Part of our Microeconomics guide

Economic Equilibrium Definition

Economic equilibrium is when market forces remain balanced, resulting in optimal market conditions in a market-based economy. The term is often used to describe the balance between supply and demand or, in other words, the perfect relationship between buyers and sellers.

Market price plays a significant role in establishing economic equilibrium and results when supply meets the demand. When an economy is in equilibrium, there should be no surplus or shortage of goods or services. Since the market is always functional, the possibility of it achieving equilibrium seems a bookish concept.

- Economic market equilibrium occurs when supply and demand levels align, creating ideal market conditions for buyers and sellers.

- The types of economic equilibrium include microeconomic and macroeconomic. In microeconomics, supply and demand between buyers and sellers are balanced. With macroeconomics, an economy achieves a balance of aggregate demand and supply.

- Competitive prices are an integral part of the theory. However, the evolving market condition makes economic equilibrium a far-fetched scenario.

- The equilibrium can be static, meaning the inputs are constant. Or, it can be dynamic where the factors are constantly changing.

How Does Economic Equilibrium Work?

When it comes to a market-based economy, there are two groups of individuals:

- Buyers

- And sellers

Buyers keep looking to purchase goods, and in turn, create demand, or the willingness and ability to buy goods at a reasonable price. When there is a demand for products or services, buyers will need someone to provide those goods at a reasonable price. It is where sellers come in. Sellers create supplies for produced goods that can sell at a specific price.

The price of these goods and services can profoundly affect buyers and sellers in a given market. Economists have coined two terms for the price relationship between buyers and sellers. These include:

- Law of demand, and

- Law of supply

The law of demand implies that sellers will demand less when prices increase. And the opposite is also true when prices decrease. The law of supply states that as demand rises, buyers must increase output to benefit. These two basic economic laws help keep prices in check and fair for both buyers and sellers.

Naturally, because of this, prices gravitate towards a balanced mean or look to be in a state of equilibrium. It happens when the quantity supplied equals the quantity demanded, or in other words, the prices are ideal for both buyers and sellers.

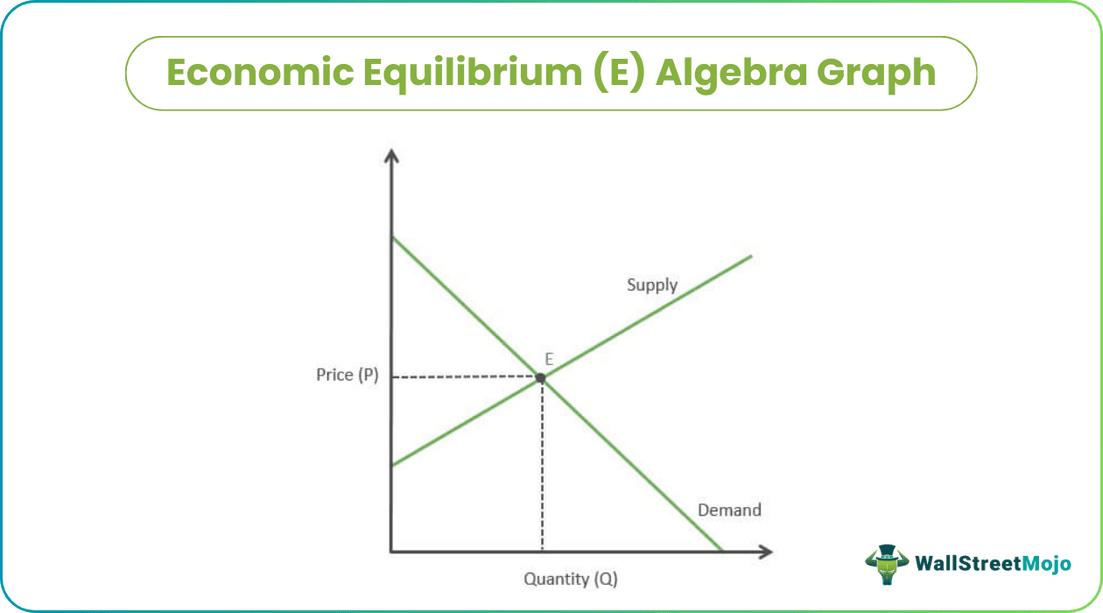

Finding Economic Equilibrium

Using algebra, one can determine the exact point at which the supply and demand curves will intersect on a given graph and achieve equilibrium.

First, one will have to determine the equations for the demand and supply curves. Let us assume the economic equilibrium price of movie tickets. The supply and demand curve equations for movie tickets are as follow:

- Supply curve (quantity supplied) = Qs = 30 – 3P

- Demand curve (quantity demanded) = Qd = 5 + 2P

Next, to find Qs = Qd, we will combine the equations.

- Qs = Qd

- 30-3P = 5 + 2P

- – 3P – 2P = 5 – 30

- – 5P = – 25

- 5P = 25

- P = 5

In this case, the equilibrium for movie tickets equals $5 for buyers and sellers to agree on the price and quantity.

Real-World Example

Technology is an excellent economic equilibrium example. Companies must compensate to achieve market equilibrium in economics and maximize profitability due to constant supply and demand changes. For example, Apple, the maker of iPhones, has significant demand for their technology.

However, according to information from Statista, there is a clear trend indicating that demand for iPhones varies throughout the year. For example, during the first quarter of each year, iPhones’ sales are much higher than the rest of the year. Because holiday sales contribute to the first quarter financial results, Apple releases each quarter.

With that said, Apple must compensate for the increase in demand and match the supply necessary to achieve maximum profitability. If they fail to do so, they will be missing out on revenue.

When the demand starts to decrease as the holidays are over, Apple will cut back on supply and adjust the price to meet the demand for the year’s remainder. As Apple has developed and matured over the years, they have learned the most efficient methods of achieving this. Thus, it has become the first U.S company valued at over $2 trillion.

Types of Economic Equilibrium

There are a few different types of economic equilibrium, including:

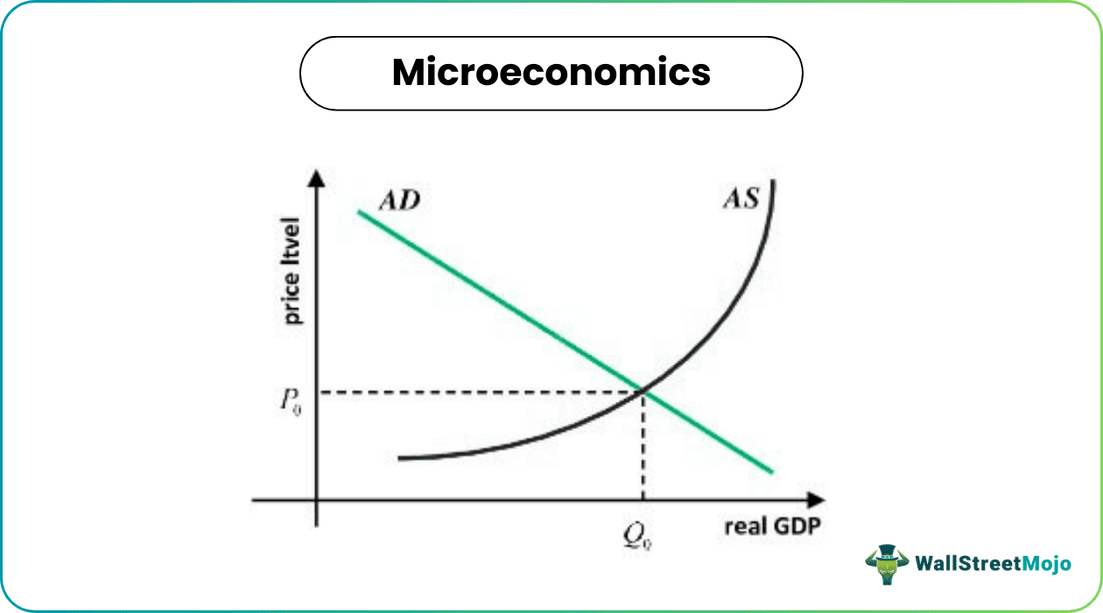

Microeconomics

Microeconomics is concerned with individuals’ and businesses’ activities and how they interact to achieve maximum results. Here, economic equilibrium occurs when the price of a good is equal to satisfying supply and demand needs.

When supply and demand intersect, this is considered the point of economic equilibrium, and the price is determined accordingly. The Apple example from above can be seen as a case of microeconomic equilibrium.

Macroeconomics

Macroeconomics looks at the economy from a wider lens. It involves studying economic factors like gross domestic product (GDP), interest rates, and fiscal spending. Economic equilibrium is achieved in macroeconomics by balancing the inputs and outputs, such as aggregate demand and aggregate supply.

Source

When an economy can match the nation’s aggregate supply and aggregate demand, it is in economic equilibrium. If the economy has more supply than demand, it is wasting resources. However, if they have more demand than supply, they miss out on profits.

Static vs. Dynamic

The economic equilibrium in micro and macroeconomics can be further divided into static and dynamic categories.

Static = In static equilibrium, the factors or inputs will not change. For example, demand and supply will remain constant. As a result, all parties involved are achieving maximum gratification.

Dynamic = In dynamic equilibrium, the factors or inputs are constantly varying. Examples can include prices, rates, and ever-changing income levels.

Recommended Articles

This has been a guide to Economic Equilibrium and its definition. Here we discuss how to find it, how it works, and an example and its types. You can learn more about accounting from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.