Work?

Economic depreciation is generally termed as the process by which assets lose their market value due to some influential factors, which overall leads to the degradation of the asset’s market value. When the owners need to sell their assets, they prefer economic depreciation over accounting depreciation to sell their assets at the market rate. Also, economic depreciation broadly impacts the sale price of any asset which the owners want to sell in the market. It is very common among owners to keep a check and monitor the rate of economic deprecation about the asset one wishes to sell.

Accountants will never record economic depreciation in their accounts or financial statement for big capital assets when it comes to accounting for business needs. Instead, they prefer to use the book value of the particular asset for the main reporting needs. One of the key areas where economic depreciation is considered for financial analysis is in the field of real estate. Economic depreciation can also serve as a forecasting methodology when the analyst wants to forecast how much revenue the good or service will generate in the future.

Causes of Economic Depreciation

Following are the causes –

- Wear and tear of Assets: With time, it is impossible to save assets from wear and tear, which becomes a mandatory attachment with every asset. Thus, the decline in the asset’s physical condition is linked to the market value when we need to sell it again, and this happens by depreciating the financial or monetary value of the asset and accounting the same for it in the mode of depreciation.

- Technological Advancements: Technology is changing rapidly, and new technologies are substituting the older ones every other day. The replacement occurs based on the effectiveness and efficiency of newer forms of technology, leading to the depreciation of assets that run on older forms of technology.

- Perishability: Assets that come into use as raw materials or inventory have a certain expiry date, i.e., they need to be utilized within a certain point of time. They generally lose their value over time and ultimately lose their value as time progresses. Thus these assets need to be depreciated over some time.

- Expiration of Rights: Assets like patents, copyrights, trademarks that are non-tangible are only valid for a specific time which is generally the contract period for which the rights have been granted or contracted. Thus this calls for depreciating the value of such intangible assets before the rights expire, which is broadly called amortization. Thus when amortization of intangible assets occurs, it is accounted for in such a way that when the rights of the assets expire, the asset’s value becomes zero or the asset becomes no more useful.

Economic Depreciation vs Accounting Depreciation

The calculation method of economic depreciation is much more complex than calculating accounting depreciation. When it comes to accounting depreciation, an asset supposes that a non-tangible one is amortized based on a fixed schedule, i.e., it is more time-based. We call this schedule the accounting term as amortization schedule, whereas in cases of economic depreciation, there is no fixed period or schedule involved. It gets amortized based on some influencing factor that affects its market value. The same goes for tangible assets too. The depreciation is calculated over a set period or schedule in accounting depreciation. In contrast, in economic depreciation, the asset value gets depreciated quite before the set point of time due to some influencing factor that affects the asset’s market value.

The economic depreciation rate is almost half of that of accounting depreciation. This difference between both results in the provision of a subsidy and also the replacement of capital at an earlier stage. Economic depreciation can be easily created on a model platform or accounted for by creating impairment charges. Economic depreciation is more based on the concept of capital investment. In contrast, accounting depreciation is driven by tax laws or IRS rules, which states that if a machine has a life of 5 years, it will be depreciated at the same rate regardless of how much longer it could stay in service.

Conclusion

All assets, be it tangible or non-tangible are subject to economic depreciation. It is just the company policy on how this can be analyzed and the effects be followed differently. A company generally is not concerned about market influences or affects its assets but it is more concerned about how the market affects its liquidity position. When it comes to depreciation a company is more concerned about how the assets are marked to market on the final books of accounts since this has a bigger impact on the overall financial performance of a company.

On the other hand, economic depreciation is given more weight by the investors since it affects the portfolio they are holding and also impacts their total net worth on a periodical basis. Economic depreciation is more prevalent among real estate industries where asset owners may see a huge spike and decline in the value of assets on account of several economic factors that directly or indirectly affect the overall market value of the assets.

Frequently Asked Questions (FAQs)

1. Why is economic depreciation important?

Economic depreciation is important because it reflects the decline in the economic value of an asset over time due to factors like wear and tear, obsolescence, or changes in market conditions. Understanding economic depreciation helps businesses make informed decisions about asset replacement, budgeting, and overall financial planning.

2. What is an example of economic depreciation?

An example of economic depreciation is the value decline of machinery used in manufacturing. As the machinery ages and becomes less efficient, its economic value decreases, impacting the company’s productivity and profitability. Economic depreciation differs from accounting depreciation, which may use different methods and timelines to calculate asset value changes.

3. What is the risk associated with economic depreciation?

The risk associated with economic depreciation lies in potential losses for businesses. If the decline in asset value is not properly accounted for or anticipated, companies may face unexpected costs, reduced efficiency, and a competitive disadvantage. Failing to adapt to economic depreciation can lead to operational inefficiencies and financial strain on businesses.

Recommended Articles

This has been a guide to Economic Depreciation and its definition. Here we discuss how economic depreciation works along with its causes and differences from accounting depreciation. You may also have a look at the following articles –