Part of our Types of Taxes guide

What Is First Time Abatement?

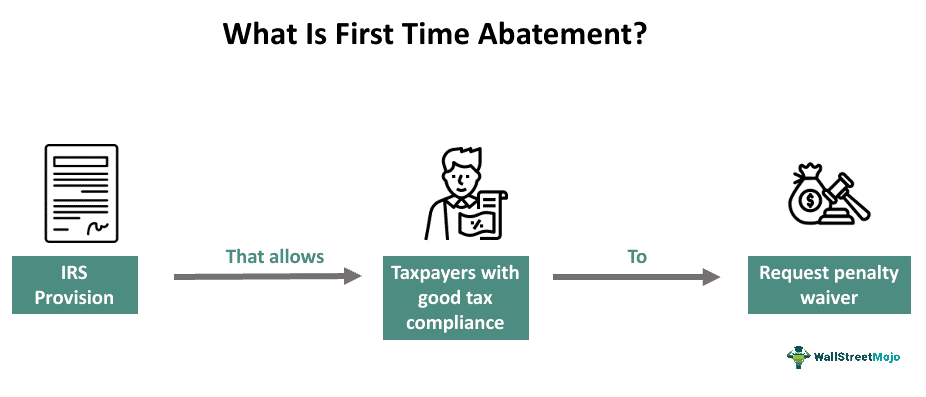

The First Time Abatement is a provision offered by the United States Internal Revenue Service to forgive or decrease an individual’s tax penalty in case they fail to comply with the tax law obligations. Not every tax-paying individual can apply for it as it requires them to meet certain criteria.

The whole concept, in a nutshell, is the US tax authority granting one a mistake, as anyone can make it. It is also observed as a reward to the taxpayers for their clean taxation and compliance history. Additionally, it is only considered by the IRS under certain circumstances and is seen as a useful remedy among the limited relief options the authority offers.

- The first time abatement is an IRS provision that allows taxpayers one mistake as a tax relief option to let go of the penalty or decrease it when they fail to comply under certain circumstances.

- The provision was introduced in 2001 by the IRS to help reward the clean taxation history of individuals and encourage future compliance with the tax regulations.

- An individual can request it by applying through a written letter signed and mailed to the IRS office.

- It is not for everyone and is only considered under certain circumstances and only if the requesting taxpayer meets the qualifying criteria.

First Time Abatement Explained

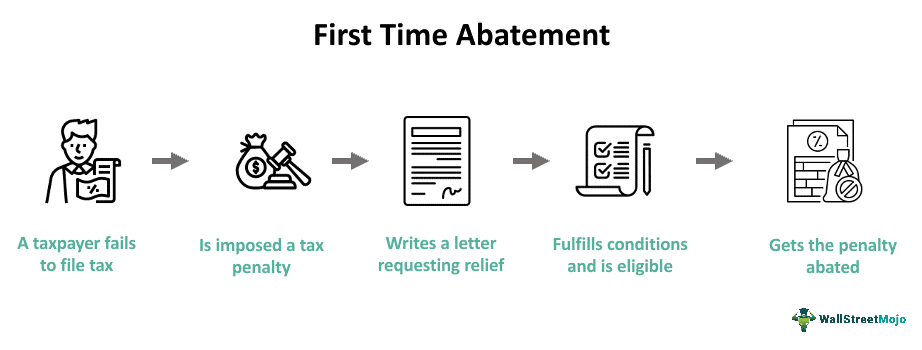

First time abatement is the simple provision of allowing the taxpayer a one-time mistake and forgiving or decreasing their tax penalty given that they have a reasonable cause and fit the qualifying criteria. The provision was introduced in 2001, and it all meant to be a way of not imposing any penalty on a taxpayer because they made a mistake filing the tax return.

A taxpayer has to formally write a letter, sign it, and mail it to the service center where they would be required to file a current year tax return; if the taxpayer is writing the letter in response to an IRS notice, the letter should be sent to the address printed on the notice.

The typical causes are –

- Failure to file unfiled tax returns penalty

- Failure to pay tax on time.

- Failure to make payroll tax deposit by the due date

The IRS first time abatement can only be claimed for a single tax period; the IRS uses a decision support software tool called the Reasonable Cause Assistant (RCA) to measure the eligibility of a taxpayer for an FTA, but lately, the RCA is being criticized for a high percentage of incorrect deriving of the eligibility.

A taxpayer who is persistent can convince the IRS to allow the first time abatement penalty and reverse the incorrect determination which marked them unqualified for it. A taxpayer will not get disqualified from the estimated tax penalty, and in case they have a record of prior penalties that the IRS abated for the cause. If an individual has already paid the penalty, they can request a refund by filing the IRS Form 843. It may take a while, efficient guidance and is more complex than filing for initial abatement.

How To Qualify?

The qualifying criteria for this provision are –

- The requesting taxpayer must be current on filing their tax returns, including if they have a tax extension.

- The requesting taxpayer must be current on their tax bill or at least have a payment arrangement organized with the IRS authority.

- The most important qualifying criteria is that the taxpayer must have a clean record with no penalties for the past three years before the tax year for which they have received a penalty and requested a tax abate.

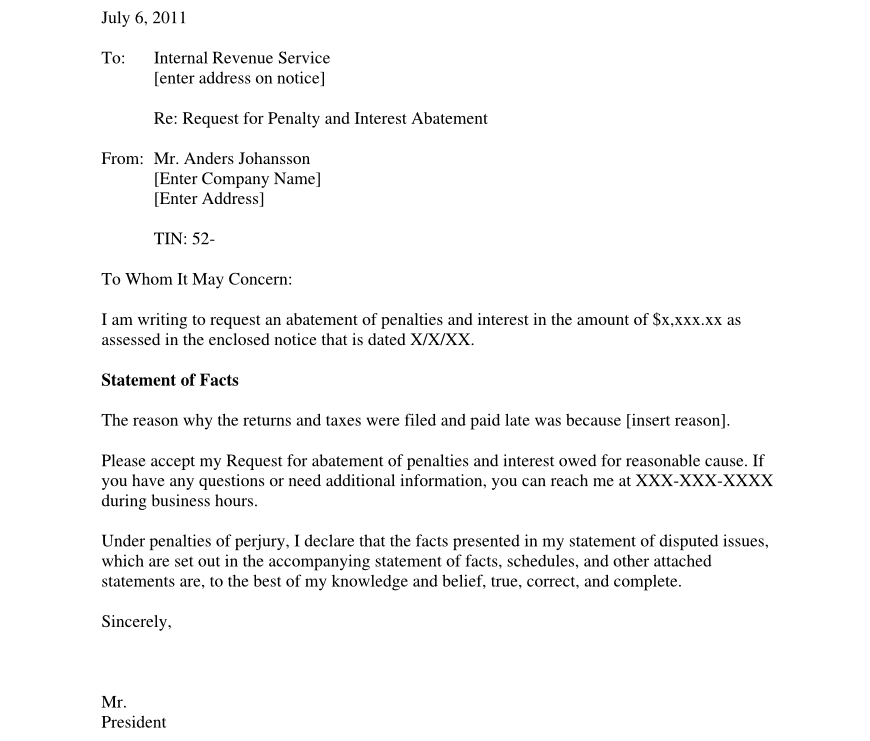

Letter Sample

The letter is addressed to the Internal Revenue Service with the email address given on the notice received by them. The subject line should specifically state the topic, which is the request for penalty and interest abatement.

Followed by the applicant’s general details like name, address and other contact details. Below this, the applicant can explicitly write to explain their condition with respect to the tax abatement process. The applicant’ must attach all the necessary documents with the letter along with other additional information.

Examples

Below are two examples to understand the concept better.

Example #1

Suppose Gerrard owns a small retail store; he is a law-abiding and tax-paying US citizen. Year after year, he paid his income tax on time without any delay. He never received any IRS letter or notice for any mishap, error, or wrong mention and manipulation of income.

In 2023, when he was about to pay his tax, Gerrard met with a car accident and failed to file his current year’s tax. Though the accident was small, he was prescribed extensive rest. All his family members took care of him, but again, in the chaos, he forgot to pay the annual tax.

Later, Gerrard was imposed a tax penalty. At first, Gerrard didn’t like it, but he knew about the tax abatement provision. He meticulously wrote a good letter to the IRS explaining his situation. Upon verification, the IRS found out that Gerrard also fits the criteria and is eligible for tax abatement. Hence, the IRS abates his tax penalty.

Example #2

After refusing to introduce the first time abatement of penalties to file tax returns for decades, California finally accepted the premise. In 2022, Governor Gavin Newsom signed the Assembly Bill 194, which established California Revenue and Tax Code Section 19132.5, granting the taxpayers a once-in-a-lifetime abatement.

This abatement applies penalties for failure to file and failure to pay, effective for taxable years beginning on or after January 1, 2022, and not before that. Requests for abatement can be made verbally or in writing with the FTB Form 2918, with contact information available on the website.

Frequently Asked Questions (FAQs)

1. What is a significant amount for first time abatement?

There is no proper record that follows, and the IRS does not define or publicly announce a significant amount that shall be the limit of the first-time abatement. The amount can vary based on various factors. However, a written request is more appreciated by the IRS compared to phone calls.

2. How to write a first time abatement letter?

The steps to follow while writing a first time abatement letter are –

• An Individual should address the IRS office properly.

• Specifically, mention the type of penalty they want to be removed.

• Maintain a polite tone explaining the events and circumstances of the situation that disable them from paying taxes on time.

• Attach documents to support their explanation.

How many times can you use the first time abatement?

There is a monetary limit on the number of penalties that can be removed. If the IRS refuses to remove the penalties in one go, the applicant may observe that the penalties are growing. Still, as long as they qualify for the reduction, they can keep on trying, and eventually, the penalties will be removed.

Recommended Articles

This has been a guide to what is First Time Abatement. Here, we explain the concept along with its letter sample, examples, and how to qualify for it. You can learn more about financing from the following articles –