Part of our Supply and Demand guide

Economic Shortage Definition

Economic shortage is a situation where the demand does not meet the supply of goods and services, thus creating a shortage. Here, the demand for goods or services will be high, but the supply does not match the level of demand, resulting in a price rise.

They are often seen with an increase in price as more people are willing and have better purchasing capacity. This is due to the market not being in equilibrium. Equilibrium is achieved when demand equals supply at the market price. Therefore, a shortage is a market phenomenon different from the concept of scarcity.

- Economic shortages are situations where unequal market supply and demand prevail.

- An increase in demand, a decrease in supply, and government interventions are reasons for the economy’s shortages of goods and services. Examples of shortages include food, water, power, and labor.

- Demand or supply changes can occur for various reasons; not all are related to a price change.

- Scarcity and shortage are two different, and certain economic shortage characteristics make them stand apart.

Economic Shortage Explained

The economic shortage is a broad event the cause of which is an imbalance in the equilibrium. As mentioned previously, it is the mismatch between quantity demanded and quantity supplied. It is mostly prevalent in socialist economic systems. However, market factors make it appear in a capitalist economy also. Due to the prevailing economic conditions, different types of economic shortages can occur. Water shortages, food shortages, power shortages, and labor shortages are a few examples of the common types of economic shortages.

The concept of shortage is different from scarcity. There are specific Economic shortage characteristics that distinguish it from scarcity, such as:

| Scarcity | Shortage |

|---|---|

| Scarcity can be termed as a situation where the resources already available in a limited quantity are unavailable | On the other hand, a shortage is a situation where the quantity is not limited in nature but is available in a lesser quantity at a particular time. |

| As it is often irreplaceable, scarcity can be permanent in nature, such as the scarcity of fresh water | In comparison, shortages are temporary in nature, for example, a shortage of clothes. They can be manufactured to control the crunch. |

| Scarcity is created by nature | Market forces create a shortage |

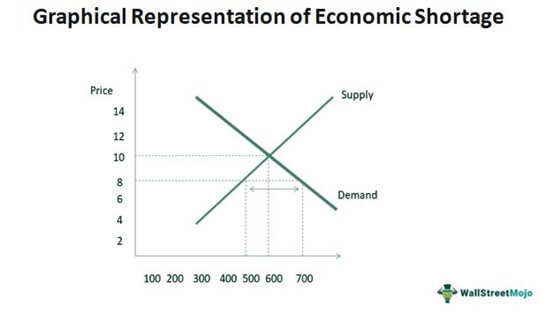

Economic shortage graph

One can demonstrate economic concepts and shortages through graphs.

In the below economic shortage graph quantity of apples demanded is 700 tonnes for a price of $8, but the quantity supplied was 500 tonnes. Hence, there is a shortage of 200 tonnes (700-500). Therefore, it is below the point of equilibrium (where supply and demand meet).

Causes

The three main reasons why shortages can happen are:

An increase or higher demand-depicted by an outward shift in the demand curve. E.g., Demands for umbrellas and raincoats increase during the rainy season.

An inward shift in the supply curve depicts a lower or decrease in supply. Low supply may be due to shipping delays, supply chain management issues or labor shortages, restrictive policies by the government, etc.

Intervention by the government- The government’s intervention is usually done to control the situation. For example, in times of war, staple foods like potatoes will be restricted (low supply, high demand). It will be hoarded and kept, leading to a further price increase. The government will try to limit how much an individual can buy to stop hoarding as a solution.

The increases or decreases in the demand and supply factors are not movements along the demand or supply curves. Changes in demand or supply need not always be a result of a price change, and therefore the shift can happen due to various factors. For example, if there is a social media trend about a new type of clothing, that particular clothing might be in demand overnight. This can push the demand high without price being a driving factor.

Example

Unavailability of cheese, coffee, and olive oil due to a supply crisis at California ports in Los Angeles and Long Beach:

Californian cities Long Beach and Los Angeles ports account for one-third of U.S. imports. They are the primary source of imports from China and have been congested for a long time. As a result, the container ships were waiting off the shores for many weeks. This further resulted in delayed deliveries. The reason that contributed to this was the size of the ships. The larger ships, called mega-container ships, take more time to unload. This is due to increased consumer spending resulting in import spikes and overloaded ports. These problems have ripple effects across the market. The shipping delays limit the availability of the commodities in the market (this is called a shortage). This now becomes an issue of supply. When there is a shortage of supply in the market, prices increase.

Therefore, companies like Costco had low-running supplies of cheese, seafood, and olive oil. At the same time, companies like Peet’s and JM Smucker (brands behind Folgers and Dunkin’ coffee) faced rising costs.

Frequently Asked Questions (FAQs)

What is an economic shortage?

It is a situation where the demanded goods or services are available less in the market for the market prices.

In other words, the supply does not meet the needs or demands of the general public. Shortages are not limited to a particular industry.

What causes economic shortage?

Various market factors cause shortages of goods and services; they may be due to a supply chain management crisis or a price rise in raw materials, but generally, it is because of an increase in demand, a decrease in supply, or due to government intervention.

What happens in economic shortage?

The effects of shortages depend on the industry. For example, a power outage could affect all industries. Likewise, water and food shortages will affect people’s livelihoods, and labor shortages will pause industrial growth, etc.

Why may an economic shortage occur?

It may occur due to anomalies in the market. However, they mostly arise when there is no equilibrium (demand=supply).

Recommended Articles

This is a guide to Economic Shortage and its definition. Here we explain the concepts of economic shortage, graph and causes along with an example.You can learn more from the following articles –