What is MACRS Depreciation?

MACRS (the full form is Modified Accelerated Cost Recovery System) is a depreciation method used in the United States for tax purposes. It allows for a higher depreciation deduction in the earlier years and less in the later years. It aims to maximize deductions using accelerated depreciation to encourage capital investments.

However, MACRS depreciation tables are not advisable for expenses for audited financial statements as these rules ignore the useful life of the asset and salvage value. Hence, businesses need to maintain separate books for tax and accounting purposes for depreciation differences to experience maximum benefits in their cash flow and tax filing as well.

MACRS Depreciation Explained

The Modified Accelerated Cost Recovery System (MACRS) is a depreciation method used for tax purposes in the United States to recover the cost of tangible assets over a specific period. MACRS allows businesses to deduct the cost of qualifying property over a predetermined schedule, providing a systematic approach for allocating the asset’s cost over its useful life. This system is particularly advantageous for businesses as it accelerates the depreciation deductions, allowing for more substantial tax savings in the earlier years of an asset’s life.

MACRS assigns specific recovery periods to different categories of assets, such as machinery, equipment, and buildings, and determines the depreciation expense using a declining balance method. The depreciation rates under MACRS are accelerated, meaning a higher percentage of an asset’s cost is deducted in the earlier years, gradually decreasing in subsequent years.

One significant feature of MACRS depreciation table is the half-year convention, which assumes that an asset is placed in service halfway through the tax year, regardless of when it was actually acquired. Additionally, the system incorporates bonus depreciation, allowing businesses to deduct a percentage of the asset’s cost in the year it is placed in service.

MACRS simplifies the tax depreciation process, aligning with the principle that the value of an asset diminishes more rapidly in its initial years. This method promotes economic efficiency by providing businesses with tax incentives to invest in and upgrade their assets. Understanding and accurately applying MACRS is crucial for businesses to optimize their tax positions and enhance cash flow.

Formula

The MACRS depreciation calculation is done using a formula that considers the cost of the asset, its recovery period, and a specified depreciation method. The general formula for MACRS depreciation is as follows:

Depreciation Expense = (Cost of Asset x MACRS Depreciation Rate / Recovery Period) x Multiplier

Here,

Cost of Asset = The initial cost of the asset, excluding any salvage value.

MACRS Depreciation Rate = The percentage determined by the IRS based on the assigned asset class and recovery period.

Recovery Period = The number of years over which the asset is depreciated.

Multiplier = An adjustment factor that accounts for the half-year convention and the application of bonus depreciation if applicable.

IRS Calculation Schedule

To select the correct depreciation rate, one must follow the below based on the IRS Modified Accelerated Cost Recovery System MACRS schedule,

#1 – Classification of Asset Property

E.g., computer equipment is classified as 5-year property, office furniture is classified as 7-year property, residential rental property is classified as 27.5-year property, and non-residential real property is classified as 39-year property.

#2 – Selection of the Depreciation Method

Small business owners/certain owners may consider taking a lower tax deduction in the early years if they expect business profits to increase in later years or want to show higher profits in earlier periods. Generally, it is better to choose the higher depreciation rates in the earlier years for maximum tax savings.

Two depreciation systems are available: the General Depreciation System (GDS) and the Alternative Depreciation System (ADS). Generally, GDS is used unless specifically mentioned using ADS.

#3 -The Period when the Asset was Placed & Disposed of Service

This principle establishes when the useful life of an asset begins and ends. It determines the number of months for which a tax deduction can be claimed when the asset is placed for use and the year its use ends.

There are three types of conventions for the period:

| Convention Types | Mid-month | Mid-quarter | Half-year |

|---|---|---|---|

| Property is placed in service or disposed of service. | in the mid of the month | in the midpoint of the quarter | the midpoint of the year |

| Applicability | Non-residential real property, residential real property, and any railroad grading or tunnel bore only. | When the mid-month convention does not apply, and total depreciable property placed in service or disposed of during the last three months is more than 40% of the total depreciable bases in service during the entire year; | When neither the mid-month convention nor the mid-quarter are applicable; |

| The tax deduction is limited to | The half-month depreciation was when the property was placed/ stopped in service | To 1.5 months of depreciation in the month, the property was placed/ stopped in service. | Six months of depreciation in the month the property was placed/ stopped in service. |

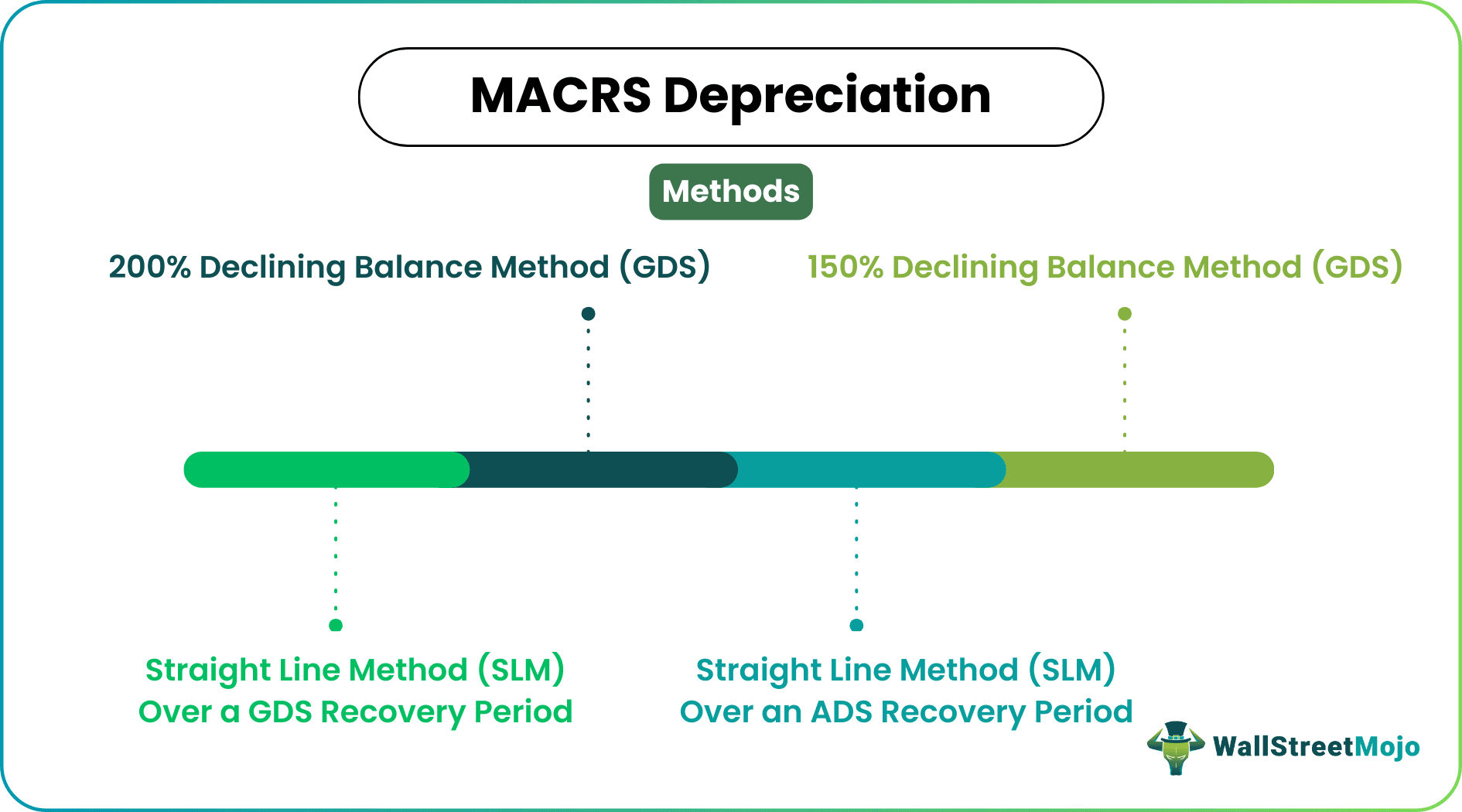

Methods

Based on the IRS, there are four MACRS depreciation calculation methods. Three are covered in the GDS system, and the last method is under the ADS system.

#1 – 200% Declining Balance Method (GDS)

It means the depreciation rate is double the straight-line depreciation rate and provides the highest tax deduction during the initial years. Then, it changes to the straight-line method when that method provides an equal or higher deduction.

#2 – 150% Declining Balance Method (GDS)

The depreciation method provides a greater depreciation rate of 150% more than the straight-line method. It then changes to the straight-line depreciation amount when that method provides an equal or greater deduction.

#3 – Straight Line Method (SLM) Over a GDS Recovery Period

SLM Depreciation method allows for a deduction of the same amount of depreciation every year except the first and last year of service.

#4 – Straight Line Method (SLM) Over an ADS Recovery Period

This method is similar to the above SLM method. However, this method is specifically for the mentioned properties that have been used for business for less than 50% of the time. Hence, the depreciation schedules generally have more extended depreciation periods for a property.

Examples

Now that we understand the basics and intricacies of MACRS depreciation table, let us understand the practicalities of the concept through the examples below.

Example #1

A machine with a life of 7 years is purchased for USD 5000 and placed into service on January 1. Based on the steps mentioned above,

- Classification of an asset – it’s a 7-year property

- Selection of depreciation method – Half-year convention, since:

- It isn’t qualified for assets mentioned under mid-month convention &

- It was purchased in the last quarter of the tax year to qualify for the mid-quarter convention.

- As the asset is considered to be “non-farm” 7-year properties, GDS using the 200% DB method is considered.

- The period when the asset was placed & disposed of service: Was placed in service on January 1, i.e., 1st

Using the rates mentioned by IRS, for a 7-year property gives us a depreciation rate of 14.29% for year 1 based on a 200% declining balance.

$5000 X 14.29% = 714.5

Example #2

A computer with a life of 5 years is purchased for USD 5000 and placed into service on April 1. Based on the steps mentioned above,

- Classification of asset property – it’s a 5-year property

- Selection of depreciation method – Half-year convention, since:

- It isn’t qualified for assets mentioned under mid-month convention &

- It was purchased in the last quarter of the tax year to qualify for the mid-quarter convention.

- As the asset is considered to be “nonfarm” 5-year properties, GDS using the 200% DB method is considered.

- The period when the asset was placed & disposed of service: It was placed in service on April 1, i.e., 2nd

Using the rates mentioned by the IRS for a 5-year property gives us a depreciation rate of 20% for year one based on a 200% declining balance.

$5000 X 20% = 1000

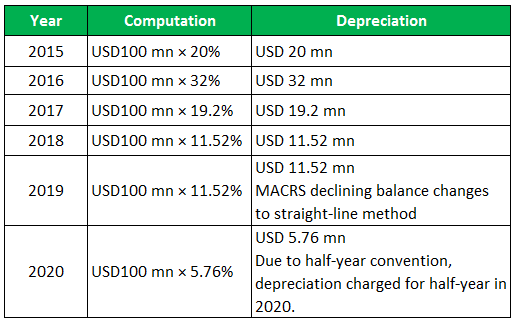

Example #3

ABC recently installed office furniture at the cost of USD 100 mn, which was put to use on May 30, 2015. The company’s year-end is December 31.

The calculation of MACRS Depreciation is performed in the following steps:

- Classification of asset property – it’s 5-year property.

- Selection of depreciation method – Since the property does not fall into the mid-month or mid-quarter convention, the half-year convention is relevant & the organization can choose either the 150% or 200% declining balance method.

- The period when the asset was placed & disposed of service: It was placed in service on May 1, i.e., 2nd quarter.

Depreciation

The depreciation based on the Modified Accelerated Cost Recovery System(MACRS) is recognized in the company’s income tax return and used to determine taxable income by factoring in any tax credits and deductions that can be claimed on the property. Putting all together, classification & cost of asset, depreciation method, and the period when the asset was placed into service determines the Modified Accelerated Cost Recovery System (MACRS).

MACRS Depreciation Vs Straight Line Depreciation

Let us understand the distinctions between MACRS depreciation table and the more popular straight line method of depreciation through the comparison below.

MACRS Depreciation

- MACRS, or Modified Accelerated Cost Recovery System, is an accelerated depreciation method used for tax purposes.

- Assigns specific depreciation rates to different classes of assets over predetermined recovery periods.

- Front-loads depreciation deductions, allowing for higher deductions in the earlier years of an asset’s life.

- MACRS accelerates depreciation for tax benefits and tax reporting.

Straight Line Depreciation

- Straight-line depreciation evenly spreads the cost of an asset over its useful life.

- Calculates depreciation at a constant rate, with the same amount deducted each year.

- Provides a consistent and predictable depreciation expense annually.

- Straight-line provides a steady and linear depreciation expense and is used for financial statement reporting and simplicity.

Recommended Articles

This article has been a guide to what is MACRS Depreciation. Here we explain its formula, calculation, and examples, and compare it with straight line depreciation. You may learn more about Accounting from the following articles –